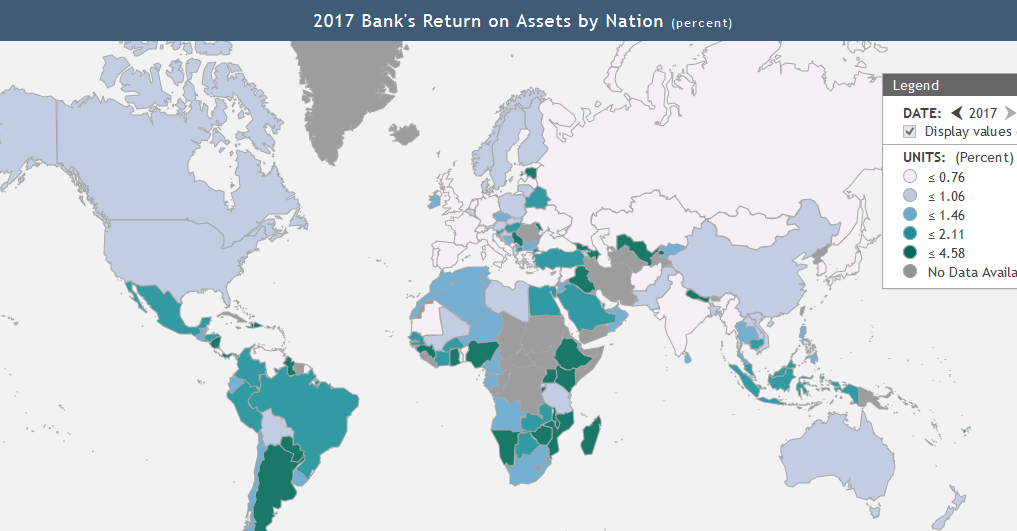

Duurzaam beleggen zitindelift. Beleggers willen dat hun geld maatschappelijk verantwoord en ethisch geïnvesteerd wordt.

Maar ben je zeker dat je geld naar ‘propere’ bedrijven gaat?

In sommige duurzame fondsen zitten oliebedrijven, tabaksfabrikanten en belastingontduikers

Fondsenbeheerders verwijzen vaak naar de ESG (environmental, social and corporate governance) score om aan te duiden dat hun beleggingen verantwoord zijn. Helaas zijn er geen eenduidige regels om die score op te stellen.

In the thread below, Benjamin Braun explains Germany’s political economy. More specifically, he and Richard Deeg studied the interaction between the financial and non financial corporate (NFC) sectors.

‘German banks' supply of patient capital is the lifeblood of the German growth model’

The German NFC sector has high profits (1) and runs a trade surplus (2).

(1) enables companies to finance their own investments. They don’t need to borrow money from banks.

(2) leads to an inflow of reserves and deposits at banks. As a result, German banks lend to foreign entities.

This seems a sensible story.

However, I don’t agree with the conclusion:

The conventional policy wisdom is that Germany is overbanked. That may be true, but also German workers are underpaid. Policymakers who want to help German banks should focus on strengthening unions, raising wages, and on moving away from export-led growth. /END

First of all, I highly doubt any policymakers really want to help German banks. If that were the case, the monstrosity of publicly owned, unprofitable banks would have been cleaned up by now.

But even if German politicians cared, it’s not clear that stronger unions or higher wages would be more than a drop in a bucket.

A higher demand for credit would have an immediate positive impact on German banks. And there is a lot of room for growth.

