The EU missed an opportunity to provide macroeconomic support that matches the size of the corona shock, to increase safe assets and to avoid transfers between member states.

Peter Thiel explains why competition is for losers and why you should start with small markets. He also answers the question “if you’re so smart, why aren’t you rich?”

Cliché ideas of how the international economy works (see the work of Brad Setser and many others):

Companies use “financial centers” aka tax havens to minimize their tax bills.

Financial institutions in surplus countries invest the money abroad, but are not good at it.

Let’s have a look at how the aircraft leasing business works in reality.

Financial center? Check: “Ireland is one of the biggest centres for airline leasing in the world. Many of the world’s biggest and best airline leasing companies are based in the Republic”, which explains why Ireland has 17,000 aircraft orders. [To be fair, financial centers also benefit from the concentration of specialized workers and firms.]

Financiers from Germany, Japan and China investing in low-margin, high risk businesses? Check: Between 2010 and 2014, [Dublin-based aircraft leasing company] Avolon also raised US$6.1 billion in debt from the capital markets and a range of commercial and specialist aviation banks including Wells Fargo Securities, Citi, Deutsche Bank, BNP Paribas, Credit Agricole, UBS, DVB, Nord LB and KfW IPEX-Bank. In 2017, Avolon entered the public debt markets and raised a total over US$9 billion in debt finance. In November 2018, Avolon announced that Japanese financial institution, ORIX Corporation had acquired a 30% stake in the business from its shareholder Bohai Capital, part of China’s HNA Group. (source: Wikipedia)

The founders of the European Payments Initiative (EPI) include all major French, German and Spanish banks.

I’m curious why Intesa Sanpaolo2 and the Austrian and Nordic banks haven’t joined.

A pan-European payment solution is long overdue. Payment providers like Visa, Mastercard and PayPal have profit margins that European banks can only dream of. Increased competition and lower prices would be great for sellers and consumers.

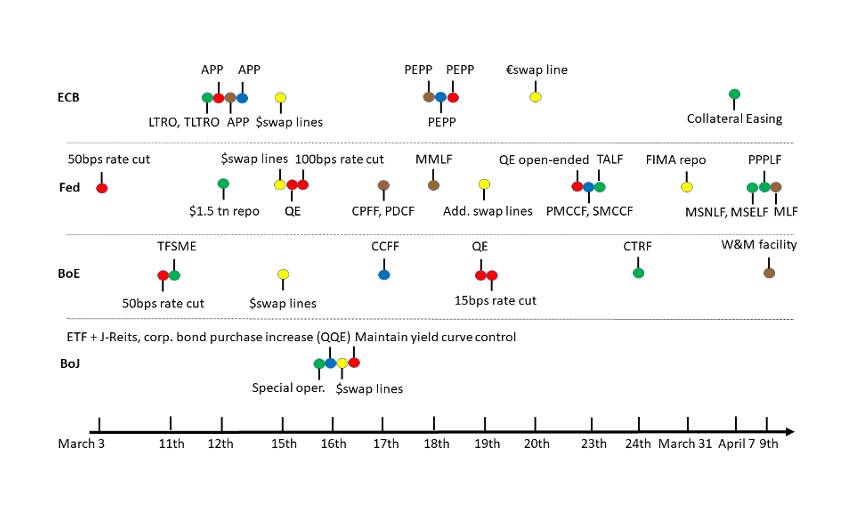

Ancient history: “In 2003, refinancing via LTROs amounts to 45 bln Euro which is about 20% of overall liquidity provided by the ECB.” (On June 18, 2020, banks borrowed 1.31 trillion euro from the ECB via TLTRO!)

Many European banks and insurance companies are trading well below their book value.

Large firms can unlock a lot of value by taking over smaller competitors, thanks to the negative goodwill. Consolidation would support the profitability of the financial industry.

Also first serious hostile takeover in the world of banking since ages. The buyers are looking to split UBI into pieces (and to finance this with badwill ?) https://t.co/GzYHANZmf4

Italian banks in particular would benefit from a consolidation of their fragmented domestic market3. In February, Intesa Sanpaololaunched a bid for UBI Banca. UniCredit should consider a similar deal with Banco BPM, Banca Monte dei Paschi di Siena or BPER Banca. Also, French BNP Paribas could merge its subsidiary BNL with one of those banks.

Spain

Spanish banking is already quite concentrated. Santander took overBanco Popular in 2017. The integration was completed in 2019. Santander and BBVA could acquire Bankinter, Bankia, or Banco de Sabadell. Of course, further domestic growth of the majors depends on regulatory approval. The two global Spanish banks definitely have the expertise to execute such an operation.

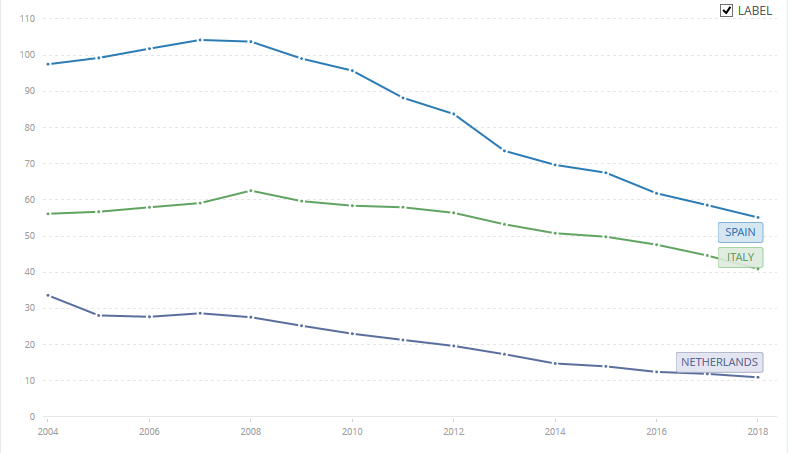

Figure 1 shows the number of bank branches relative to population for Spain, Italy and the Netherlands. It’s clear that Italy and Spain have a lot of potential for cost cutting.

Figure 1: Commercial bank branches per 100,000 adults in Spain, Italy and the Netherlands. Source: World Bank.

Portugal, Poland and the Netherlands

In neighbouring Portugal, Banco Comercial Português seems a good match for Santander. Especially since both Iberian banks are active in Poland. Speaking of Poland, Santander and ING might be interested in mBank. mBank is owned by Commerzbank, a bank that desperately needs to focus its strategy.

A foreign group could shake up the uncompetitive Dutch market by buying ABN AMRO. However, as most of ABN AMRO is still state owned, this will be complicated.

Insurance

Many listed insurers like Aegon, NN Group (NL), Ageas (BE), Baloise, Swiss Life (CH) or UnipolSai (IT) trade at a significant discount to their book value. This could be an opportunity for big insurance companies AXA, Allianz and Zurich Insurance Group.

Consortiums of buyers could also divide the operations of their targets (although there is a bad precedent for this scenario).

Update 23 July 2020: Marc Rubinstein at Net Interest came to the same conclusion: “Coming out of Covid, when banks realise they don’t need such a large physical presence, further consolidation is likely. What’s more, if equity valuations don’t recover, banks may be able to use negative goodwill to cover restructuring charges.”

The number of corona infections can roughly be modeled as N ~ R^t, where t is time4 and R is the reproduction number. The reproduction number R is the average number of new infections caused by one person infected with Covid-19.

If R > 1, the number of patients grows exponentially. If R < 1, the epidemic fizzles out.

How do people get infected? Obviously, they have to come into contact with the virus.