Peter Thiel explains why competition is for losers and why you should start with small markets. He also answers the question “if you’re so smart, why aren’t you rich?”

Kevin Hale on how to evaluate startup ideas:

Peter Thiel explains why competition is for losers and why you should start with small markets. He also answers the question “if you’re so smart, why aren’t you rich?”

Kevin Hale on how to evaluate startup ideas:

The Asian Banker has an overview of the largest banks in Africa and the Middle East.

Some things that could happen1:

Cliché ideas of how the international economy works (see the work of Brad Setser and many others):

Let’s have a look at how the aircraft leasing business works in reality.

Financial center? Check:

“Ireland is one of the biggest centres for airline leasing in the world. Many of the world’s biggest and best airline leasing companies are based in the Republic”, which explains why Ireland has 17,000 aircraft orders. [To be fair, financial centers also benefit from the concentration of specialized workers and firms.]

Financiers from Germany, Japan and China investing in low-margin, high risk businesses? Check:

Between 2010 and 2014, [Dublin-based aircraft leasing company] Avolon also raised US$6.1 billion in debt from the capital markets and a range of commercial and specialist aviation banks including Wells Fargo Securities, Citi, Deutsche Bank, BNP Paribas, Credit Agricole, UBS, DVB, Nord LB and KfW IPEX-Bank. In 2017, Avolon entered the public debt markets and raised a total over US$9 billion in debt finance. In November 2018, Avolon announced that Japanese financial institution, ORIX Corporation had acquired a 30% stake in the business from its shareholder Bohai Capital, part of China’s HNA Group. (source: Wikipedia)

A group of 16 European banks are working on a unified card and digital wallet that can be used across Europe.

The founders of the European Payments Initiative (EPI) include all major French, German and Spanish banks.

I’m curious why Intesa Sanpaolo2 and the Austrian and Nordic banks haven’t joined.

A pan-European payment solution is long overdue. Payment providers like Visa, Mastercard and PayPal have profit margins that European banks can only dream of. Increased competition and lower prices would be great for sellers and consumers.

Stroomt het geld van de Nederlandse en Duitse belastingbetalers naar de luie Italianen? Philipp Heimberger en Nikolaus Krowall zetten enkele feiten over de Italiaanse economie op een rijtje in dit artikel.

Korte versie op Twitter:

Some interesting articles I came across recently:

Yemen has two governments (civil war), one currency, and two monetary systems.

IT project management horror story at German Apobank (in German).

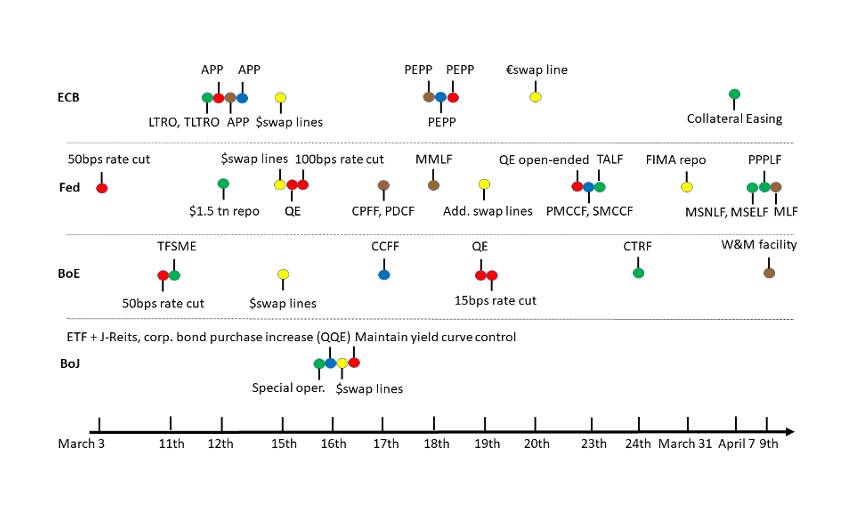

Overview of the Eurosystem response to the pandemic.

What central banks have done to help the economy survive Covid-19

Historical lessons from large increases in government debt

Euro area economic expansions are like Tolkien’s Elves: they don’t die of old age. The most recent one was murdered by corona.

(On a sidenote: I’ve been critical about the lack of blogging at the ECB. But it turns out that the Banque de France’s Eco Notepad is an excellent blog, as the four articles above show!)

All of the World’s Money and Markets in One Visualization

How may clicks to open a bank account? (Built for Mars on the user experience of retail banking)

The Economic Foundations of Industrial Policy: an amazing longread (very long!) on productivity, explaining why rich nations are rich

Ancient history: “In 2003, refinancing via LTROs amounts to 45 bln Euro which is about 20% of overall liquidity provided by the ECB.” (On June 18, 2020, banks borrowed 1.31 trillion euro from the ECB via TLTRO!)

