Hello and welcome to another episode of the Finrestra podcast! I’m Jan Musschoot.

Summer is almost over, but I wanna start September with some economic thoughts inspired by my vacation in Denmark.

One of the things I noticed during my week in Copenhagen was the vast number of American tourists. For example, I went on a guided walking tour through the city center, and almost everyone in the group was American, and more specifically Californian. In restaurants, we frequently sat next to Americans. It’s remarkable when you think about it—flying from the US to Copenhagen, and especially from the West Coast, takes about ten hours. Meanwhile, there are like 500 million potential tourists in Europe who are much closer. For me, it was just a one hour flight.

So why are there so many Americans in Copenhagen relative to Europeans? Although Copenhagen is a beautiful city, Denmark is quite expensive, so many European tourists prefer cheaper options. On the other hand, I know there are also lots of Americans in places like Portugal, France and Italy.

So going on vacation in Europe must be quite cheap to Americans. And the real question is:

Why are Americans richer than Europeans (on average)?

Strong dollar?

When you think about tourism, one obvious explanation is the exchange rate. A strong dollar against the euro means Americans can buy more euros, making Europe relatively cheaper. While this sounds like a reasonable explanation, the five-year exchange rate between the dollar and the euro doesn’t support this. There was a period in 2022 when the euro was weak, but today, the exchange rate is similar to pre-pandemic levels in 2019.

The US dollar was strong in 2022, but is back to 2019 levels (pre-pandemic)

So, this isn’t the main reason for the large number of American tourists. And if you’re thinking, hold on, Denmark isn’t in the eurozone and uses the Danish krone, the Danish National Bank keeps the exchange rate between the euro and the crown fixed.

However, a strong dollar can influence tourism. The Japanese yen has weakened significantly compared to the dollar. I wouldn’t be surprised if more Americans are visiting Japan now because their dollars go much further there.

The US dollar is strong compared to the yen, making Japan cheap for American tourists

So, if the exchange rate isn’t the reason why Americans are richer, what is? Because regardless of the metric—whether it’s GDP per capita, purchasing power parity, or other indicators—Americans are indeed richer than Europeans on average.

Lower taxes

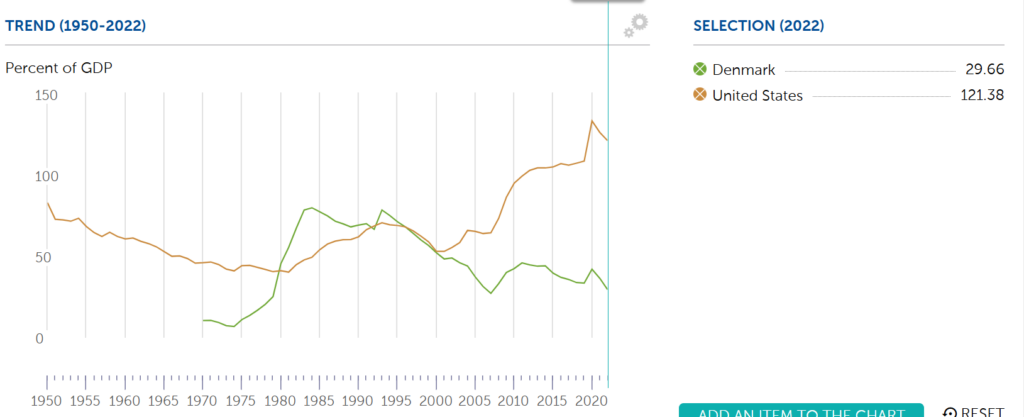

One major factor contributing to this wealth difference is higher deficits and lower taxes in the U.S.. In the U.S., government deficits have been high since the financial crisis of 2008, leading to a government debt-to-GDP ratio above 120%. In contrast, Denmark has a public debt ratio below 30%, thanks to high taxes and small deficits or even budget surpluses.

Government debt-to-GDP ratio for Denmark and the US. Source: IMF

While Denmark invests heavily in public infrastructure, one of the reasons why it’s such a nice place to visit, this spending is funded by taxes rather than debt. Meanwhile, in the U.S., people benefit from lower taxes, leading to higher incomes.

