I got the GDP/person data for all the OECD cities in The EU and the UK with more than a million residents. And then I removed Dublin (because the data's daft) and then I made this graph. And now I'll get back to reading British writing/opinions about our cities "pulling ahead". pic.twitter.com/KMDIMjNzdY

Here top 10 by solar output, rather than capacity of which only a fraction is only ever used, based on IEA data (which doesn't have Vietnam in its database). https://t.co/X3XnH7bFqipic.twitter.com/cPCk1qkXjQ

Depressing story from @HirokoTabuchi about how oil giants sell off their unwanted polluting assets to companies with even looser environmental goals. The figure of flaring before and after sale is jaw dropping.

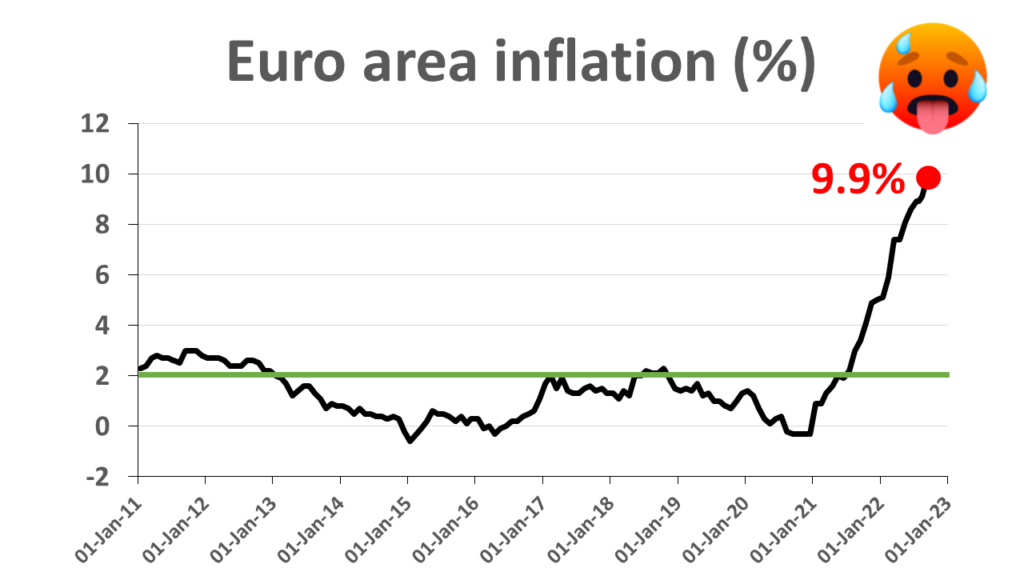

The European Central Bank is raising interest rates.

Here is ECB President Lagarde: “The Governing Council decided today to raise the three key ECB interest rates by 75 basis points. […] The Governing Council also decided to change the terms and conditions of the third series of targeted long-term refinancing operations, known as TLTRO III.” (press release, video)

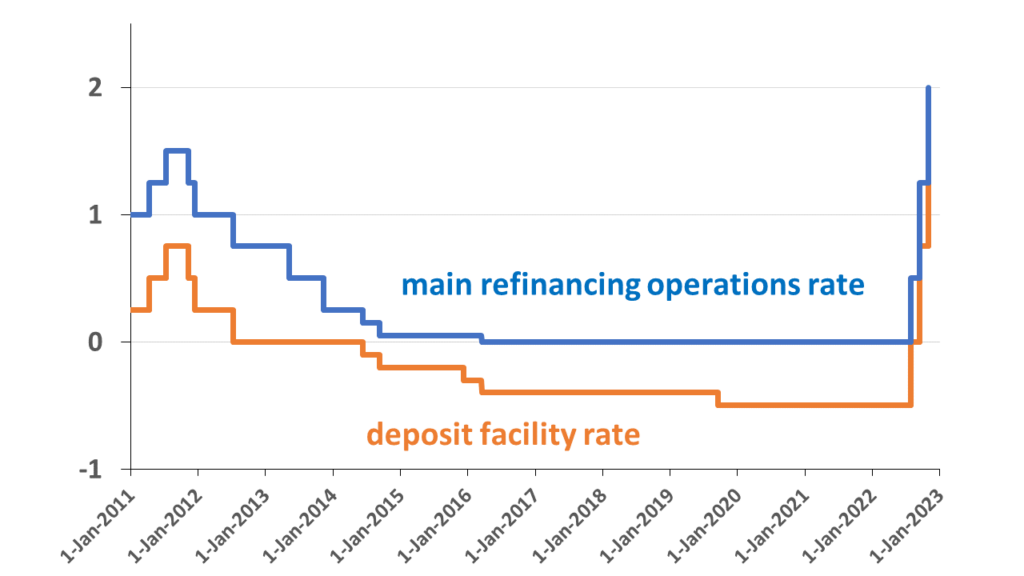

The ECB pays the deposit facility rate on money that banks have deposited at the ECB. That’s similar to the interest rate you receive on your savings account.

Banks can also borrow money from the ECB for a short period. These seven day loans are called “main refinancing operations” (MRO). The main refinancing operations rate is the interest rate that the ECB receives on these loans.

The ECB has increased the deposit facility rate and the main refinancing operations rate already three times in 2022.

