Hello and welcome to another episode of the Finrestra podcast! I’m Jan Musschoot.

Summer is almost over, but I wanna start September with some economic thoughts inspired by my vacation in Denmark.

One of the things I noticed during my week in Copenhagen was the vast number of American tourists. For example, I went on a guided walking tour through the city center, and almost everyone in the group was American, and more specifically Californian. In restaurants, we frequently sat next to Americans. It’s remarkable when you think about it—flying from the US to Copenhagen, and especially from the West Coast, takes about ten hours. Meanwhile, there are like 500 million potential tourists in Europe who are much closer. For me, it was just a one hour flight.

So why are there so many Americans in Copenhagen relative to Europeans? Although Copenhagen is a beautiful city, Denmark is quite expensive, so many European tourists prefer cheaper options. On the other hand, I know there are also lots of Americans in places like Portugal, France and Italy.

So going on vacation in Europe must be quite cheap to Americans. And the real question is:

Why are Americans richer than Europeans (on average)?

Strong dollar?

When you think about tourism, one obvious explanation is the exchange rate. A strong dollar against the euro means Americans can buy more euros, making Europe relatively cheaper. While this sounds like a reasonable explanation, the five-year exchange rate between the dollar and the euro doesn’t support this. There was a period in 2022 when the euro was weak, but today, the exchange rate is similar to pre-pandemic levels in 2019.

The US dollar was strong in 2022, but is back to 2019 levels (pre-pandemic)

So, this isn’t the main reason for the large number of American tourists. And if you’re thinking, hold on, Denmark isn’t in the eurozone and uses the Danish krone, the Danish National Bank keeps the exchange rate between the euro and the crown fixed.

However, a strong dollar can influence tourism. The Japanese yen has weakened significantly compared to the dollar. I wouldn’t be surprised if more Americans are visiting Japan now because their dollars go much further there.

The US dollar is strong compared to the yen, making Japan cheap for American tourists

So, if the exchange rate isn’t the reason why Americans are richer, what is? Because regardless of the metric—whether it’s GDP per capita, purchasing power parity, or other indicators—Americans are indeed richer than Europeans on average.

Lower taxes

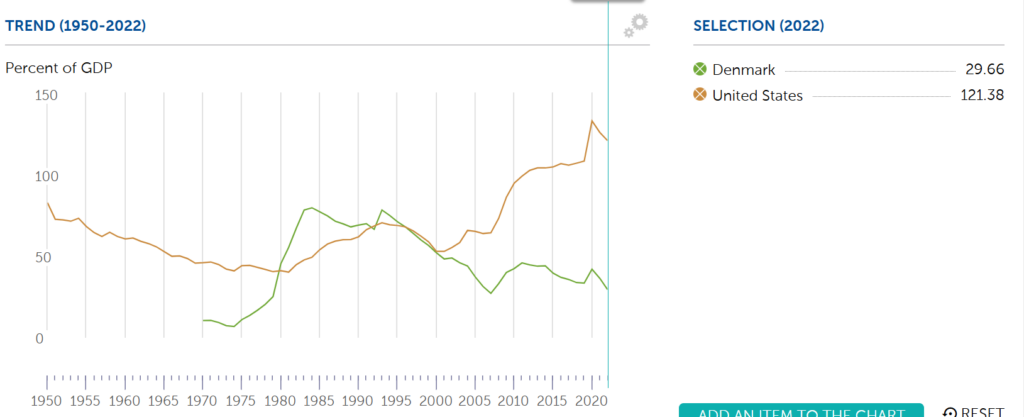

One major factor contributing to this wealth difference is higher deficits and lower taxes in the U.S.. In the U.S., government deficits have been high since the financial crisis of 2008, leading to a government debt-to-GDP ratio above 120%. In contrast, Denmark has a public debt ratio below 30%, thanks to high taxes and small deficits or even budget surpluses.

Government debt-to-GDP ratio for Denmark and the US. Source: IMF

While Denmark invests heavily in public infrastructure, one of the reasons why it’s such a nice place to visit, this spending is funded by taxes rather than debt. Meanwhile, in the U.S., people benefit from lower taxes, leading to higher incomes.

If Denmark borrowed more and ran budget deficits instead of surpluses, people would have more money to spend, save, or invest, benefiting the Danish and European economy. Lower taxes on income or consumption would give people more disposable income, allowing them to make investments, improve their homes, or travel more—just like many Americans do.

OK, that’s it for this week’s episode. I’ll do another one about Denmark later, because I haven’t said anything about its biggest company yet.

This episode is not sponsored by Danish Tourism, but if you visit Copenhagen, I highly recommend you buy a Copenhagen card.

The war in Ukraine, the rise of China, economic stagnation, and deteriorating relations with Africa are some of Europe’s most pressing geopolitical challenges.

In this episode, I talk about how banks reflect these geopolitical shifts.

Until the 2022 invasion of Ukraine, EU politicians and bankers treated Russia like any other Central and Eastern European country. Banks like UniCredit, Raiffeisen Bank International, Société Générale and others had significant subsidiaries in Russia, just as they had in e.g. the Czech Republic, Poland or Bulgaria.

Vice versa, Russian banks did business in Europe.

However, since the invasion, all but one Russian bank in the EU have been forced to shut down. In contrast, European banks continue to operate in Russia, to the chagrin of European and American officials.

As the visit of Xi Jinping to Hungary and Serbia demonstrates, good political relations and Chinese investment go hand in hand. Usually, the larger a country’s GDP, the more foreign banks it attracts. But although Hungary has a small economy, it has more Chinese banks than e.g. Austria, Sweden or Romania.