If Denmark borrowed more and ran budget deficits instead of surpluses, people would have more money to spend, save, or invest, benefiting the Danish and European economy. Lower taxes on income or consumption would give people more disposable income, allowing them to make investments, improve their homes, or travel more—just like many Americans do.

OK, that’s it for this week’s episode. I’ll do another one about Denmark later, because I haven’t said anything about its biggest company yet.

This episode is not sponsored by Danish Tourism, but if you visit Copenhagen, I highly recommend you buy a Copenhagen card.

The war in Ukraine, the rise of China, economic stagnation, and deteriorating relations with Africa are some of Europe’s most pressing geopolitical challenges.

In this episode, I talk about how banks reflect these geopolitical shifts.

Until the 2022 invasion of Ukraine, EU politicians and bankers treated Russia like any other Central and Eastern European country. Banks like UniCredit, Raiffeisen Bank International, Société Générale and others had significant subsidiaries in Russia, just as they had in e.g. the Czech Republic, Poland or Bulgaria.

Vice versa, Russian banks did business in Europe.

However, since the invasion, all but one Russian bank in the EU have been forced to shut down. In contrast, European banks continue to operate in Russia, to the chagrin of European and American officials.

As the visit of Xi Jinping to Hungary and Serbia demonstrates, good political relations and Chinese investment go hand in hand. Usually, the larger a country’s GDP, the more foreign banks it attracts. But although Hungary has a small economy, it has more Chinese banks than e.g. Austria, Sweden or Romania.

Macron talked about the need for cross-border consolidation of European banks. It’s easy to suspect ulterior motives, as BNP Paribas and Crédit Agricole are well placed to buy foreign competitors. But given the single European market, the dominance of local banks in the biggest euro countries doesn’t seem right.

Finally, as France’s military and political power in Africa wanes, French banks have been selling their African subsidiaries to local banks.

Future episodes will be about how to sell SocGen, the effect of higher interest rates, and the frozen Russian central bank assets at Euroclear.

Transcript/blog version:

Hello and welcome to another season of the Finrestra Podcast!

I’ve been on hiatus for more than a year, but now I’m back with a lot of new content. But more on that at the end of this episode.

Today’s topic is the geopolitics of banking. I’m gonna talk about foreign banks in Europe and European banks in the rest of the world based on presidents Putin, Xi and Macron.

So first of all, Vladimir Putin.

Since Putin’s invasion of Ukraine in 2022, a lot has changed for banks, both for Russian banks in Europe and for European banks in Russia.

Almost immediately after the invasion, Russian banks in Europe were sanctioned or they suffered bank runs, and then the European regulators shut them down.

Sberbank, the largest Russian bank, had a number of subsidiaries in Central Europe. It had bought these from Austrian Volksbank in 2012, at a time when Russia was still seen as a “normal” country.

Russia’s second largest bank, VTB, was also active in a couple of European countries before the war. Those operations are liquidated.

But there were also some smaller Russian banks that you probably never heard of.

For example, the fourth largest bank on Cyprus was RCB, formerly known as Russian Commercial Bank. RCB doesn’t exist anymore.

In the Netherlands, there was Amsterdam Trade Bank. Despite the name, it was owned by Russian Alfa Bank. Amsterdam Trade Bank was sanctioned and then closed.

Recently, in Luxembourg, the East-West United Bank was also closed down. East-West United Bank started as a Soviet bank during the Cold War, but its story ended thanks to Putin and the European sanctions.

Luxembourg is also the only country in the EU that still has an active Russian bank, Gazprombank. The EU is still buying gas from Russia, and the payments go through Gazprombank.

So that covers the Russian banks in the EU.

If we look at the European banks in Russia, the story is quite different.

Maybe I should start with the situation before the invasion.

According to the Russian central bank, there were three European banks with significant operations in Russia: UniCredit, Raiffeisen Bank International and Société Générale.

Intesa Sanpaolo, OTP, ING and a couple of others also did business there.

These are all banks who had expanded not just into Russia, but also into other former communist countries like Poland, the Czech Republic or Bulgaria.