Before these rate hikes, the deposit facility rate had been negative since 2014. And for previous rate hikes, we even have to go back to the year 2011. As of 2 November 2022, the deposit facility rate will be 1.5 percent and the main refinancing operations rate will be 2 percent.

How much money will the ECB pay to banks or receive from banks?

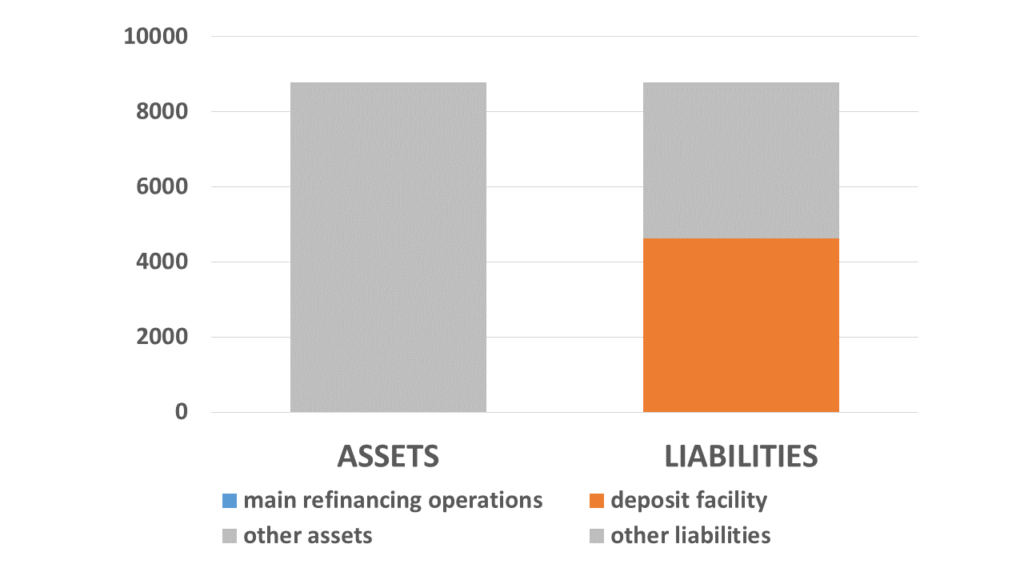

To answer that question, we need to look at the balance sheet of the ECB. The ECB has a balance sheet of almost 8.8 trillion euro (8,800 billion euro).

At 4.6 trillion euro, the deposits of banks in the deposit facility make up a little more than half of the ECB’s liabilities.

I didn’t forget to include the main refinancing operations, but these loans are less than 4 billion euro, so you cannot see them on the asset side of the balance sheet.

How much will the ECB pay to banks?

4.6 trillion deposits times a deposit facility rate of 1.5 percent means that the ECB will pay 69 billion euro to banks. The ECB will actually pay a little more, because banks also have something called “minimum reserves” at the ECB. And by the end of 2022, the ECB will also pay the deposit facility rate on these minimum reserves. Before [21 December 2022], it paid the main refinancing operations rate.

Lagarde: “The Governing Council also decided to change the terms and conditions of the third series of targeted long-term refinancing operations known as TLTRO III.”

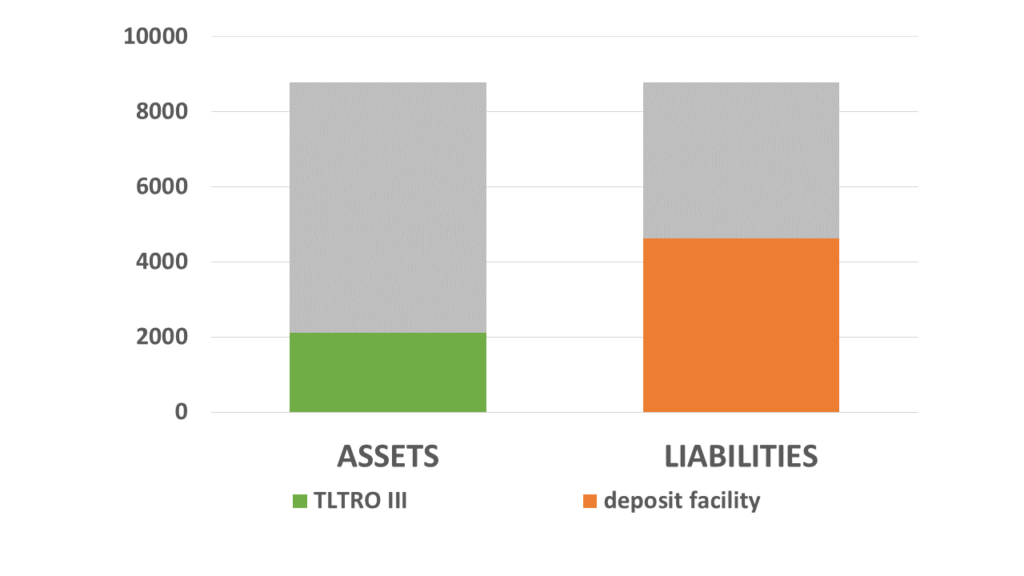

So TLTRO III are three-year loans made by the ECB to commercial banks. The ECB offered these loans between the end of 2019 and the end of 2021. What was special about these three-year loans is that banks had to pay a negative interest rate to the ECB. So in fact they could borrow money from the ECB and pay back less than they had borrowed in the first place.

