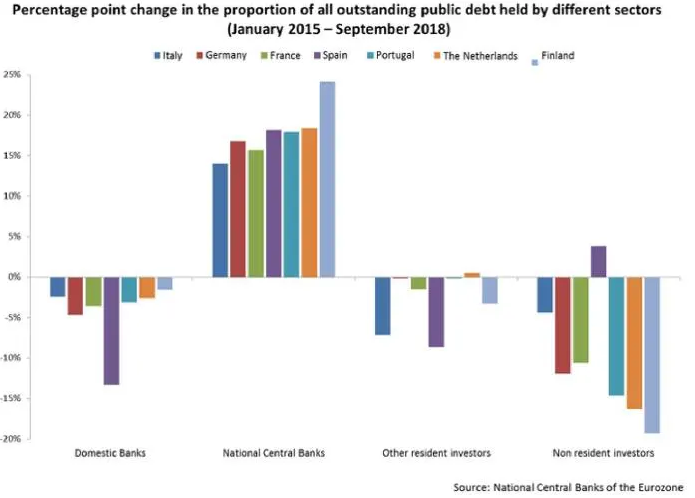

Mainly non-resident investors, although there are national differences, as this graph by Marcello Minenna shows:

What did companies do with the money from the ECB?

Corporates used the attracted funds mostly to increase dividends, according to research by Karamfil Todorov.

Did QE ease financial conditions?

Yes. Karamfil Todorov found that the ECB’s Corporate Sector Purchase Programme (CSPP) “increased prices and liquidity of bonds eligible to be purchased substantially”1.

Can we trust central bank research on the effect of QE?

Central bank researchers face strong incentives to be positive on QE. Brian Fabo, Martina Jančoková, Elisabeth Kempf and Ľuboš Pástor found that “central bank papers report larger effects of QE on output and inflation. Central bankers are also more likely to report significant effects of QE on output and to use more positive language in the abstract. Central bankers who report larger QE effects on output experience more favorable career outcomes.”

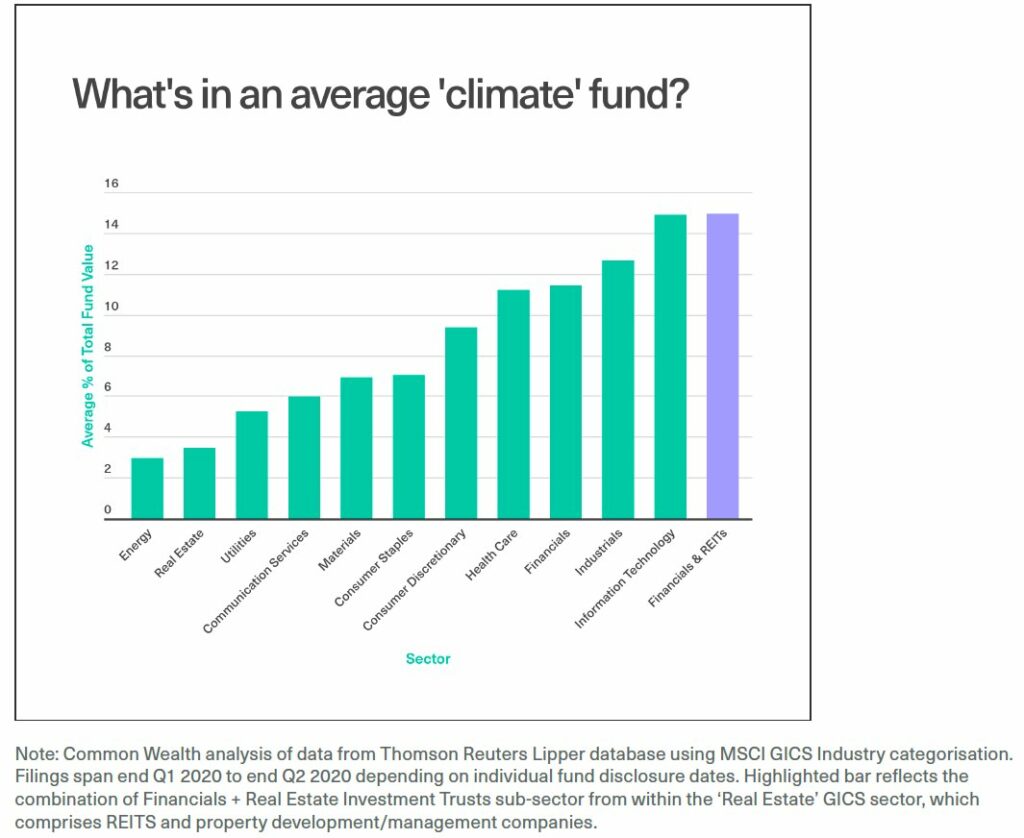

A report by Common Wealth found that some climate-themed funds invest in oil & gas companies such as ExxonMobil. More broadly, the largest holdings of climate funds were Big Tech and finance. Adrienne Buller, the author of the study, writes “what do these ostensibly climate-focused funds really contribute to combatting the climate crisis, reducing emissions or driving a rapid transition to low carbon economic activities? There is nothing in the specific labelling or remit of these funds that would require them to invest in the green economy, in financial instruments design to drive the transition of business models to lower carbon activities, or other similar investments.” (emphasis mine)

There are plenty of metrics by which providers assess climate risk. Given different methodologies and the complexity of estimating climate risk, there is some divergence in the metrics. However, Chiara Colesanti Senni and Julia Anna Bingler do find that “metrics tend to converge for companies that are most and least exposed to climate risk”.