Of these European banks, only Société Générale has fully left Russia.

It’s funny that I didn’t read any warnings from Yellen to JPMorgan and Citibank, who also still operate in Moscow.

I guess it shows you who’s the boss in international politics and finance.

Geopolitics aside, you can question the wisdom of selling a profitable bank to a friend of Putin.

But given the fate of the Russian banks in Europe, it’s strange that the Western ones can still do business in Russia.

Maybe it’s for propaganda: unlike the West, Russia respects the rule of law.

Or it could be because they’re useful for facilitating international payments.

Or maybe Putin believes that European bankers can influence politics.

That would be pretty naive.

In Europe, politicians are much more powerful than bankers (see Brexit).

It’s probably more likely that Putin thinks it’s good to retain some leverage over Western banks, because billions of euros of the Russian Central Bank are frozen in the EU.

Western politicians want to use that money for Ukraine, so Putin could retaliate by nationalizing their banks.

So that was the Putin chapter of this banking and geopolitics episode.

Next, let’s move on to China.

Xi Jinping, the Chinese president, was in Europe last month.

He visited three countries: France, Hungary and Serbia.

France is a logical destination: it’s the second largest economy in the EU, and the only one with nuclear weapons.

But why did Xi go to Hungary and Serbia?

Well, obviously because they have the best political relations with China.

And those relations result in Chinese investment: from BYD factories in Hungary, mines in Serbia and the railway between Budapest and Belgrade.

What’s the geopolitical banking angle here?

If you’re a Chinese company that’s gonna invest abroad, why would you depend on Western banks?

It’s more convenient to deal with banks that you know, and who speak your language.

So there are two Chinese banks in Hungary: China Construction Bank and Bank of China. Bank of China even has a regional headquarters in Budapest. And it has a branch in Belgrade.

For comparison, there’s only one Chinese bank in countries like Austria, Sweden, Ireland and Romania, who have much larger economies than Hungary and especially Serbia.

But taking into account the geopolitics explains why Hungary and Serbia are outliers: Chinese banks are attracted by more than GDP alone.

Now with all of this talk about two small countries, I don’t want to give you the impression that Chinese banks only follow geopolitics.

In fact, there are five major Chinese banks in Paris and Frankfurt, so the “law” of financial geography does apply.

However, here’s a fun fact: the EU country with most Chinese banks is not France or Germany, but… tiny Luxembourg.

That’s for another episode.

So that was the story of Xi Jinping and the Chinese banks in Europe.

What about European banks in China?

China’s economy relies almost entirely on its own domestic banks.

European banks do more business in Hong Kong than in mainland China, a country with more than a billion people.

Compared to making cars or chips, banking is pretty simple. So the Chinese didn’t need foreign banks to learn how to run their banks.

Finally, I wanna talk about Emmanuel Macron, the French president.

Macron recently talked to Bloomberg about the need for cross-European banks.

Personally, I don’t believe that should be a political target.

The banking union is an obsession of people in Brussels. But it won’t help the economy of the EU.

Although I have to say, I’m not surprised that Macron, a former Rothschild banker, is pushing for cross-border bank mergers in the EU.

BNP Paribas and Crédit Agricole, the two largest banks in the EU, are French.

So they are in pole position to consolidate the industry in Europe.

But if we give Macron the benefit of the doubt, who doesn’t just want to create French banking empires, he actually does have a point.

In the big five euro countries, Germany, France, Italy, Spain and the Netherlands, the biggest banks are all domestic players.

In contrast, Central and Eastern Europe is much closer to Macron’s pan-European vision.

Their banking systems are a mix of foreign and domestic banks.

There are some financial and historical reasons for this difference between East and West.

A top bank in a small economy might cost a couple of billion euros, while a similar bank in a large country could cost an order of magnitude more.

So twenty years ago, Western banks bought banks in Eastern Europe, where GDP was much lower than it is today.

A similar expansion in the West would have been extremely capital intensive.

For example, Dutch ABN AMRO was valued at 71 billion euros when it was acquired in 2007.

The 1990s and 2000s were also a period of geopolitical optimism and openness to foreign investment.