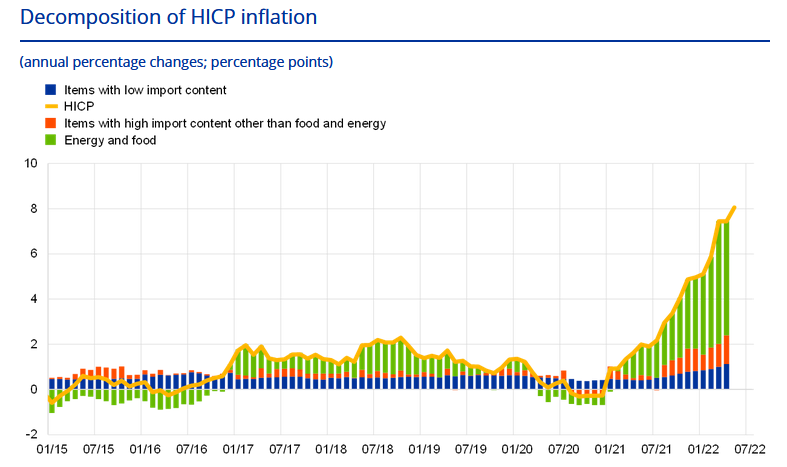

You can ask “why did the ECB do that?” Well, if you look at the inflation chart, you can see that at the time when the TLTRO loans were initiated, inflation was below the two percent target of the ECB. But now that inflation is far above the two percent target, the ECB has decided that these negative rates on the TLTRO loans are no longer justified.

And so they have decided to increase the interest rate for the remainder of the TLTRO period to the deposit facility rate. For banks that have outstanding TLTRO loans and also deposits in the deposit facility, the ECB has made it possible to repay the TLTRO III loans early3. This will have the effect that both the assets and the liabilities of the ECB go down, so this will shrink the balance sheet of the ECB.

To recap: the ECB has increased the main refinancing operations rate to 2% and the deposit facility rate to 1.50%. The ECB will pay the deposit facility rate on the deposits and minimum reserves of banks and it will receive the deposit facility rate on the TLTRO III loans of banks.

Taking into account the interest that the ECB pays on the deposit facility and the minimum reserves, and the interest it receives from the TLTRO loans, in one year the ECB should be paying 41 billion euro to banks at the current level of the deposit facility rate (1.5%).

If you are Christine Lagarde and you want to improve your communication, I suggest you read my book Bankers are people too, in which I explain how banks and central banks work using cartoons and also a lot of balance sheets but especially lots of stories about banks and central banks.

I have focused on the technical details of higher interest rates and the TLTRO loans, but of course since the ECB is responsible for price stability, the question is: will higher rates actually help to reduce inflation?

I did an entire video on inflation in Europe (not just in the euro area, but also in countries with other central banks than the ECB) and to be honest, it doesn’t look very promising.