Macron talked about the need for cross-border consolidation of European banks. It’s easy to suspect ulterior motives, as BNP Paribas and Crédit Agricole are well placed to buy foreign competitors. But given the single European market, the dominance of local banks in the biggest euro countries doesn’t seem right.

Finally, as France’s military and political power in Africa wanes, French banks have been selling their African subsidiaries to local banks.

Future episodes will be about how to sell SocGen, the effect of higher interest rates, and the frozen Russian central bank assets at Euroclear.

Transcript/blog version:

Hello and welcome to another season of the Finrestra Podcast!

I’ve been on hiatus for more than a year, but now I’m back with a lot of new content. But more on that at the end of this episode.

Today’s topic is the geopolitics of banking. I’m gonna talk about foreign banks in Europe and European banks in the rest of the world based on presidents Putin, Xi and Macron.

So first of all, Vladimir Putin.

Since Putin’s invasion of Ukraine in 2022, a lot has changed for banks, both for Russian banks in Europe and for European banks in Russia.

Almost immediately after the invasion, Russian banks in Europe were sanctioned or they suffered bank runs, and then the European regulators shut them down.

Sberbank, the largest Russian bank, had a number of subsidiaries in Central Europe. It had bought these from Austrian Volksbank in 2012, at a time when Russia was still seen as a “normal” country.

Russia’s second largest bank, VTB, was also active in a couple of European countries before the war. Those operations are liquidated.

But there were also some smaller Russian banks that you probably never heard of.

For example, the fourth largest bank on Cyprus was RCB, formerly known as Russian Commercial Bank. RCB doesn’t exist anymore.

In the Netherlands, there was Amsterdam Trade Bank. Despite the name, it was owned by Russian Alfa Bank. Amsterdam Trade Bank was sanctioned and then closed.

Recently, in Luxembourg, the East-West United Bank was also closed down. East-West United Bank started as a Soviet bank during the Cold War, but its story ended thanks to Putin and the European sanctions.

Luxembourg is also the only country in the EU that still has an active Russian bank, Gazprombank. The EU is still buying gas from Russia, and the payments go through Gazprombank.

So that covers the Russian banks in the EU.

If we look at the European banks in Russia, the story is quite different.

Maybe I should start with the situation before the invasion.

According to the Russian central bank, there were three European banks with significant operations in Russia: UniCredit, Raiffeisen Bank International and Société Générale.

Intesa Sanpaolo, OTP, ING and a couple of others also did business there.

These are all banks who had expanded not just into Russia, but also into other former communist countries like Poland, the Czech Republic or Bulgaria.

Of these European banks, only Société Générale has fully left Russia.

It’s funny that I didn’t read any warnings from Yellen to JPMorgan and Citibank, who also still operate in Moscow.

I guess it shows you who’s the boss in international politics and finance.

Geopolitics aside, you can question the wisdom of selling a profitable bank to a friend of Putin.

But given the fate of the Russian banks in Europe, it’s strange that the Western ones can still do business in Russia.

Maybe it’s for propaganda: unlike the West, Russia respects the rule of law.

Or it could be because they’re useful for facilitating international payments.

Or maybe Putin believes that European bankers can influence politics.

That would be pretty naive.

In Europe, politicians are much more powerful than bankers (see Brexit).

It’s probably more likely that Putin thinks it’s good to retain some leverage over Western banks, because billions of euros of the Russian Central Bank are frozen in the EU.

Western politicians want to use that money for Ukraine, so Putin could retaliate by nationalizing their banks.

So that was the Putin chapter of this banking and geopolitics episode.

Next, let’s move on to China.

Xi Jinping, the Chinese president, was in Europe last month.

He visited three countries: France, Hungary and Serbia.

France is a logical destination: it’s the second largest economy in the EU, and the only one with nuclear weapons.

But why did Xi go to Hungary and Serbia?

Well, obviously because they have the best political relations with China.

And those relations result in Chinese investment: from BYD factories in Hungary, mines in Serbia and the railway between Budapest and Belgrade.

What’s the geopolitical banking angle here?

If you’re a Chinese company that’s gonna invest abroad, why would you depend on Western banks?

It’s more convenient to deal with banks that you know, and who speak your language.

So there are two Chinese banks in Hungary: China Construction Bank and Bank of China. Bank of China even has a regional headquarters in Budapest. And it has a branch in Belgrade.

For comparison, there’s only one Chinese bank in countries like Austria, Sweden, Ireland and Romania, who have much larger economies than Hungary and especially Serbia.

But taking into account the geopolitics explains why Hungary and Serbia are outliers: Chinese banks are attracted by more than GDP alone.

Now with all of this talk about two small countries, I don’t want to give you the impression that Chinese banks only follow geopolitics.

In fact, there are five major Chinese banks in Paris and Frankfurt, so the “law” of financial geography does apply.

However, here’s a fun fact: the EU country with most Chinese banks is not France or Germany, but… tiny Luxembourg.

That’s for another episode.

So that was the story of Xi Jinping and the Chinese banks in Europe.

What about European banks in China?

China’s economy relies almost entirely on its own domestic banks.

European banks do more business in Hong Kong than in mainland China, a country with more than a billion people.

Compared to making cars or chips, banking is pretty simple. So the Chinese didn’t need foreign banks to learn how to run their banks.

Finally, I wanna talk about Emmanuel Macron, the French president.

Macron recently talked to Bloomberg about the need for cross-European banks.

Personally, I don’t believe that should be a political target.

The banking union is an obsession of people in Brussels. But it won’t help the economy of the EU.

Although I have to say, I’m not surprised that Macron, a former Rothschild banker, is pushing for cross-border bank mergers in the EU.

BNP Paribas and Crédit Agricole, the two largest banks in the EU, are French.

So they are in pole position to consolidate the industry in Europe.

