In their paper Against amnesia: re-imagining central banking, Benjamin Braun and Leah Downey describe the elite consensus on central banking as a ‘holy trinity’. This holy trinity consists of (1) an independent central bank that (2) sets the short term interest rate to (3) achieve stable prices1.

The fact that quantitative easing (QE) is still often called unconventional monetary policy speaks volumes for how deeply the holy trinity is ingrained in the minds of the community. However, more and more people are questioning this model of central banking2.

Central bankers are almost begging politicians to spend more. A formal framework for fiscal and monetary coordination would do away with the fiction3 of central bank independence.

There’s an explosion of ideas for new instruments, from yield curve control to canceling debt to green TLTROs.

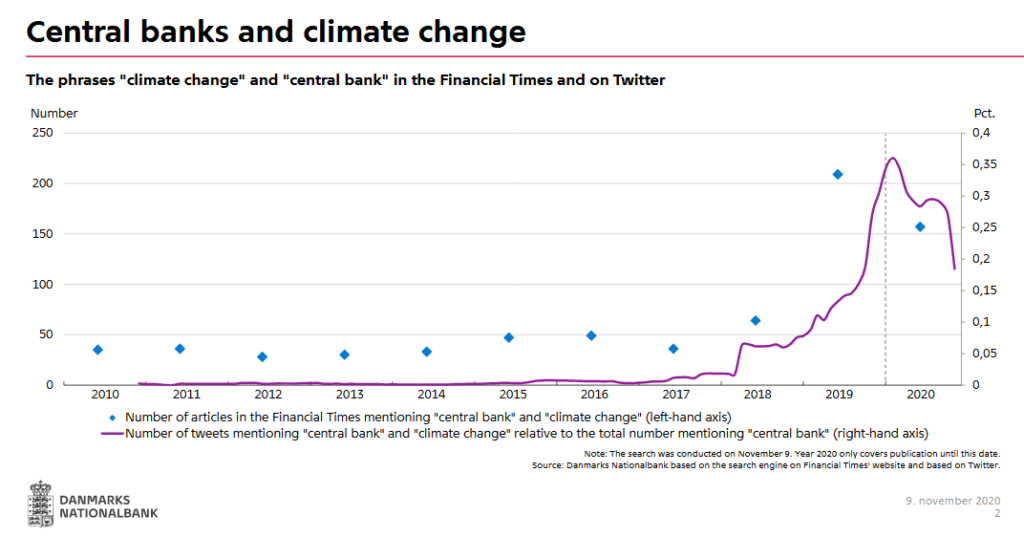

While almost nobody wants to ditch price stability, central bankers are taking on extra responsabilities based on local sensitivities. European central bankers (both at the ECB and the Bank of England) are making their institutions climate friendly. The Federal Reserve has had a dual mandate of price stability and full employment for a long time. The Reserve Bank of New Zealand will take house prices into account.

Although central banking post-holy trinity will have its own challenges, I, for one, welcome our central bank overlords.