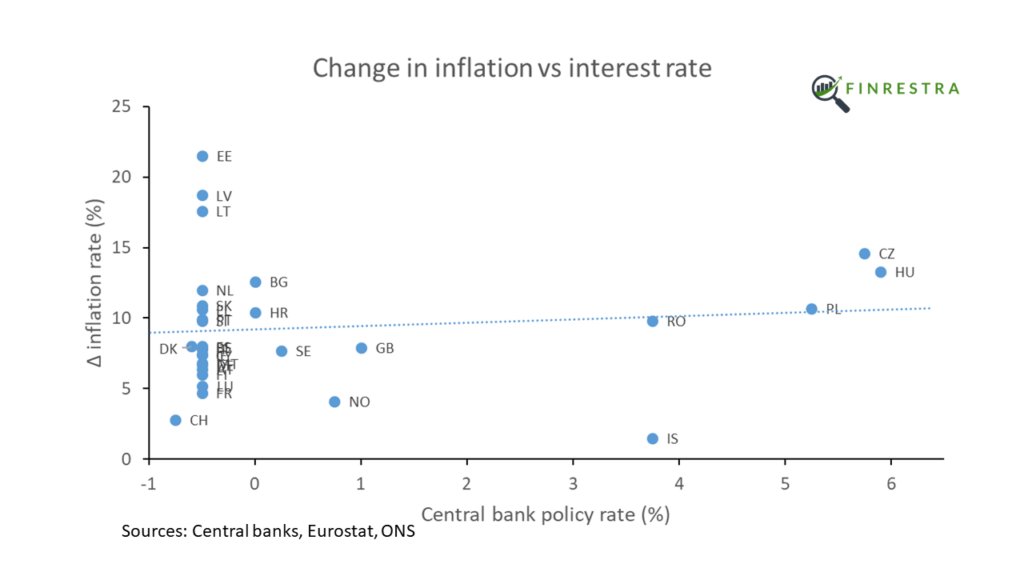

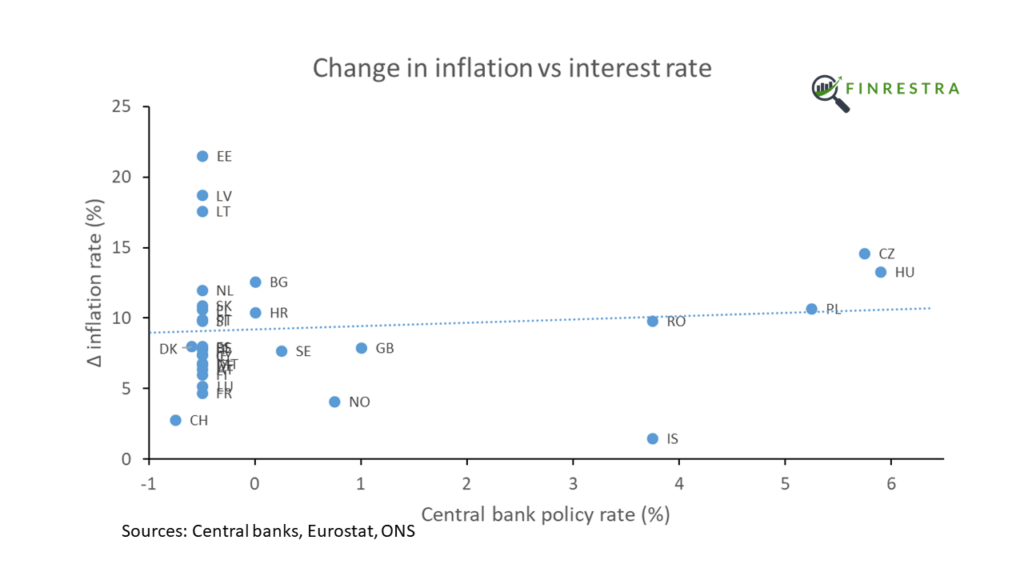

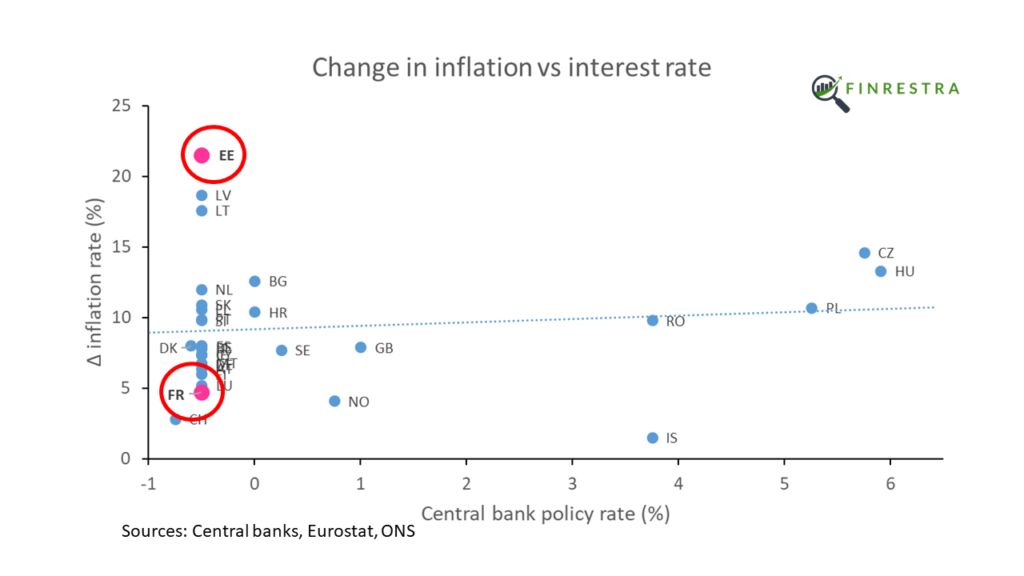

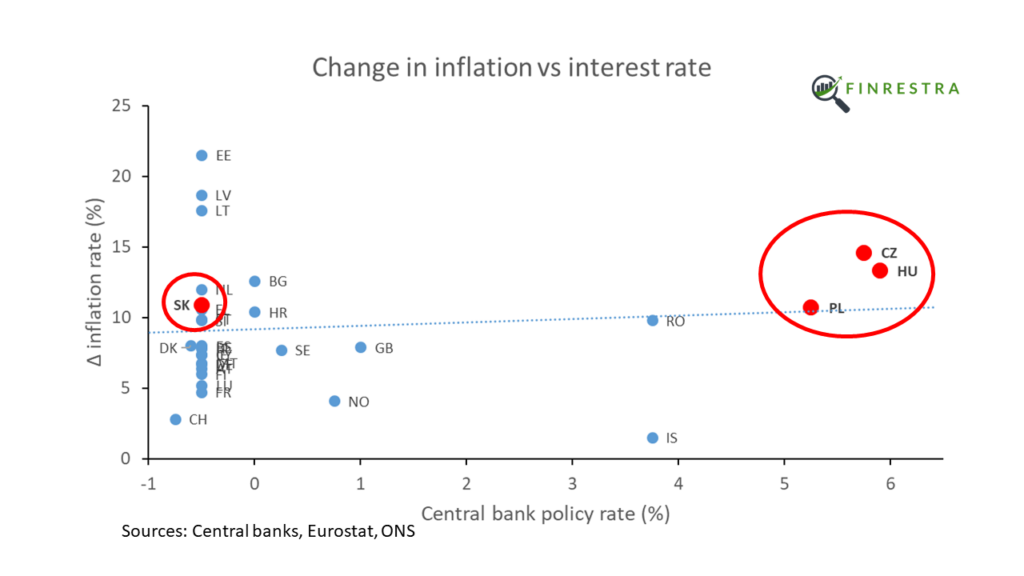

So here’s a slide that shows the increase in inflation and the central bank interest rate.