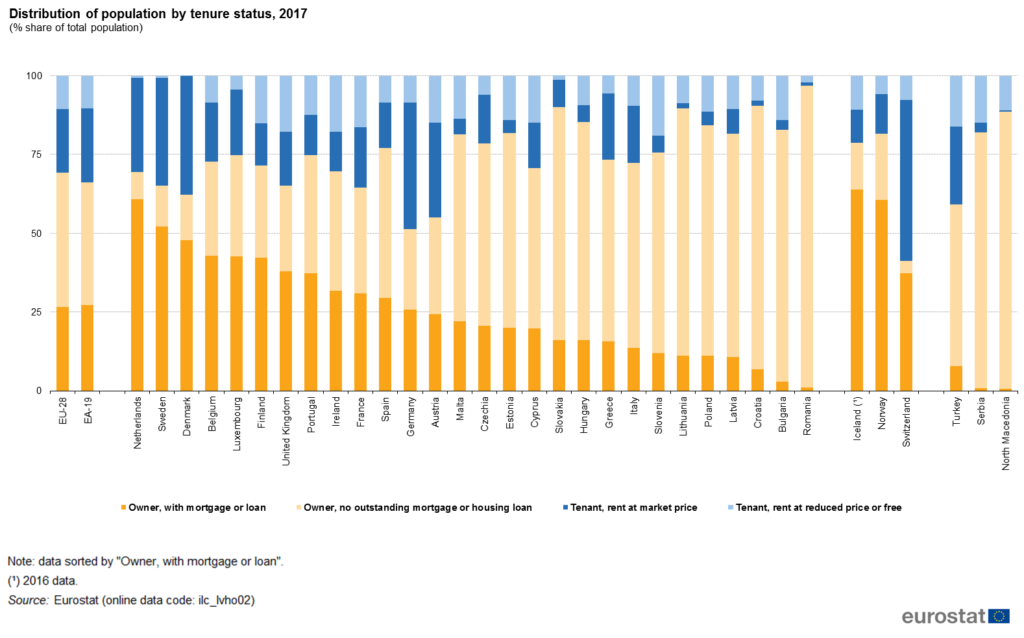

Home ownership in Germany is low compared to non-German speaking countries, as you can see in this picture from Eurostat.

Stimulating home ownership would boost the demand for mortgages.

More investment by the government, as called for by industry and labor unions, would also increase the domestic supply of assets for banks if it’s funded by bonds instead of taxes.

If Angela Merkel wants some more advice, she can leave a comment 🙂

The interest rate on its savings account will be zero percent, which is less than the minimum of 0.11% at other banks.

Finally, there’s no indication that it will delight customers with superior services.

So NewB scores zero out of three.

Yet NewB’s business plan expects the bank to have 277 million euro in deposits by the end of 2024.

Some Chinese banks offer pork meat as a reward for opening an account. Maybe NewB should give an Impossible Burger to new customers? Otherwise, this is gonna turn into Mission: Impossible.

What do crypto enthousiasts have in common with defenders of independent central banks?

Based on the “Buy Bitcoin”-replies to ECB/Fed tweets, it seems the answer is “not much”.

However, that’s incorrect. Both groups think that their projects are apolitical.

Many central bankers view themselves as technocrats, divorced from politics.

But that’s a fantasy.

You see, anything a central bank does – even within its mandate – has political consequences.

Should monetary policy take into account climate change?

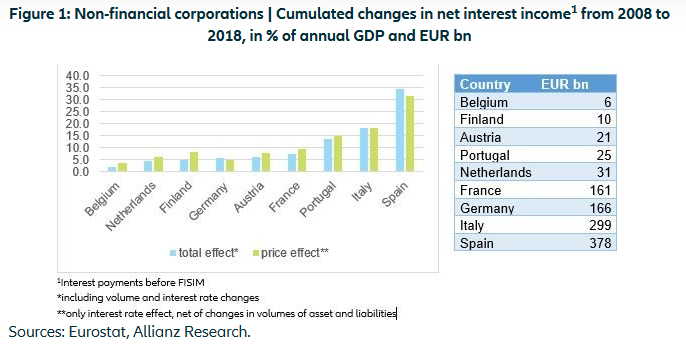

Should the central bank change interest rates or do QE to reach its inflation goal? Whatever option is chosen, monetary policy has distributional effects. For example, the German government has saved hundreds of billions in interest costs.

European non-financial corporations have benefited from low interest rates. Source

These two dilemmas illustrate that central banking is inherently political.

Therefore, economists should calculate the consequences of different monetary policy options. These scenarios will make the politics of the central bank’s actions explicit. For example, I estimated the effect of deeply negative interest rates (a proposal of Miles Kimball) on banks, governments, the ECB and the private sector.