Data and tools for monitoring climate change and financial assets:

Aggregate assets and liabilities of Financial Institutions (banks, insurers, securities institutions)

Monetary Policy Reports, includes breakdown of loans and deposits by borrower (households, enterprises and public entities, non-banking financial institutions, overseas), lending volumes according to size of banks, Aggregate funding to the real economy according to loans, bonds, other funding; balance of payments, foreign exchange reserves

Monetary Policy Instruments, including Open Market Operations (short term reverse repo), Required Reserves (required reserve ratios), Interest Rates, Lending Facilities

How can the European Central Bank (ECB) support a sustainable recovery? In a report for Positive Money Europe and Sustainable Finance Lab, Jens van ‘t Klooster and Rens van Tilburg propose that the ECB starts a Green TLTRO program.

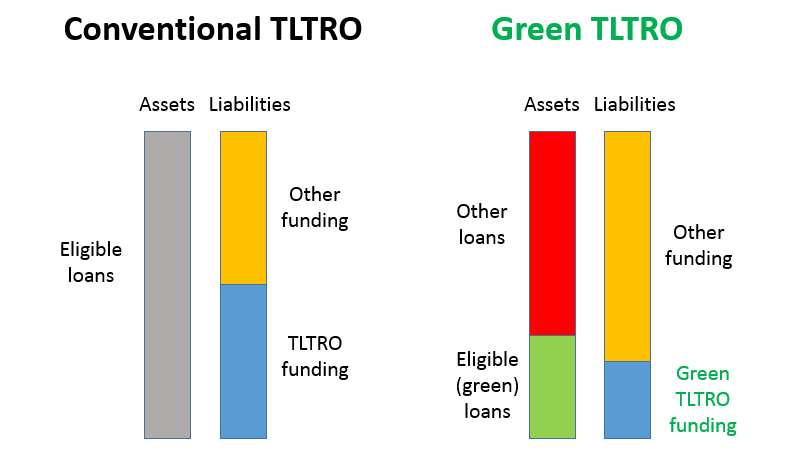

Green TLTRO is a refinancing program for commercial banks. Banks can fund their green loans with longer term (several years) deposits from the European Central Bank (ECB). Green loans are bank loans that comply with the EU’s Green Taxonomy.

The figure below shows the balance sheet of a commercial bank with conventional (left) and green (right) TLTRO. Under TLTRO-III, the ECB funds 50% of a bank’s eligible assets. Under green TLTRO, the ECB funding is only available for green bank loans.

The interest rate on the Green TLTRO is determined by the volume of green bank loans. More green loans result in a lower interest rate on the funding from the ECB. With negative interest rates, banks have to pay back less to the ECB than they borrowed. This provides a strong incentive to banks to increase their lending to green projects, and to pass on the low rates to borrowers.

Is Green TLTRO a pie in the sky proposal? Only if you’re not keeping up with the times.

TLTROs are a well-established monetary policy tool. The ECB is currently doing TLTRO-III.

Today at 11:30CET we'll get the allotment for ECB's TLTRO-III.5. Expect a much smaller take-up than in June, although potentially above €50bn.

There's €5.7bn maturing and €10.9bn in TLTRO-II repayments, so that excess liquidity would rise closer to the €3tn mark. pic.twitter.com/ikjvAtQ8Av

In a recent speech, ECB Executive Board Member Isabel Schnabel pointed out that climate change is a market failure. She said that collective action, including by the ECB, should correct this market failure and accelerate the transition towards a carbon-neutral economy.

Asked about the Green TLTRO report by MEP Bas Eickhout, ECB President Lagarde said that “climate change has to be part and parcel of our strategy review. Not because it is a secondary objective, but because of its impact on price stability, because of its significant impact on risk assessment and risk management. And the Green TLTRO, as you called it, is a matter that is of interest and that we will look at.”

What volume of green loans should the ECB target during the first 3 years? How low should the interest rate on Green TLTRO be? Should the eligible bank assets include loans to households for house purchases, a category that is currently exluded from TLTRO?

In a webinar on 12 October 2020, Jens van ‘t Klooster discusses the Green TLTRO proposal with Isabel Vansteenkiste (ECB) and Frederik Ducrozet (Pictet).