And so you can see that in certain central European countries like the Czech Republic and Poland the central bank has already increased interest rates a lot more than the ECB. But you can still see that there is no correlation between the central bank interest rate and the change in inflation in European countries.

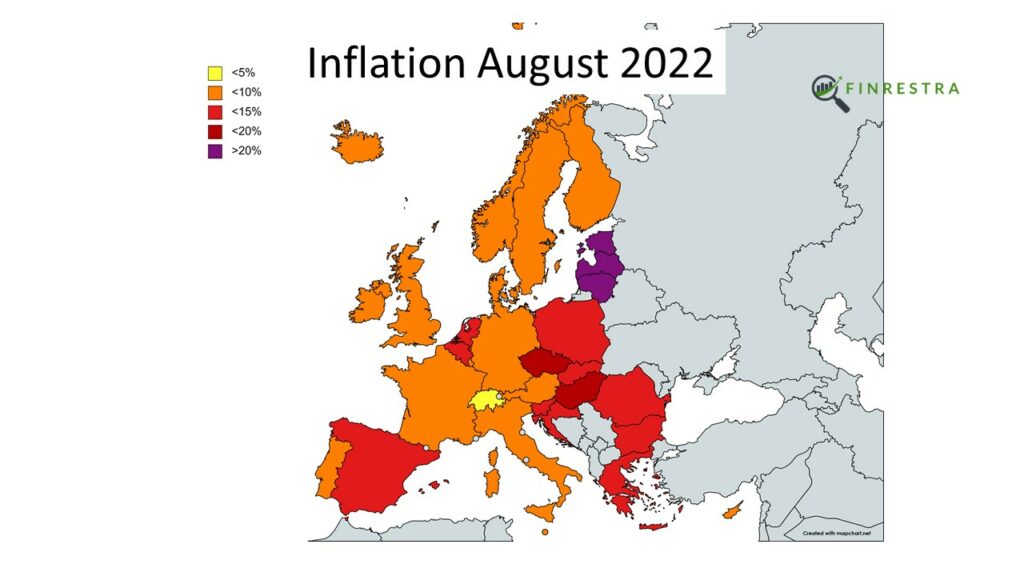

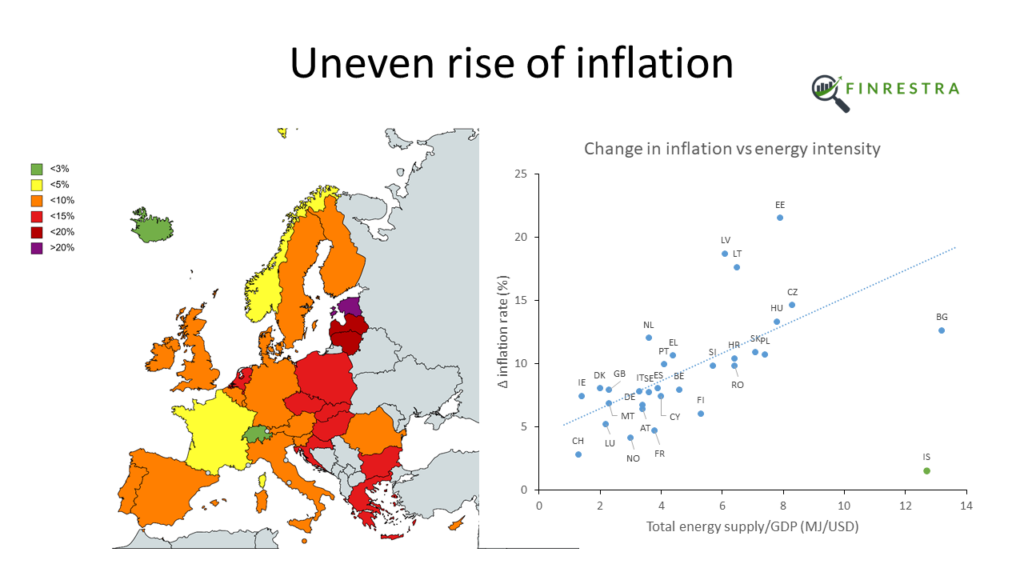

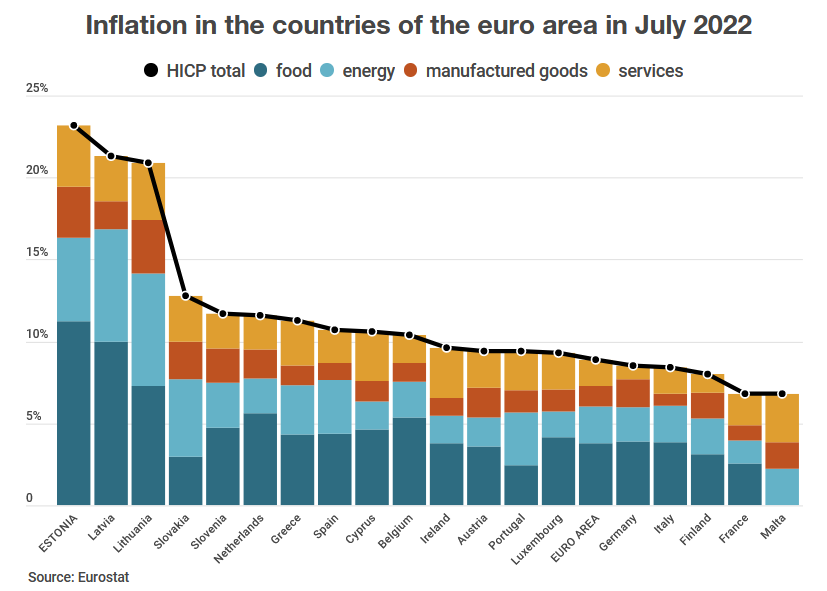

In June 2021, inflation was still close to 2%. In August 2022, it was above 10% in the European Union (EU) as a whole. But that number hides a remarkable divergence between countries. In Estonia, inflation reached a stunning 25% in August 2022. In France, it was 6.6%. In Switzerland, not an EU member state, inflation was just 3.3%.