Especially in the euro area, the ECB should take differences in asset mixes between countries into account.

Increased transparency will enable central bankers to defend monetary policy against criticism.

Update 26 January 2020: my arguments are obviously not new, see for example:

"Politics is built into central banking. […) Monetary policy choices may not be as politically divisive as war or welfare programmes, but they are too controversial ever to be purely technocratic." Heterox ideas 5 y ago, common view today. Great article also https://t.co/r3TkhkNlVu

Computer-aided design (CAD) enables engineers to create products much faster and cheaper compared to trial and error.

But did you know that innovators have used abstract modeling long before the existence of computers?

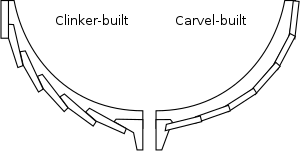

Anton Howes, a historian of innovation, tells the story of Matthew Baker. Baker was a 16th century shipbuilder who improved the construction of carvel ships.

Carvel-built hull versus the previous clinker-built method. Source

As Howes explains:

What Matthew Baker did in the 1570s was to take the design process out of the shipyard, and onto paper. He drew his ships, to scale. And by using pen and paper, with geometry to make such drawings possible, he opened up grand new possibilities for design. […] He drew out new designs for frames, using geometry to work out how any variation would affect the overall shape of the hull, as well as its weight and carrying capacity – all at the cost of only time, ink, and paper, and avoiding the huge potential waste of conducting experiments at full scale in wood. His process allowed him to innovate more easily, and even to design new measuring instruments.

Interestingly, the new methods were not quickly adopted in the rest of Europe:

By the 1580s, new English ships were among the most technically advanced in Europe, and even in the mid-seventeenth century, ship plans were apparently still unknown in France. Having once lagged far behind, geometry began to give English shipbuilding the edge.

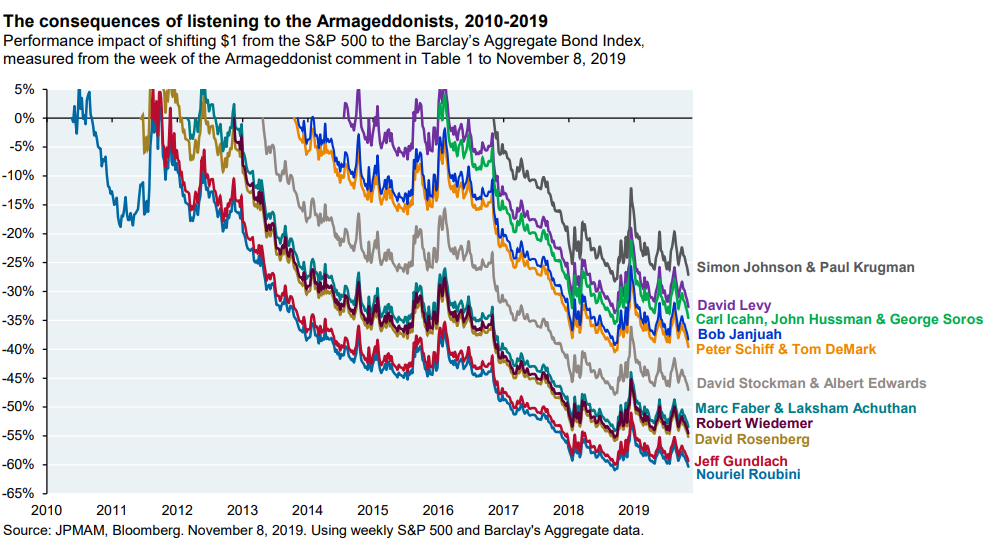

Journalisten zijn dol op “experts” die voorspellen dat er een beurscrash komt. Doemberichten zorgen voor clicks.

Analisten van de Amerikaanse bank JP Morgan hebben een overzicht gemaakt van hoeveel geld je liet liggen door hun voorspellingen op te volgen. De resultaten zijn ontnuchterend: tot 60%…

{kind=link}

#/media/File:Clinker-carvel.svg){kind=link}