But if we give Macron the benefit of the doubt, who doesn’t just want to create French banking empires, he actually does have a point.

In the big five euro countries, Germany, France, Italy, Spain and the Netherlands, the biggest banks are all domestic players.

In contrast, Central and Eastern Europe is much closer to Macron’s pan-European vision.

Their banking systems are a mix of foreign and domestic banks.

There are some financial and historical reasons for this difference between East and West.

A top bank in a small economy might cost a couple of billion euros, while a similar bank in a large country could cost an order of magnitude more.

So twenty years ago, Western banks bought banks in Eastern Europe, where GDP was much lower than it is today.

A similar expansion in the West would have been extremely capital intensive.

For example, Dutch ABN AMRO was valued at 71 billion euros when it was acquired in 2007.

The 1990s and 2000s were also a period of geopolitical optimism and openness to foreign investment.

But in 2024, politicians wouldn’t be happy that foreigners buy the local banking champions, even if they’re from other EU members.

Remember that this episode is about geopolitics.

If any ‘Western’ banks have enough capital to buy big French banks, it’s the Americans or Canadians.

And although the US and Canada are his NATO allies, there’s no way Macron would give JPMorgan permission to buy BNP Paribas.

In fact, when the journalist asked if Macron would agree with the sale of Société Générale, the French President said “Dealing as Europeans means you need consolidation as Europeans.”

In the interview, they suggested Santander as the buyer.

That wouldn’t be my suggestion. I’ll do another podcast episode about how I would sell SocGen.

OK, so that’s about France and French banks in Europe.

Finally I wanna comment on France and its banks in Africa.

Hello and welcome to another episode of the Finrestra Podcast! (Apple, Spotify, YouTube)

I am Jan Musschoot.

Warren Buffett once said: “Only when the tide goes out do you discover who’s been swimming naked.”

And boy, have people been swimming naked in 2022!

Investors saw the valuations of tech companies crash by 50, 70 or even more than 90%.

The so-called “geopolitical” European Commission – who wants the EU to be the first climate neutral continent – had to beg for gas around the world after boycotting Russia.

But the naked swimmer that I want to focus on is the ECB, a favorite of this podcast.

This is what Lagarde said about inflation at the end of 2021:

So inflation was supposed to have been a hump, gradually coming down to the 2 percent target over the course of 2022.

But in fact, inflation had been too high since the summer of 2021, and it basically kept on going up for the entirety of 2022. In December of 2022, it dropped a little, but it was still 9.2 percent according to Eurostat.

The ECB’s economists have been worried a lot about inflation expectations and wage-price spirals.

But nominal wage growth has recently accelerated. Whether future wage agreements will lead to a wage-price spiral ultimately depends on monetary policy. If long-term inflation expectations remain anchored, the risks of a wage-price spiral will be limited. 9/15 pic.twitter.com/x1I8czqSw2

But what’s been driving Europe’s inflation for more than a year has been the cost of energy. It’s not clear at all how the metrics that central banks usually look at are relevant for this kind of inflation. I did some research last year that showed that if you look at government deficits, the unemployment rate, or the central bank interest rate, these are basically irrelevant when it comes to predicting the inflation that we observed.

What’s mostly correlated to the current inflation is the amount of energy economies use relative to their size. In other words, energy intensity is what drives inflation.

And when it comes to energy, the ECB has screwed up. Yes, central bankers made a lot of speeches about climate change since Lagarde is in charge. But I can’t heat my home with speeches and tweets.

If the ECB had funded investments to make us less dependent on imported fossil fuels, inflation would have been much lower.

Imagine that the EU had invested massively in building renovation, heat pumps and clean energy sources while inflation was below target.

This would have reduced our vulnerability to Russia and other geopolitical rivals.

And fossil fuels would be a much smaller part of the consumer price index.

On top of that, Europe’s industry would have plenty of cheap energy right now…

So energy-driven inflation was the first tide that showed that the ECB was swimming naked.

But this exposes the ECB to another problem, which is the mismatch between its assets and liabilities. While inflation was below target, the ECB bought trillions of euros of bonds. A lot of these have a fixed, negative yield. Under the PEPP, the pandemic emergency purchase program, the ECB put a turbo on this QE.

And how were these bond purchases funded? With bank deposits.

Now what happens when interest rates go up? The central bank starts to pay interest on these bank deposits, while its assets have a fixed yield.

According to one estimate, the Eurosystem is going to lose about 600 billion euro because of this failing risk management.

Anyone with a basic grasp of finance could have predicted this.

I even told the ECB to issue bonds instead of funding their assets with reserves.

Of course, they didn’t listen, because they’re so smart…

And what’s extra sad, is that the ECB has been complaining that governments haven’t invested enough in infrastructure.

Central bankers also complain about how untargeted government relief to help citizens and companies with their energy bills contributes to inflation.

#Chart These charts show that fiscal support measures in the euro area were mostly untargeted and that public investment was very low. 18/19 pic.twitter.com/oqbB5s2Bx6

The problem is again that the ECB didn’t put its money where its mouth was.

For years, QE has kept government funding costs in check, without any conditions on how governments should spend to keep inflation in check.

Maybe as a serious, non-political central bank, the ECB should have actually made sure that these crucial investments got done?

Instead, the ECB basically acted as a financial speculator, counting on low inflation and low interest rates forever.

Again, just imagine that the ECB would have invested not in securities, but in real infrastructure over the past decade.

How much better off Europe would be right now!

The final tide that went out in 2022 is that of Lagarde’s leadership.

Everybody knows that she’s not an economist. So maybe we shouldn’t blame her for failing to anticipate the inflation or the financial losses.

But she was previously a minister in France and the head of the International Monetary Fund.