But in 2024, politicians wouldn’t be happy that foreigners buy the local banking champions, even if they’re from other EU members.

Remember that this episode is about geopolitics.

If any ‘Western’ banks have enough capital to buy big French banks, it’s the Americans or Canadians.

And although the US and Canada are his NATO allies, there’s no way Macron would give JPMorgan permission to buy BNP Paribas.

In fact, when the journalist asked if Macron would agree with the sale of Société Générale, the French President said “Dealing as Europeans means you need consolidation as Europeans.”

In the interview, they suggested Santander as the buyer.

That wouldn’t be my suggestion. I’ll do another podcast episode about how I would sell SocGen.

OK, so that’s about France and French banks in Europe.

Finally I wanna comment on France and its banks in Africa.

Belgium (Antwerp) is Europe's largest diamond importer ($8.6 billion in 2020, of which $1.5 billion from Russia). Only a handful of countries mine diamonds. https://t.co/AK9dhgzC0Epic.twitter.com/THAXFkpqXn

All high debt Eurozone economies continue to reduce public debt at a pace exceeding that required by the existing fiscal rules – even France (just about) 😱

Another problem of the EPCs is that they are not harmonized across the EU. Thresholds and criteria are determined at the national level, creating major issues of comparability across countries. This is of course a problem for those who want to use EPCs as a proxy for risk. 8/12 pic.twitter.com/LYvu7Vu39I

#Chart These charts show that fiscal support measures in the euro area were mostly untargeted and that public investment was very low. 18/19 pic.twitter.com/oqbB5s2Bx6

The SNB reported a loss of CHF132 bn in 2022, of which CHF131 bn came from losses on foreign currency positions. This is by far the largest loss on record. pic.twitter.com/UbykA8QNa1

Signs are emerging of diversification in global solar PV supply chains, with the US & India set to boost investment in solar manufacturing by up to $25 billion in the next 5 years

China remains the dominant player, but its global share may decrease from 90% today to 75% by 2027 pic.twitter.com/GJrBUTN0Z5

Hello and welcome to another episode of the Finrestra Podcast! (Apple, Spotify, YouTube)

I am Jan Musschoot.

Warren Buffett once said: “Only when the tide goes out do you discover who’s been swimming naked.”

And boy, have people been swimming naked in 2022!

Investors saw the valuations of tech companies crash by 50, 70 or even more than 90%.

The so-called “geopolitical” European Commission – who wants the EU to be the first climate neutral continent – had to beg for gas around the world after boycotting Russia.

But the naked swimmer that I want to focus on is the ECB, a favorite of this podcast.

This is what Lagarde said about inflation at the end of 2021:

So inflation was supposed to have been a hump, gradually coming down to the 2 percent target over the course of 2022.

But in fact, inflation had been too high since the summer of 2021, and it basically kept on going up for the entirety of 2022. In December of 2022, it dropped a little, but it was still 9.2 percent according to Eurostat.

The ECB’s economists have been worried a lot about inflation expectations and wage-price spirals.

But nominal wage growth has recently accelerated. Whether future wage agreements will lead to a wage-price spiral ultimately depends on monetary policy. If long-term inflation expectations remain anchored, the risks of a wage-price spiral will be limited. 9/15 pic.twitter.com/x1I8czqSw2

But what’s been driving Europe’s inflation for more than a year has been the cost of energy. It’s not clear at all how the metrics that central banks usually look at are relevant for this kind of inflation. I did some research last year that showed that if you look at government deficits, the unemployment rate, or the central bank interest rate, these are basically irrelevant when it comes to predicting the inflation that we observed.

What’s mostly correlated to the current inflation is the amount of energy economies use relative to their size. In other words, energy intensity is what drives inflation.

And when it comes to energy, the ECB has screwed up. Yes, central bankers made a lot of speeches about climate change since Lagarde is in charge. But I can’t heat my home with speeches and tweets.

If the ECB had funded investments to make us less dependent on imported fossil fuels, inflation would have been much lower.

Imagine that the EU had invested massively in building renovation, heat pumps and clean energy sources while inflation was below target.