HICP in 31 European countries. Sources: Eurostat (all countries except UK), ONS (UK). All maps in this post created with MapChart.

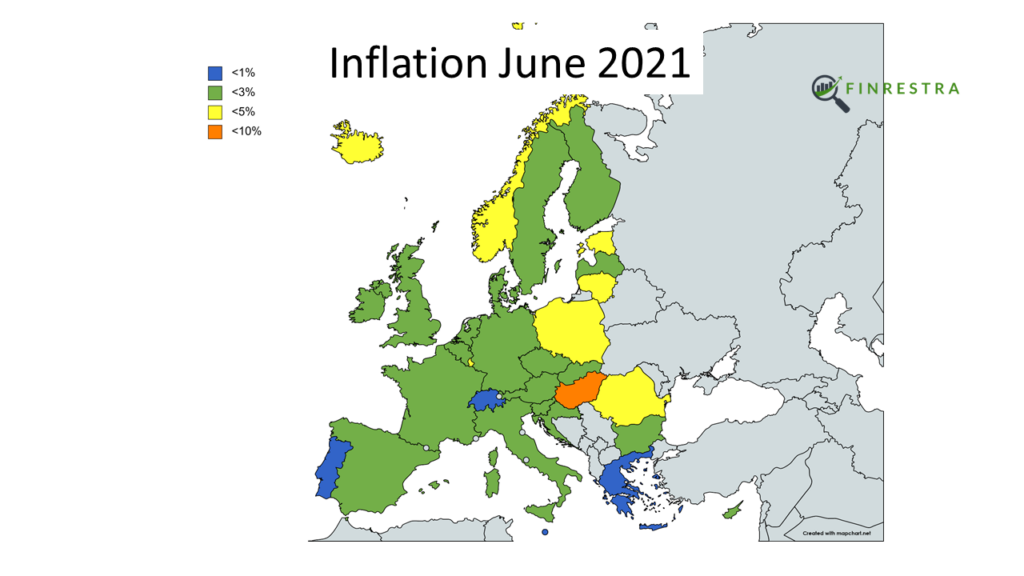

A year before, in June 2021, inflation was very close to 2% in most European countries. With 5.3%, Hungary had the highest inflation. Inflation was lowest in Portugal, at -0.6%.

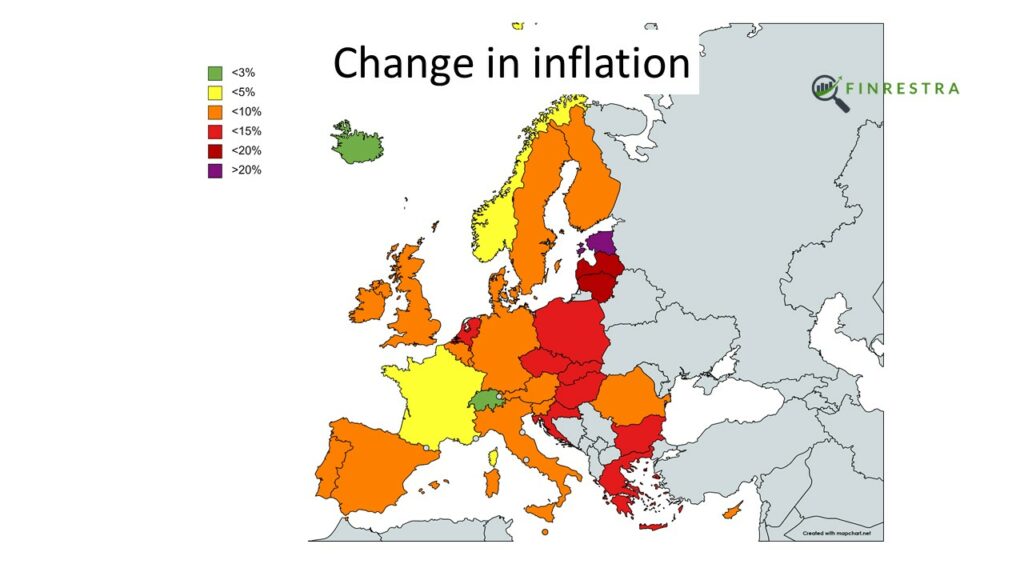

In this post, we’ll look at the change of inflation in 31 countries: the 27 member states of the EU, and the United Kingdom (UK), Norway, Switzerland and Iceland.

Inflation rise between June 2021 and August 2022.

How can we explain the dramatic, uneven rise in inflation?