So she must be a strong leader, right?

For those of you who’ve been listening to the podcast for a while, you might remember what I wrote in my New Year’s letter to Lagarde a year ago.

I suggested that either she quit, or she starts doing her job.

Obviously she’s still the President, so she didn’t quit.

But as the President, she should have fired the people who’ve been feeding her false predictions for all of this time.

At the end of 2021, ECB staff projected that euro area inflation would be about 3% in 2022. And core inflation would be below 2%.

🇪🇺 New @ecb staff projections. Key figures: 3.2% inflation in 2022 (!), but headline and core inflation at 1.8%, close to but *below* 2% target. pic.twitter.com/Y5On3eIPsv

I don’t know if it’s even possible for Lagarde to fire the most high profile economists like Isabel Schnabel or Philip Lane. But you’d expect some heads to roll.

Now before I go, I want to thank everybody who has supported this podcast and my YouTube channel. It’s not always easy to combine this with my other work, but I do appreciate your feedback!

In the coming year, I’m planning to release one podcast episode per month. And I want to do about a dozen deep dives into central banking and the financial system on the Finrestra Youtube channel.

So if you want to keep informed, please subscribe!

This has been another episode of the Finrestra podcast.

Hello and welcome to another episode of the Finrestra podcast! I am Jan Musschoot.

In this episode, I will talk about the sale of HSBC Canada and especially what HSBC can do with the cash it will receive from this sale. But first, let’s do a quick recap of the financial news of November.

FTX, a crypto trading platform, went bankrupt and its founder SBF went from being a multi-billionaire to essentially being broke.

In the euro area, inflation finally went down a little. Inflation was 10% in November whereas inflation was still 10.6 percent in October. Inflation is going down a little thanks to lower energy prices.

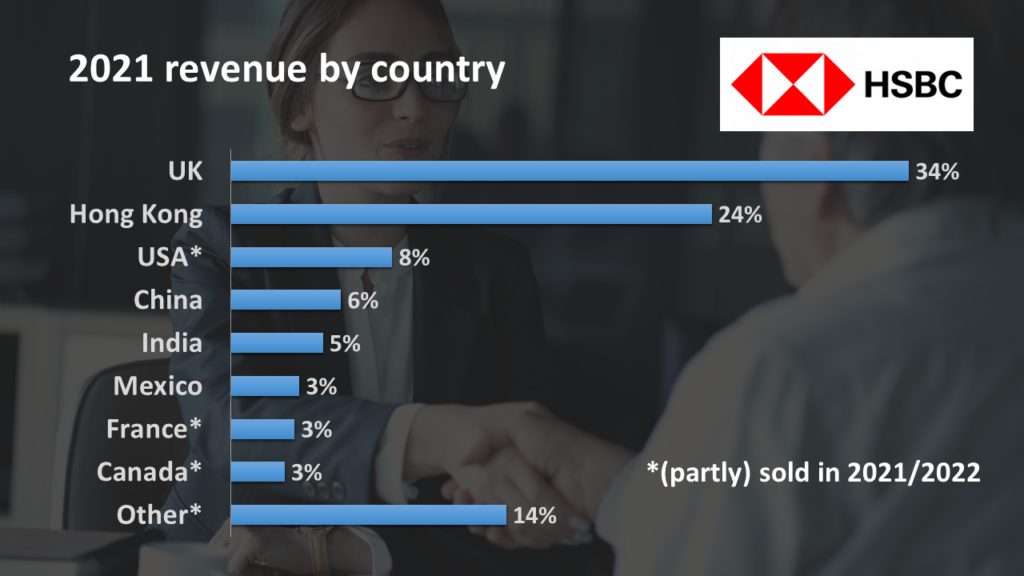

If you look at where HSBC derives its revenue from, Canada is barely three percent of revenue. It’s about four percent of profits and also four percent of the balance sheet. So banking in Canada is just a small part of the global group that is HSBC.

So it makes sense to exit this market, because you cannot have the scale you want to be highly profitable. Canada also has some big domestic banks who dominate banking in the country, so it makes sense for HSBC to exit the market, especially given that they received a good price for it.

This Go big or go home strategy is something that HSBC has been following for a few years now. For example, last year they also announced that they would exit [part of] the retail banking business in the US and that they would sell the French retail banking business, which was also about three percent of the group’s revenue. But they cannot compete to with the large French banks in France. And then in November 2022, so last month, HSBC also sold its bank in Oman (in the Middle East) to a local bank.

And this ‘let’s go big or go home’ strategy is not unique to HSBC. For instance last year I did a podcastepisode about the sale of Bank of the West by BNP Paribas. The French multinational bank sold its US retail banking division to focus more on its core markets. And that’s also what HSBC has been doing here with the sale of HSBC Canada.

In financial terms, it seems that HSBC has done a pretty good deal because they received 13.5 billion Canadian dollars (which is about 10 billion US dollars). That’s about eight percent of HSBC group’s market cap. So that’s actually a good deal. If you look into the financial statements, they say they will make a net profit of more than 5 billion dollars on this sale above the book value1. And of course, selling the Canadian division will also shrink HSBC’s assets by a little less than 100 billion US dollars. So the sale provides a good boost to the capital ratio of HSBC as well.

Now let’s focus on what HSBC could do with the cash that it will receive.

One possibility is just to return it to the shareholders in a dividend. But that’s kind of boring, so what I would do is to follow the Go big or go home strategy and ‘go big’ in the core markets of HSBC.

HSBC’s core markets are firstly in Asia, where it’s the biggest bank in Hong Kong and also has significant operations in China, India, in the Middle East, and in some other Asian countries.