This would have reduced our vulnerability to Russia and other geopolitical rivals.

And fossil fuels would be a much smaller part of the consumer price index.

On top of that, Europe’s industry would have plenty of cheap energy right now…

So energy-driven inflation was the first tide that showed that the ECB was swimming naked.

But this exposes the ECB to another problem, which is the mismatch between its assets and liabilities. While inflation was below target, the ECB bought trillions of euros of bonds. A lot of these have a fixed, negative yield. Under the PEPP, the pandemic emergency purchase program, the ECB put a turbo on this QE.

And how were these bond purchases funded? With bank deposits.

Now what happens when interest rates go up? The central bank starts to pay interest on these bank deposits, while its assets have a fixed yield.

According to one estimate, the Eurosystem is going to lose about 600 billion euro because of this failing risk management.

Anyone with a basic grasp of finance could have predicted this.

I even told the ECB to issue bonds instead of funding their assets with reserves.

Of course, they didn’t listen, because they’re so smart…

And what’s extra sad, is that the ECB has been complaining that governments haven’t invested enough in infrastructure.

Central bankers also complain about how untargeted government relief to help citizens and companies with their energy bills contributes to inflation.

#Chart These charts show that fiscal support measures in the euro area were mostly untargeted and that public investment was very low. 18/19 pic.twitter.com/oqbB5s2Bx6

The problem is again that the ECB didn’t put its money where its mouth was.

For years, QE has kept government funding costs in check, without any conditions on how governments should spend to keep inflation in check.

Maybe as a serious, non-political central bank, the ECB should have actually made sure that these crucial investments got done?

Instead, the ECB basically acted as a financial speculator, counting on low inflation and low interest rates forever.

Again, just imagine that the ECB would have invested not in securities, but in real infrastructure over the past decade.

How much better off Europe would be right now!

The final tide that went out in 2022 is that of Lagarde’s leadership.

Everybody knows that she’s not an economist. So maybe we shouldn’t blame her for failing to anticipate the inflation or the financial losses.

But she was previously a minister in France and the head of the International Monetary Fund.

So she must be a strong leader, right?

For those of you who’ve been listening to the podcast for a while, you might remember what I wrote in my New Year’s letter to Lagarde a year ago.

I suggested that either she quit, or she starts doing her job.

Obviously she’s still the President, so she didn’t quit.

But as the President, she should have fired the people who’ve been feeding her false predictions for all of this time.

At the end of 2021, ECB staff projected that euro area inflation would be about 3% in 2022. And core inflation would be below 2%.

🇪🇺 New @ecb staff projections. Key figures: 3.2% inflation in 2022 (!), but headline and core inflation at 1.8%, close to but *below* 2% target. pic.twitter.com/Y5On3eIPsv

I don’t know if it’s even possible for Lagarde to fire the most high profile economists like Isabel Schnabel or Philip Lane. But you’d expect some heads to roll.

Now before I go, I want to thank everybody who has supported this podcast and my YouTube channel. It’s not always easy to combine this with my other work, but I do appreciate your feedback!

In the coming year, I’m planning to release one podcast episode per month. And I want to do about a dozen deep dives into central banking and the financial system on the Finrestra Youtube channel.

So if you want to keep informed, please subscribe!

This has been another episode of the Finrestra podcast.

Although I didn’t reach that target, I am quite pleased with the progress I made. Especially given that the first half of 2022 was so busy that I could hardly create any new videos.

Some videos did well, others didn’t get the number of views that I expected they would get. That’s life…

One of the features of YouTube is that your content can suddenly be picked up by the algorithm, even when it has been posted months earlier. For me, that a big advantage compared to social networks like Twitter and LinkedIn.

In 2023, I hope to be able to create about a dozen ‘deep dive’ videos, like the one on inflation and the one on interest rates.

In addition, I’d like to make a podcast episode every month (minus the summer holidays).

Rather than maximize the number of views, it would be great if I can get more watch time. Currently, my most popular video has been watched for 150 hours.

If I can create 10 videos that get watched 200 hours or more in 2023, I’ll be very happy 🙂