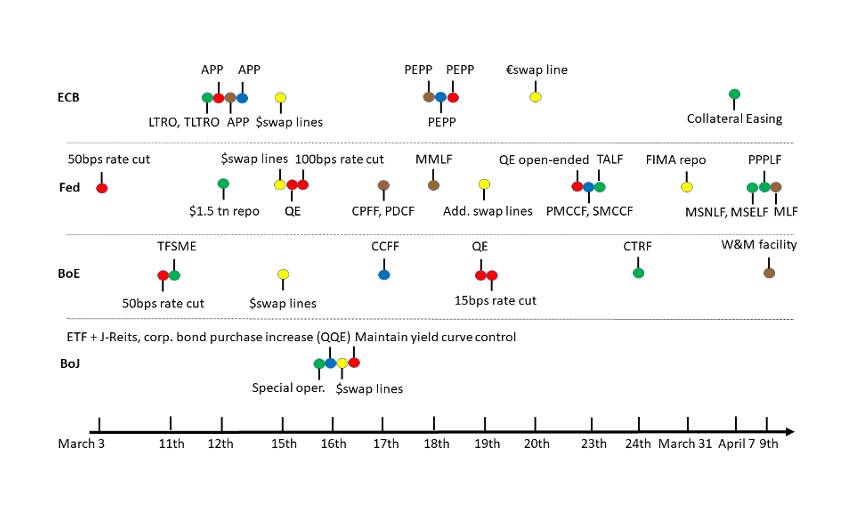

Ancient history: “In 2003, refinancing via LTROs amounts to 45 bln Euro which is about 20% of overall liquidity provided by the ECB.” (On June 18, 2020, banks borrowed 1.31 trillion euro from the ECB via TLTRO!)

Many European banks and insurance companies are trading well below their book value.

Large firms can unlock a lot of value by taking over smaller competitors, thanks to the negative goodwill. Consolidation would support the profitability of the financial industry.

Also first serious hostile takeover in the world of banking since ages. The buyers are looking to split UBI into pieces (and to finance this with badwill ?) https://t.co/GzYHANZmf4

Italian banks in particular would benefit from a consolidation of their fragmented domestic market1. In February, Intesa Sanpaololaunched a bid for UBI Banca. UniCredit should consider a similar deal with Banco BPM, Banca Monte dei Paschi di Siena or BPER Banca. Also, French BNP Paribas could merge its subsidiary BNL with one of those banks.

Spain

Spanish banking is already quite concentrated. Santander took overBanco Popular in 2017. The integration was completed in 2019. Santander and BBVA could acquire Bankinter, Bankia, or Banco de Sabadell. Of course, further domestic growth of the majors depends on regulatory approval. The two global Spanish banks definitely have the expertise to execute such an operation.

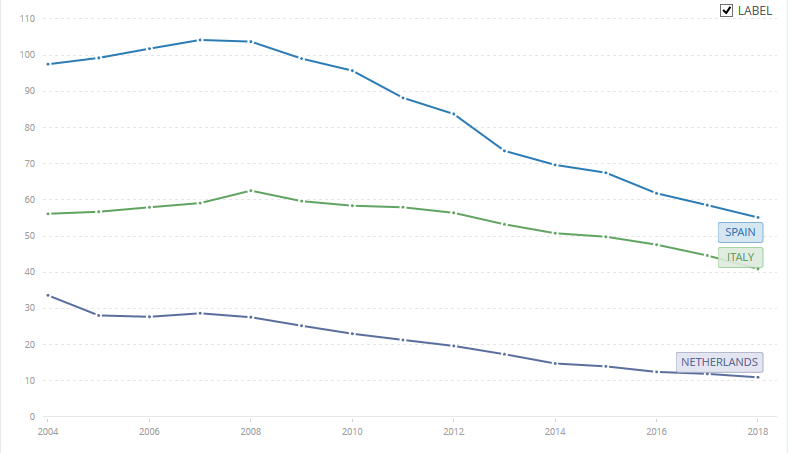

Figure 1 shows the number of bank branches relative to population for Spain, Italy and the Netherlands. It’s clear that Italy and Spain have a lot of potential for cost cutting.

Figure 1: Commercial bank branches per 100,000 adults in Spain, Italy and the Netherlands. Source: World Bank.

Portugal, Poland and the Netherlands

In neighbouring Portugal, Banco Comercial Português seems a good match for Santander. Especially since both Iberian banks are active in Poland. Speaking of Poland, Santander and ING might be interested in mBank. mBank is owned by Commerzbank, a bank that desperately needs to focus its strategy.

A foreign group could shake up the uncompetitive Dutch market by buying ABN AMRO. However, as most of ABN AMRO is still state owned, this will be complicated.

Insurance

Many listed insurers like Aegon, NN Group (NL), Ageas (BE), Baloise, Swiss Life (CH) or UnipolSai (IT) trade at a significant discount to their book value. This could be an opportunity for big insurance companies AXA, Allianz and Zurich Insurance Group.

Consortiums of buyers could also divide the operations of their targets (although there is a bad precedent for this scenario).

Update 23 July 2020: Marc Rubinstein at Net Interest came to the same conclusion: “Coming out of Covid, when banks realise they don’t need such a large physical presence, further consolidation is likely. What’s more, if equity valuations don’t recover, banks may be able to use negative goodwill to cover restructuring charges.”

Door de lockdown hebben veel bedrijven verlies geleden. Het ligt voor de hand dat de overheid de schade moet vergoeden.

Maar in plaats van dat rechtstreeks te doen, met eenduidige voorwaarden, bouwt de politiek weer een reeks koterijen bij.

Politici hebben de mond vol van gerichte maatregelen en vereenvoudiging.

In realiteit krijgen we hinder- en sluitingspremies (een druppel op een hete plaat voor grotere bedrijven), lagere btw voor de horeca (hulp aan één sector), cadeaus voor kapitaalverstrekkers (investeren is risico’s nemen, waarom moet dit een fiscaal voordeel krijgen?)…

Ik hoop dat politici die voor deze maatregelen stemmen niet gaan zagen over de ingewikkelde belastingaangifte of over toekomstige begrotingstekorten1.

De gegoede klasse zoals politici, professoren en vermogensbeheerders (tiens, wie zat ook al weer in het economisch relancecomité?) wordt in de watten gelegd. Zo wordt de btw op restaurant verlaagd naar 6%2. En wie tot 75.000 euro belegt in “vriendenaandelen” krijgt als beloning een jaarlijkse belastingkorting.