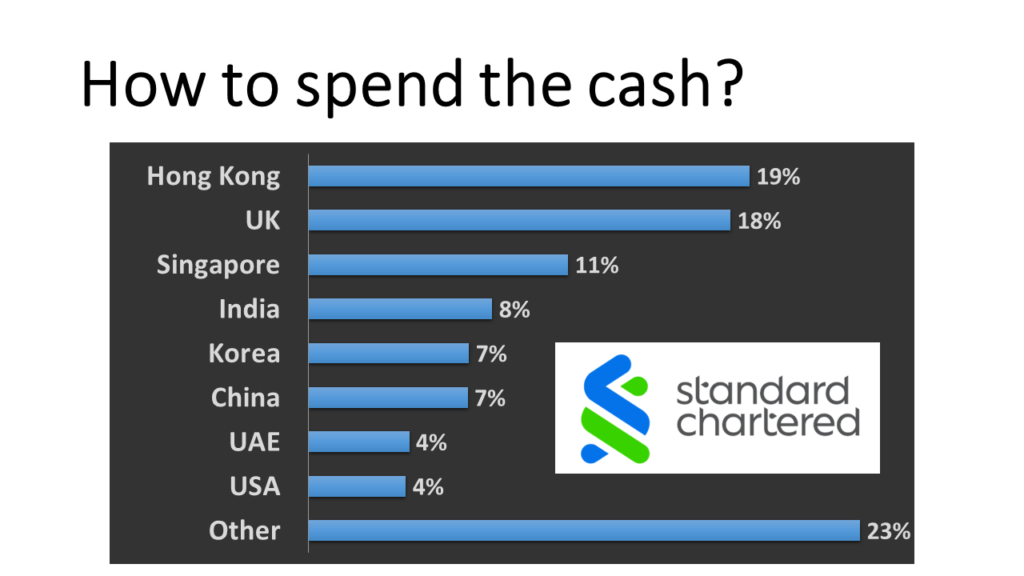

So what could we do with the cash (or the cash plus some extra borrowed money)?

The obvious takeover candidate would be Standard Chartered. Standard Chartered is another British bank that is based in London and is mostly operational in the Far East (and also partly in Africa and the Middle East). If HSBC were to buy Standard Chartered, there would be synergies of course in the London offices. I’m not sure if they would be allowed to take over the Hong Kong division of Standard Chartered because maybe HSBC would become too dominant in Hong Kong, but at least buying the Asian divisions would be a huge boost to HSBC in Singapore and it would also strengthen the bank in China,India and South Korea. Also in the United Arab Emirates and Asian economies like Malaysia, Indonesia, Vietnam. All those countries would contribute to a higher market share of HSBC and hopefully also to higher profitability and economies of scale.

I already mentioned that they should probably sell the Hong Kong division of Standard Chartered. And I guess they should also sell the African subsidiaries of Standard Chartered because I don’t see a lot of synergies there. And HSBC is mostly focused on Asia and not on Africa. So that would also bring in some extra cash because the 10 billion US dollars won’t be enough to buy standard Charters. But I think there’s a very clear business case to purchase Standard Chartered.

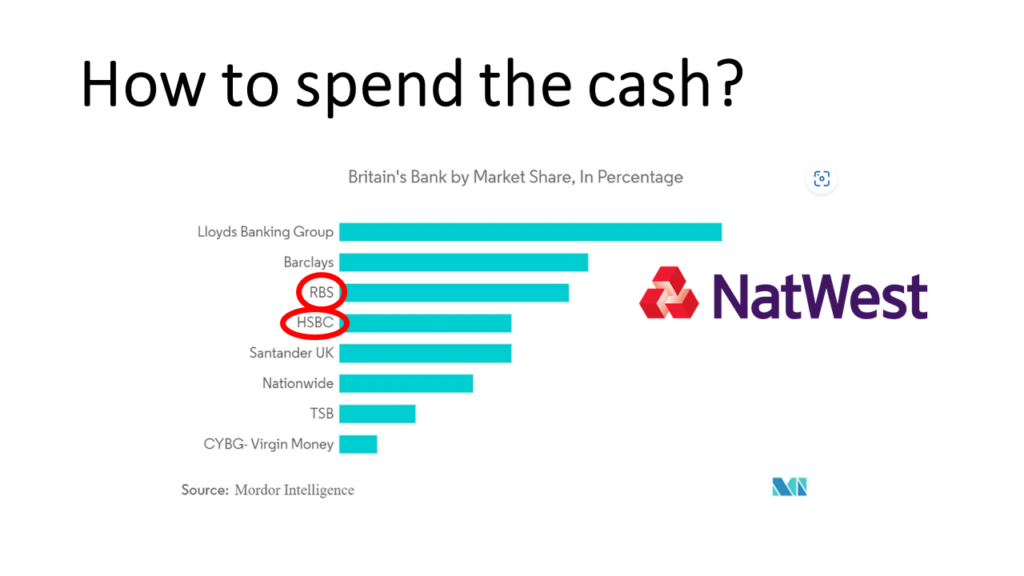

Another possibility would be to stay in the United Kingdom. So I found some research by Mordor Intelligence showing the market share of banks in the British market. You see that Lloyds is the clear market leader while HSBC is only the fourth largest retail bank in the UK (together with Santander UK). So a possible takeover target would be NatWest, which is the parent company above Royal Bank of Scotland – which is currently the third largest bank in Britain. Together with HSBC, they would be about as large as Lloyds Banking Group. So they would be the first or second largest bank in the United Kingdom. This [acquisition] would definitely provide some economies of scale on its British home market and would be quite easy to integrate. I think that deal makes a lot of sense also from a business perspective. Compared to Standard Chartered, where you would need to do a lot of divestments and integration in a lot of markets, the NatWest acquisition would be quite simple in terms of geography. You would also only need the approval of the British authorities. So I think that makes a lot of sense as well.

