I especially liked his discussion of “front book, back book“. Banks and insurers accumulate a long-term book of assets. These generate a predictable stream of income (interest and premiums). Unfortunately, this “back book” exposes them to unexpected losses. As a result, financial firms need a lot of capital.

The business model of Software-as-a-Service (SaaS) companies is also based on a back book. However, unlike banks, their portfolio of subscribers does not require a lot of capital.

In the same newletter, Rubinstein discusses the possibility of bank M&A funded by badwill, as I suggested earlier.

Sean Pawley talks about banking in East Africa on the Palladium Podcast (discussion about banks between 6:50 and 22:15). Multiple issues with banking in Rwanda and other countries in the region: economy runs on cash payments -> banks lack reliable data on borrowers -> high default rates -> unstable banks, high interest rates and fees, preference of cash over bank deposits. His solution: a narrow bank that eliminates credit risk. Provide a cellphone-based payment solution. Collect payment data. Based on the data, start making loans.

As always, Santander does the smart fin thing: they just booked 12.6bn of goodwill and DTA impairments! That is massive ! Why ? Because it doesn't affect CET1. And if you're going to do it, do it when you can't pay dividend anyway ? More seriously, this is going to be a pattern!

The founders of the European Payments Initiative (EPI) include all major French, German and Spanish banks.

I’m curious why Intesa Sanpaolo1 and the Austrian and Nordic banks haven’t joined.

A pan-European payment solution is long overdue. Payment providers like Visa, Mastercard and PayPal have profit margins that European banks can only dream of. Increased competition and lower prices would be great for sellers and consumers.

Ancient history: “In 2003, refinancing via LTROs amounts to 45 bln Euro which is about 20% of overall liquidity provided by the ECB.” (On June 18, 2020, banks borrowed 1.31 trillion euro from the ECB via TLTRO!)

Many European banks and insurance companies are trading well below their book value.

Large firms can unlock a lot of value by taking over smaller competitors, thanks to the negative goodwill. Consolidation would support the profitability of the financial industry.

Also first serious hostile takeover in the world of banking since ages. The buyers are looking to split UBI into pieces (and to finance this with badwill ?) https://t.co/GzYHANZmf4

Italian banks in particular would benefit from a consolidation of their fragmented domestic market2. In February, Intesa Sanpaololaunched a bid for UBI Banca. UniCredit should consider a similar deal with Banco BPM, Banca Monte dei Paschi di Siena or BPER Banca. Also, French BNP Paribas could merge its subsidiary BNL with one of those banks.

Spain

Spanish banking is already quite concentrated. Santander took overBanco Popular in 2017. The integration was completed in 2019. Santander and BBVA could acquire Bankinter, Bankia, or Banco de Sabadell. Of course, further domestic growth of the majors depends on regulatory approval. The two global Spanish banks definitely have the expertise to execute such an operation.

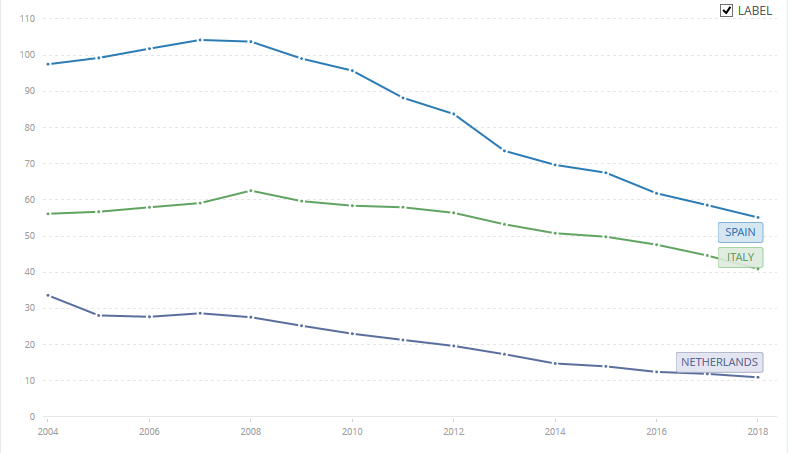

Figure 1 shows the number of bank branches relative to population for Spain, Italy and the Netherlands. It’s clear that Italy and Spain have a lot of potential for cost cutting.

Figure 1: Commercial bank branches per 100,000 adults in Spain, Italy and the Netherlands. Source: World Bank.

Portugal, Poland and the Netherlands

In neighbouring Portugal, Banco Comercial Português seems a good match for Santander. Especially since both Iberian banks are active in Poland. Speaking of Poland, Santander and ING might be interested in mBank. mBank is owned by Commerzbank, a bank that desperately needs to focus its strategy.

A foreign group could shake up the uncompetitive Dutch market by buying ABN AMRO. However, as most of ABN AMRO is still state owned, this will be complicated.

Insurance

Many listed insurers like Aegon, NN Group (NL), Ageas (BE), Baloise, Swiss Life (CH) or UnipolSai (IT) trade at a significant discount to their book value. This could be an opportunity for big insurance companies AXA, Allianz and Zurich Insurance Group.