Update 2020/10/18: this is the video

Full disclosure: I have done consulting work for this report.

So if you want to convince me of your financial panacea, show me what it means in practice. Who are the winners and losers? What are the consequences of your plan for households, companies, banks, government finances, inflation, employment?

Supply shock is what armchair economists talk about, because it sounds complicated and smart. The real danger is a fall in demand. Central banks and governments should act now.https://t.co/GFNyyWTJzLhttps://t.co/1xkE32D5qj

This is the bottom line. This is an exogenous shock that creates Knightian uncertainty and will likely increase savings rates and risk aversion. The optimal response is for governments/CBs to forcefully and preemptively offset the increase in private risk. Whatever it takes. https://t.co/zYM8qfLfIx

This notion that Fed has "limited ammunition" is by collective public choice. Fed/Treasury could/should underwrite bank lending to small/med businesses with (hopefully) temporary cash-flow problem and skittish creditors. https://t.co/1lxYrvzvMB

There are hundreds, if not thousands, of economists in good standing throughout the Fed, academia, and private forecasting, all discussing a *demand* shock.

To respond to us with "you can't solve a *supply* shock with demand-side tools" is a malicious mischaracterization.

This reminds me of a historical paper I wrote on how the Bank of France smoothed the negative impact of a negative supply supply shock not by interest rate cut but by making more counterparties eligibility to the discount window. A thread & the paper https://t.co/G3JKjcAMDdhttps://t.co/GRpnVq1cdS

Eulogy by Aya Sissoko, President of the ECB, 8 January 2076

It is with great sadness that we say farewell to our honorary President and dear friend Christine Lagarde today.

Madame Lagarde will be fondly remembered as the fourth President of the European Central Bank, the predecessor of the Euro Central Bank.

Christine became President during a protracted malaise in the euro area. By throwing off the yoke of false dogma, she revitalized the ECB. Her curiosity, vision and political prowess changed the course of history.

Under her leadership, the ECB showed the world how to handle the climate transition. At the same time, the euro economy grew at a rate previously believed to be impossible.

Ask any of the Seven Bankers, and they will all agree: Christine was the first modern central banker. Her autobiography, published 30 years ago, is still a must-read.

Christine’s career set the gold standard for our profession. Not just for what she did during her presidency, but also for what she didn’t do.

Her resignation in the wake of the Crisis of 2033 was a clear statement against the all-powerful central banker. During her retirement, Christine refrained from commenting on current events.

Christine, Madame Lagarde, you were born Lallouette – the lark – but you will always be The Owl of Frankfurt.

On behalf of the 1.4 billion people who use the euro every day,

What do crypto enthousiasts have in common with defenders of independent central banks?

Based on the “Buy Bitcoin”-replies to ECB/Fed tweets, it seems the answer is “not much”.

However, that’s incorrect. Both groups think that their projects are apolitical.

Many central bankers view themselves as technocrats, divorced from politics.

But that’s a fantasy.

You see, anything a central bank does – even within its mandate – has political consequences.

Should monetary policy take into account climate change?

Should the central bank change interest rates or do QE to reach its inflation goal? Whatever option is chosen, monetary policy has distributional effects. For example, the German government has saved hundreds of billions in interest costs.

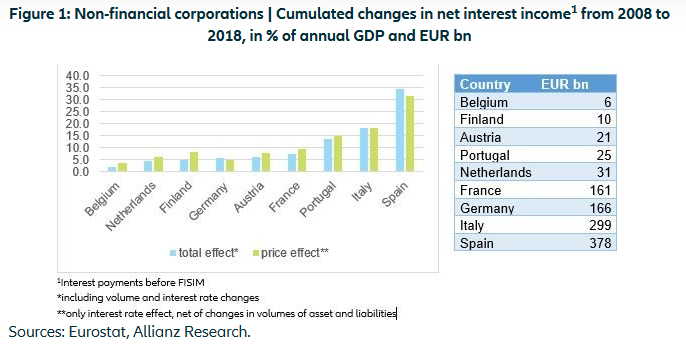

European non-financial corporations have benefited from low interest rates. Source

These two dilemmas illustrate that central banking is inherently political.

Therefore, economists should calculate the consequences of different monetary policy options. These scenarios will make the politics of the central bank’s actions explicit. For example, I estimated the effect of deeply negative interest rates (a proposal of Miles Kimball) on banks, governments, the ECB and the private sector.

Especially in the euro area, the ECB should take differences in asset mixes between countries into account.

Increased transparency will enable central bankers to defend monetary policy against criticism.

Update 26 January 2020: my arguments are obviously not new, see for example:

"Politics is built into central banking. […) Monetary policy choices may not be as politically divisive as war or welfare programmes, but they are too controversial ever to be purely technocratic." Heterox ideas 5 y ago, common view today. Great article also https://t.co/r3TkhkNlVu