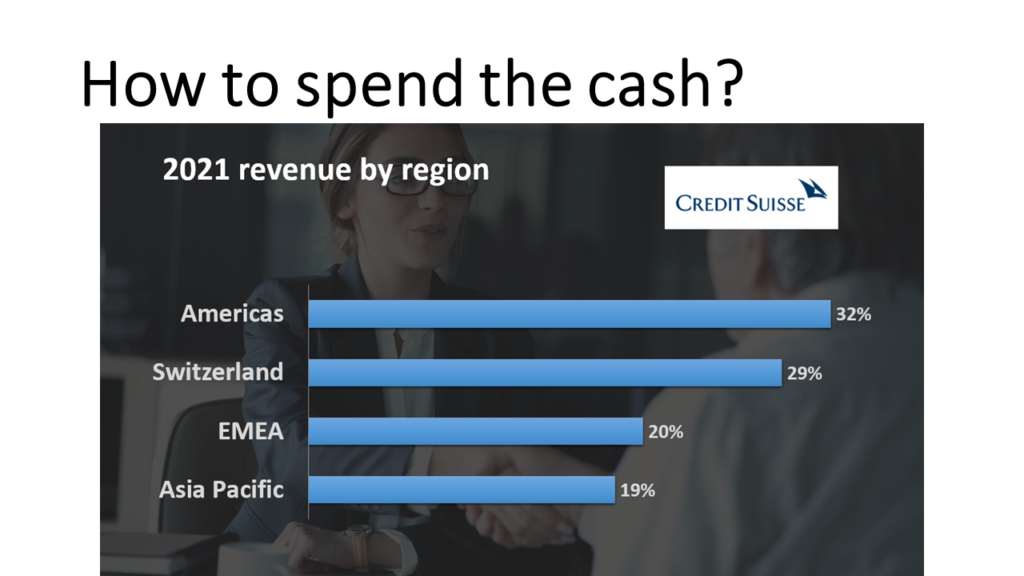

And then finally, thinking out of the box, we could also look at Credit Suisse. I wouldn’t suggest to buy the entirety of Credit Suisse, although its market cap is so low that with $10 billion you could almost buy the entire bank.

But what is probably a better idea is if HSBC would buy the Asia Pacific operations and maybe also the Middle Eastern operations of Credit Suisse. So I guess you don’t need the entire amount of 10 billion dollars. But by buying the Asia Pacific operations of Credit Suisse, HSBC could strengthen its wealth management in countries like China but also in Singapore and in other East Asian countries. And maybe also strengthen some of the investment banking operations in Asia. I think management of Credit Suisse would probably be happy to sell those divisions because then Credit Suisse can focus more on its core divisions in Switzerland and the Americas. While now CS are a global bank but they don’t have the size they need to be a real global bank.

So these have been three ideas. HSBC has sold its Canadian division for a lot of money. They could either buy Standard Chartered, or NatWest, or the Asian activities of Credit Suisse. I’m very curious of course what you think. Should they just return the money to their shareholders? Or should they buy other banks? Or do you have any other ideas? Maybe they should focus on share buybacks.

I hate to bring this up on the first (working) day of 2022, but the primary objective of the ECB is still price stability.

With inflation close to 5%, it seems that talking and tweeting about the ECB’s secondary objectives is more important than delivering stable prices.

Within a year’s time, your economists have doubled their projections for inflation in 2022.

🇪🇺 New @ecb staff projections. Key figures: 3.2% inflation in 2022 (!), but headline and core inflation at 1.8%, close to but *below* 2% target. pic.twitter.com/Y5On3eIPsv

So you’ll understand that people don’t believe you when you say that inflation will go down this year.

If you do choose to stay ECB President in 2022, I wish you a firm hand.

On New Year’s day, the 20th birthday of the euro, you called the euro a “beacon of stability and solidity around the world”.

To keep it that way, the ECB will need your strong leadership.

Happy birthday to the euro! 20 years since the launch of euro cash, our currency is a beacon of stability and solidity around the world – thanks to you, the hundreds of millions of Europeans who use it every day. https://t.co/BZBSZeRR9J

Hello and welcome to a special episode of the Finrestra podcast.

I wish you a happy new year! Stick around till the end, because I’m giving away 250 euros.

New year, new month, so here’s a quick recap of the European financial news of December.

Santander has to pay almost 68 million euros to Andrea Orcel. Santander had offered the former UBS banker the role of CEO, but withdrew its offer.

In other legal news, a French court has reduced a 4.5 billion euro fine for UBS to 1.8 billion euro. The Swiss bank was found guilty of money laundering.

Dutch green bank Triodos will set up a multilateral trading facility for its shareholders (technically certificate holders). Since the beginning of 2020, shareholders cannot sell their certificates. It is expected that trading will resume at a price that is 30 or 40 percent lower than before the pandemic.

There was also consolidation and divestment news.

BNP Paribas has agreed to sell its American subsidiary Bank of the West for 16.3 billion dollars. Listen to episode 9 of the Finrestra podcast for our take on this transaction.

Cooperative bank Crelan acquires AXA Bank Belgium. The deal had already been announced in 2019, but was waiting for approval by the ECB. The new bank will be the fifth largest in Belgium.

Regular listeners know that I usually do an in-depth analysis of one topic after the news. However, today I want to tell you a bit about Finrestra and my plans for 2022.

I started this podcast because there are not many podcasts focused on European finance. My original goal was to do a weekly interview. But I quickly found out that this is easier said than done. Weekly episodes require more time than I have. And it hasn’t been easy to find people who want to come on the show. So I want to thank my first guests Uuree Batsaikhan, Koen Vingerhoets and Rik Coeckelbergs again!