Consortiums of buyers could also divide the operations of their targets (although there is a bad precedent for this scenario).

Update 23 July 2020: Marc Rubinstein at Net Interest came to the same conclusion: “Coming out of Covid, when banks realise they don’t need such a large physical presence, further consolidation is likely. What’s more, if equity valuations don’t recover, banks may be able to use negative goodwill to cover restructuring charges.”

How do you move millions of dollars from one place to another?

Obviously, you use a bank.

But what if the money is dirty?

The Organized Crime and Corruption Reporting Project (OCCRP) has documented several laundromats, e.g. the Troika Laundromat.

A laundromat is a scheme of shell companies and bank accounts to move money – often Russian money – offshore. The investigations read like a spy novel, full of criminals, politicians, lawyers and bankers.

For example, this article explains how Moldovan judges enabled flows out of Russia by authenticating guarantees on “defaulted loans” between shell companies.

Sometimes, bankers looted their own institutions, see The Vienna Bank Job for details.

Fascinating stuff, involving major Western banks as well.

How should authorities respond to these illicit activities?

In the thread below, Benjamin Braun explains Germany’s political economy. More specifically, he and Richard Deeg studied the interaction between the financial and non financial corporate (NFC) sectors.

‘German banks' supply of patient capital is the lifeblood of the German growth model’

The German NFC sector has high profits (1) and runs a trade surplus (2).

(1) enables companies to finance their own investments. They don’t need to borrow money from banks.

(2) leads to an inflow of reserves and deposits at banks. As a result, German banks lend to foreign entities.

This seems a sensible story.

However, I don’t agree with the conclusion:

The conventional policy wisdom is that Germany is overbanked. That may be true, but also German workers are underpaid. Policymakers who want to help German banks should focus on strengthening unions, raising wages, and on moving away from export-led growth. /END

First of all, I highly doubt any policymakers really want to help German banks. If that were the case, the monstrosity of publicly owned, unprofitable banks would have been cleaned up by now.

But even if German politicians cared, it’s not clear that stronger unions or higher wages would be more than a drop in a bucket.

A higher demand for credit would have an immediate positive impact on German banks. And there is a lot of room for growth.

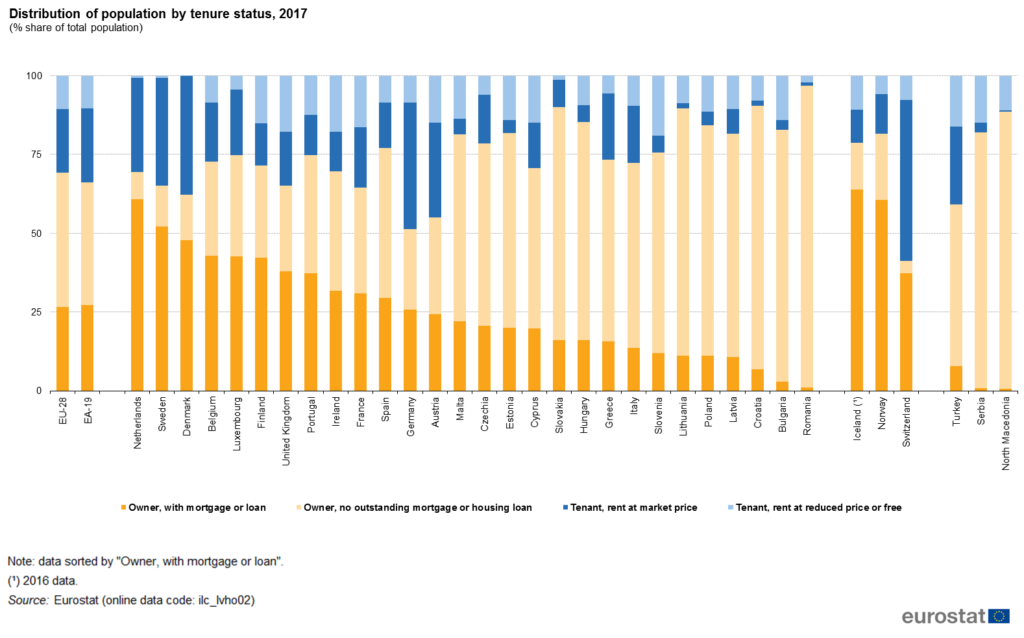

Home ownership in Germany is low compared to non-German speaking countries, as you can see in this picture from Eurostat.

Stimulating home ownership would boost the demand for mortgages.

More investment by the government, as called for by industry and labor unions, would also increase the domestic supply of assets for banks if it’s funded by bonds instead of taxes.

If Angela Merkel wants some more advice, she can leave a comment 🙂

The interest rate on its savings account will be zero percent, which is less than the minimum of 0.11% at other banks.

Finally, there’s no indication that it will delight customers with superior services.

So NewB scores zero out of three.

Yet NewB’s business plan expects the bank to have 277 million euro in deposits by the end of 2024.

Some Chinese banks offer pork meat as a reward for opening an account. Maybe NewB should give an Impossible Burger to new customers? Otherwise, this is gonna turn into Mission: Impossible.

{kind=link}