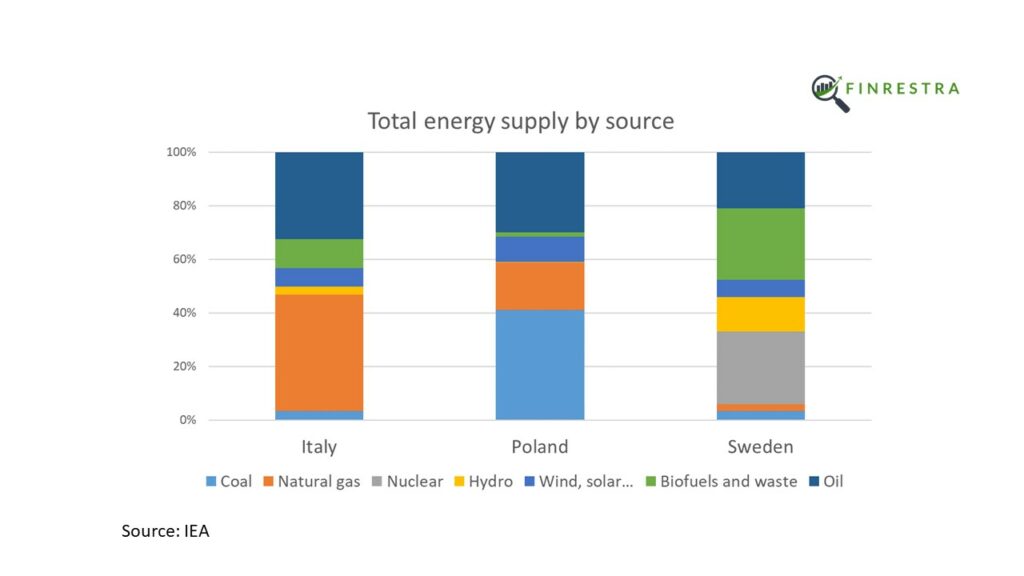

Energy intensity

Consumers are paying a lot more for energy than they used to. Companies also face higher energy bills, which has an impact on the price of their goods and services.

But energy prices are set on international markets, e.g. for oil, gas, coal and electricity. Why doesn’t expensive energy result in a similar rise of inflation across Europe?