For 2022, there will be two episodes per months. I hope that from February onwards, I will be able to interview a number of very interesting guests. Stay tuned!

If you’re listening to this podcast on Apple or Spotify, you may not know that there is also a Finrestra YouTube channel, where I post short videos about financial topics. For example, I have a series of bank profiles, including of Santander, Triodos, BNP Paribas and ING, which were all mentioned in the news recap. I also want to create more videos with short stories about European finance.

But neither the podcast nor YouTube pays my bills, and this is where you can help me. Don’t worry, I’m not asking for money, I’m giving you a chance to win money!

Finrestra stands for Financial Research and Training. So far, we have mainly worked for Belgian based clients. But I want to expand my activities to the rest of Europe. If you share my YouTube video with my two courses for 2022 on LinkedIn and tag a friend before 25 January, you can win 250 euro. I’ll put the link in the description.

This has been another episode of the Finrestra podcast. You can find my on twitter @janmusschoot. You can mail me at jan dot musschoot at finrestra dot com.

Thanks for listening and I hope you have a great 2022!”

Euro area inflation remains far above the ECB’s 2 percent target. Dutch inflation was 5.2 percent, a figure not observed since 1982. The German inflation rate was the highest since 19 ninety 2. Ironically, the union of the ECB’s own employees wants higher wages due to inflation.

In other record news, the French stock market index CAC 40 reached a new all-time high. It finally surpassed its peak from the year 2000.

There was also consolidation news:

BBVA wants to buy the stake of Turkish Garanti BBVA bank it doesn’t own yet

KBC buys the Bulgarian banking activities of Raiffeisen Bank International

The news of record high stock prices brings us to the topic of this episode: European bank CEOs should be ashamed.

Why?

Because their stocks have been horrible investments. Despite a nice rally in 2021, most large European banks still trade 70, 80 or 90 percent below their 2007 highs.

Or look at banks by market capitalization. The biggest European bank, HSBC, is only worth a quarter of American JP Morgan. And you could argue that HSBC isn’t even really a European bank, as most of its profit is generated in Hong Kong.

What’s the second largest European bank by market cap? Surely it must be a German, British or French one? Nope. It’s actually Sberbank of Russia. Russia, a country with a GDP smaller than Italy’s.

I can hear some CEOs already. How they are victims of low interest rates, low growth, overcapacity. Blah blah blah.

Instead of making excuses, take a hard look at banks like DNB, KBC, Nordea and SEB. Why are these relatively small banks worth more than giants like Deutsche Bank, Société Générale and UniCredit?

I know the answer. But do bank CEOs?

Here’s some free advice. Listen to episode 3 of the Finrestra podcast. And watch the “Bank in two minutes” series on our YouTube channel.

What will you learn? That successful banks focus. Focus on a few countries. Focus on one client segment, or at least on very complementary segments.

In contrast, banks with low profitability are often monsters of Frankenstein. They are part retail bank, part investment bank. They are active in dozens of countries.

They are big, but do they deliver what clients and investors want? The market doesn’t think so.

Now dear listener, before I go, I want to ask you a favor. For an upcoming episode, I would like to talk about Industry, the series about junior investment bankers. I recognized a lot of situations in the series. So if you work in a bank, watched Industry and would like to talk about it, please contact me! This has been another episode of The Finrestra Podcast. If you have suggestions for topics or guests, you can mail me at jan.musschoot@finrestra.com. You can find me on twitter @janmusschoot. Thanks for listening!”

“Hello and welcome to another episode of The Finrestra Podcast. My name is Jan Musschoot. We were off last week due to the banking holiday on November 1st. So here is a recap of the European financial news of October.

The governing council of the ECB discussed inflation, but central bankers expect no rate hikes in 2022.

Italy and UniCredit ended negotiations over the sale of Monte Paschi di Siena.

Swedish Handelsbanken will leave Denmark and Finland. This fits into a trend that I discussed in episode 3 of the Finrestra podcast.

Volvo Cars had its IPO in Stockholm, one of the largest European IPOs this year

French government bonds were traded on a blockchain with central bank digital currency

ING phases out its payment subsidiary Payvision

ABN AMRO passes on anti money laundering costs to coffeeshops, which can increase fees up to 1000%

French bank La Banque Postale will exit oil and gas by 2030

Dutch pension fund ABP stops investing in fossil fuel producers by 2023

Finally, COP26 started. COP26 is the climate summit in Glasgow.

And that brings us to the deep dive of this episode.

What do banks do against climate change?

The website Our world in data has a nice overview of the greenhouse gas emissions by sector. The majority of global emissions come from energy use in industry, transport and buildings. Other activities that emit a lot of greenhouse gases include agriculture and the production of cement.

Banking or finance aren’t explicitly mentioned. Not surprising, because you only need an office and a computer to generate financial services. So the direct CO2 emissions of banks are negligible.

On the other hand, banks provide funding to coal miners, oil and gas companies, and other carbon intensive industries. Asset managers and pension funds invest in the stocks and bonds of fossil fuel producers. These assets contribute to the so-called ‘Scope 3 emissions’ of the financial industry. According to Greenpeace and the WWF, UK financial institutions are responsible for nearly double the UK’s annual carbon emissions.

But banks can also steer their clients towards lower emissions. They can refuse credit for power plants that burn coal, and divert the money to wind farms. Loans for real estate, both residential and commercial, are a big chunk of banks’ assets. Banks can stimulate borrowers to make buildings energy-efficient.