Opiniestuk met Hans Bevers in De Tijd (11/06/2020):

Mik met een relanceplan op vaste kosten en investeringen

Enkele citaten in artikel Trends (26/03/2020):

Many European banks and insurance companies are trading well below their book value.

Large firms can unlock a lot of value by taking over smaller competitors, thanks to the negative goodwill. Consolidation would support the profitability of the financial industry.

Italian banks in particular would benefit from a consolidation of their fragmented domestic market3. In February, Intesa Sanpaolo launched a bid for UBI Banca. UniCredit should consider a similar deal with Banco BPM, Banca Monte dei Paschi di Siena or BPER Banca. Also, French BNP Paribas could merge its subsidiary BNL with one of those banks.

Spanish banking is already quite concentrated. Santander took over Banco Popular in 2017. The integration was completed in 2019. Santander and BBVA could acquire Bankinter, Bankia, or Banco de Sabadell. Of course, further domestic growth of the majors depends on regulatory approval. The two global Spanish banks definitely have the expertise to execute such an operation.

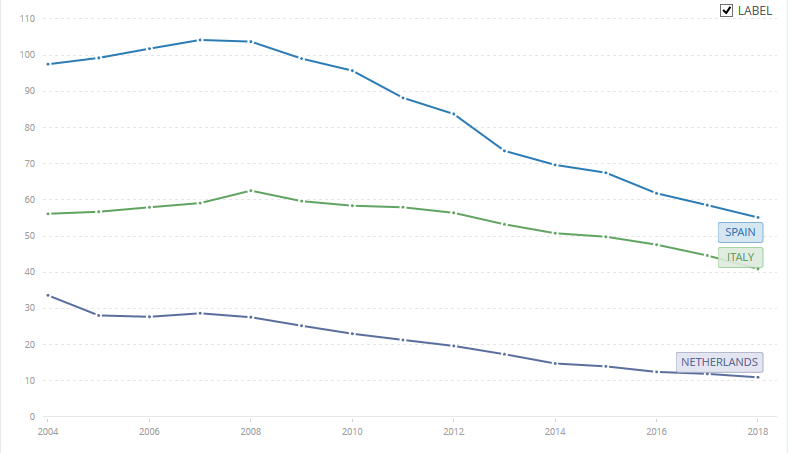

Figure 1 shows the number of bank branches relative to population for Spain, Italy and the Netherlands. It’s clear that Italy and Spain have a lot of potential for cost cutting.

In neighbouring Portugal, Banco Comercial Português seems a good match for Santander. Especially since both Iberian banks are active in Poland. Speaking of Poland, Santander and ING might be interested in mBank. mBank is owned by Commerzbank, a bank that desperately needs to focus its strategy.

A foreign group could shake up the uncompetitive Dutch market by buying ABN AMRO. However, as most of ABN AMRO is still state owned, this will be complicated.

Many listed insurers like Aegon, NN Group (NL), Ageas (BE), Baloise, Swiss Life (CH) or UnipolSai (IT) trade at a significant discount to their book value. This could be an opportunity for big insurance companies AXA, Allianz and Zurich Insurance Group.

Consortiums of buyers could also divide the operations of their targets (although there is a bad precedent for this scenario).

Exciting times!

Update 9 June 2020: Banco Sabadell plans to close 235 branches

Update 23 July 2020: Marc Rubinstein at Net Interest came to the same conclusion: “Coming out of Covid, when banks realise they don’t need such a large physical presence, further consolidation is likely. What’s more, if equity valuations don’t recover, banks may be able to use negative goodwill to cover restructuring charges.”

Door de lockdown hebben veel bedrijven verlies geleden. Het ligt voor de hand dat de overheid de schade moet vergoeden.

Maar in plaats van dat rechtstreeks te doen, met eenduidige voorwaarden, bouwt de politiek weer een reeks koterijen bij.

Politici hebben de mond vol van gerichte maatregelen en vereenvoudiging.

In realiteit krijgen we hinder- en sluitingspremies (een druppel op een hete plaat voor grotere bedrijven), lagere btw voor de horeca (hulp aan één sector), cadeaus voor kapitaalverstrekkers (investeren is risico’s nemen, waarom moet dit een fiscaal voordeel krijgen?)…

Ik hoop dat politici die voor deze maatregelen stemmen niet gaan zagen over de ingewikkelde belastingaangifte of over toekomstige begrotingstekorten4.

De gegoede klasse zoals politici, professoren en vermogensbeheerders (tiens, wie zat ook al weer in het economisch relancecomité?) wordt in de watten gelegd. Zo wordt de btw op restaurant verlaagd naar 6%5. En wie tot 75.000 euro belegt in “vriendenaandelen” krijgt als beloning een jaarlijkse belastingkorting.