To formalize their climate commitments, 50 European banks have joined the Net-Zero Banking Alliance. This alliance is convened by the United Nations and led by the banking industry. The members of the Net-Zero Banking Alliance commit to transition their lending and investment portfolios to align with net-zero by 2050. The signatories include sustainable banks like Triodos and GLS Bank. But without the big banks, this initiative wouldn’t have much effect. However, the CEOs of most large European banks have also signed the Commitment Statement of the Net-Zero Banking Alliance. Members currently include global systemically important banks such as HSBC, BNP Paribas, Santander, Deutsche Bank and UniCredit. So far, no Belgian banks have joined.

Is the Net-Zero Banking Alliance yet another case of greenwashing? Is it all blah blah blah, as Greta Thunberg would say? It shouldn’t be.

Banks that join the Alliance have to disclose targets on how they will support the temperature goals of the Paris Agreement. These targets will be reviewed to ensure consistency with climate science. Everybody will be able to check whether banks keep their promises, because they have to report the emissions of their lending and investment portfolios annually.

This has been another episode of The Finrestra Podcast. If you have suggestions for topics or guests, you can mail me at jan.musschoot@finrestra.com. You can find me on twitter @janmusschoot. Thanks for listening!”

“Hello and welcome to another episode of The Finrestra Podcast.

My name is Jan Musschoot.

The topic of today’s episode: Go big or go home!

According to economic theory, banks have good reasons to expand abroad. Bigger banks should benefit from economies of scale. A broader geographic footprint results in a more diversified loan portfolio. So multinational groups should be more resilient against economic downturns.

However, cross-border expansion is not what we observe in the real world. In fact, multinational banks have been selling their foreign subsidiaries for years. Earlier this year, American Citibank announced that it would exit retail banking in 13 countries, most of them in Asia. Last year, Spanish bank BBVA sold its unit in the United States.

Banks are also selling their foreign activities in Europe. Here are some examples, all from 2021.

British HSBC was so desperate to get rid of its French retail bank, that it sold the unit for one symbolic euro. Dutch ING also plans to leave the French retail market. That same ING has sold its retail bank in Austria. Dutch Rabobank decided to wind down its Belgian retail activities, as it couldn’t find a buyer. British NatWest and Belgian KBC have announced they would exit the Republic of Ireland.

Bankers have good reasons to leave foreign markets. Because policymakers are scared of “too big to fail” banks, so-called systemically important banks need larger capital buffers. More countries also means higher costs for reporting and compliance. Banks have learned that there are few synergies between countries, even for branchless banks that only offer online services, like ING and Rabobank.

That’s why there is a clear trend towards deglobalization.

But that’s not the end of the story. Not all banks are returning to their domestic past.

Economies of scale are a thing, but not in the sense that bigger is always better.

What you want is to have scale within a market.

A good example is Societe Generale. The French financial services group sold most of its Central and Eastern European units. But SocGen kept its subsidiaries in the Czech Republic and in Romania. In both countries, these banks are the third largest in the market. Hungarian OTP sold its small subsidiary in neighboring Slovakia to KBC-owned CSOB. But OTP has also recently signed a deal to buy the second largest bank of Slovenia. Merged with its existing Slovenian subsidiary, it will become the market leader. And this silent consolidation isn’t limited to the East. French Credit Agricole has been gradually increasing its market share in Italy, for example.

So while European policymakers despair at the lack of cross-border mergers and acquisitions, the much needed consolidation is happening. Banks are reducing their geographic complexity.

And some groups have become robust multinational banks that have a significant market share in multiple countries.

If you want to discuss banks’ strategy, you can find me on Twitter @janmusschoot.

To learn more about our research and courses, check out our website, finrestra.com.

“Here’s what you need to know about the debt ceiling.

The main player in this drama is the US congress. Congress is the legislative body of the federal government, similar to parliaments in Europe. Congress makes the laws.

In particular, Congress specified how much the US should spend on things like social security and the military. Congress also passed laws on taxation.

These laws are executed by the Treasury, what we call the Ministry of Finance in Europe.

Because expenditures exceed the tax revenue approved by Congress, the Treasury needs to borrow the difference. So US government debt goes up.

And that’s where the debt ceiling comes in.

In addition to laws on spending and taxation, Congress also passed a law on the maximum level of government debt. This so-called “debt ceiling” is currently somewhat above 28 trillion dollars.

If Congress doesn’t raise the debt ceiling, the Treasury has a huge problem.

To comply with the law, Treasury has to spend money on existing programs. But according to the debt ceiling, it cannot borrow any more money. And Treasury cannot create new taxes, that’s the responsibility of Congress.

So it seems that the Treasury is trapped in an impossible trinity, where it cannot satisfy the three demands of Congress (spend, tax, debt ceiling) at the same time.

But some smart lawyers have discovered a loophole.

Treasury has the right to make money. Specifically, the Treasury can mint coins from platinum, a precious metal. But the value of the coins isn’t in the metal. The coin can be whatever value the Treasury says it is. Just like a 100 dollar bill is worth a hundred dollars because it is issued by the Federal Reserve, not because the material is worth a hundred dollars.

So when Congress doesn’t raise the debt ceiling, Treasury can make a trillion dollar platinum coin. That way, it has extra money to keep paying the existing spending programs approved by Congress, without increasing the debt.

There’s a website, mintthecoin.org, which has answers to a lot of questions on the proposal to mint a trillion dollar coin. For example, whether it’s legal (yes, it is) and whether it would lead to hyperinflation (no, it won’t).

I hope you enjoyed this episode of the Finrestra Podcast. Don’t forget to listen to ourfirstepisode with Uuree Batsaikhan of Positive Money Europe. You can follow me on Twitter @janmusschoot, that’s @ j a n m u s s c h o o t. Our website is finrestra.com. Thanks for listening!”