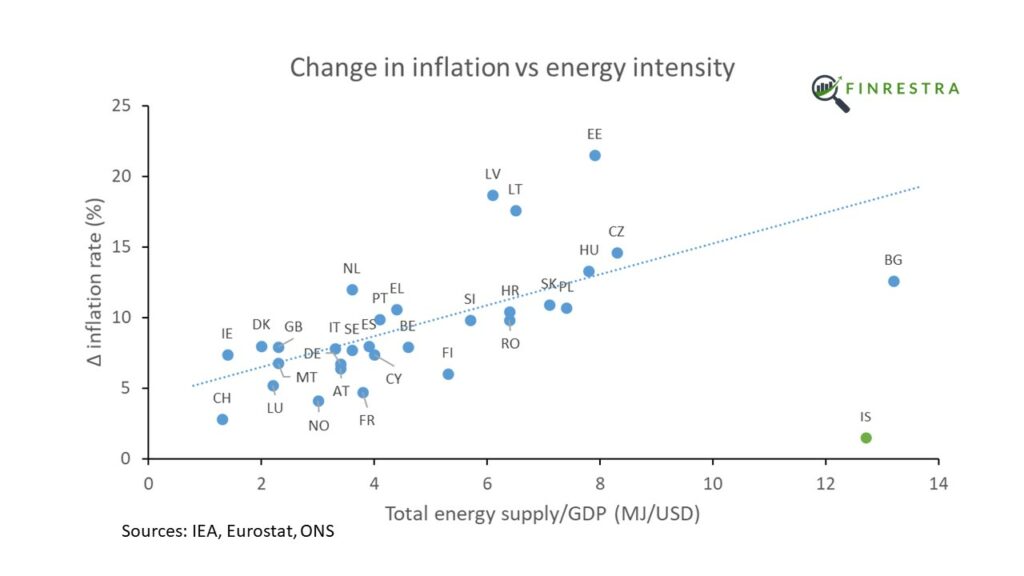

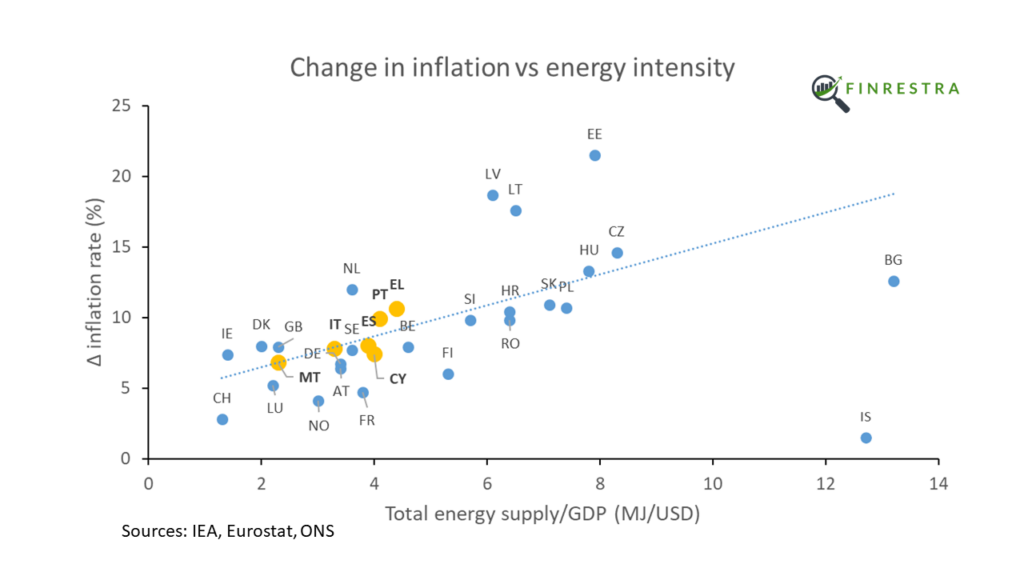

As the following figure shows, there is a strong correlation1 between the rise of inflation and the ratio of energy use to GDP2. As a general rule, the more energy a country needs to produce a dollar of economic output, the higher its inflation. Countries in Central and Eastern Europe have higher energy intensities and higher inflation rates than their Western European neighbors.

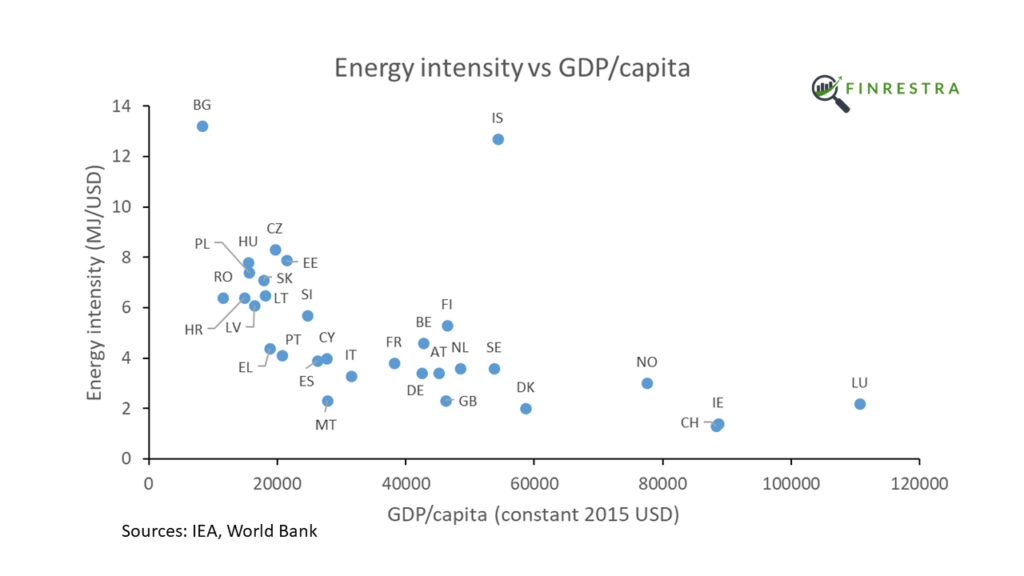

Countries with a lower GDP per capita tend to be more energy intensive.

So it’s not surprising that Central and Eastern European countries, who are relatively poor, are experiencing higher inflation than the West3.

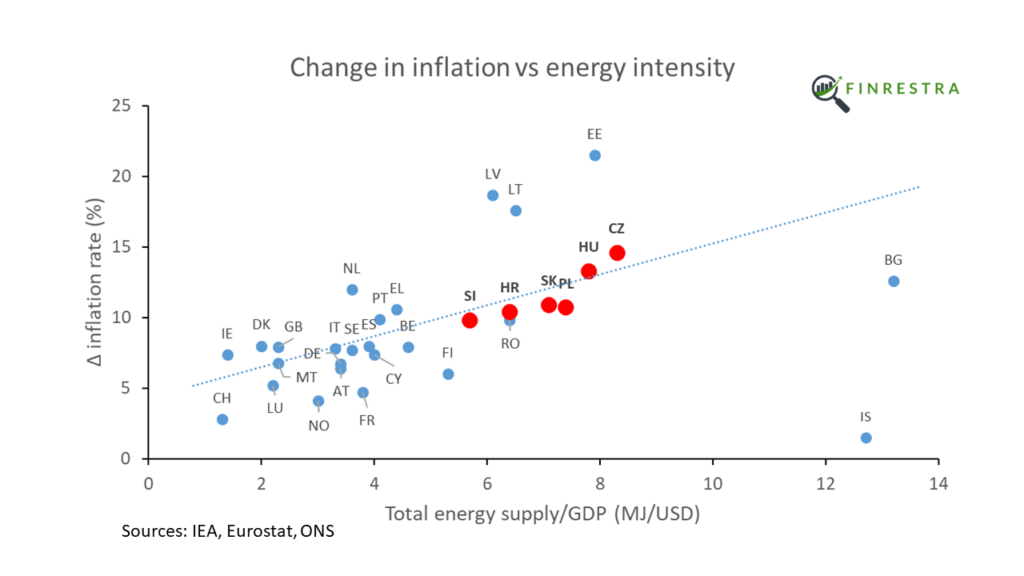

But it’s not just an East-West story. Even within regions with similar GDP per capita, the more energy intensive countries experience higher inflation. For example Central Europe4,

The picture is less clear in Western Europe. The energy intensity of Luxembourg and Ireland is distorted by the denominator (small countries with a very high GDP per capita due to the presence of international companies). France already limited energy prices in 2021. The Nordic countries are just weird ¯_(ツ)_/¯

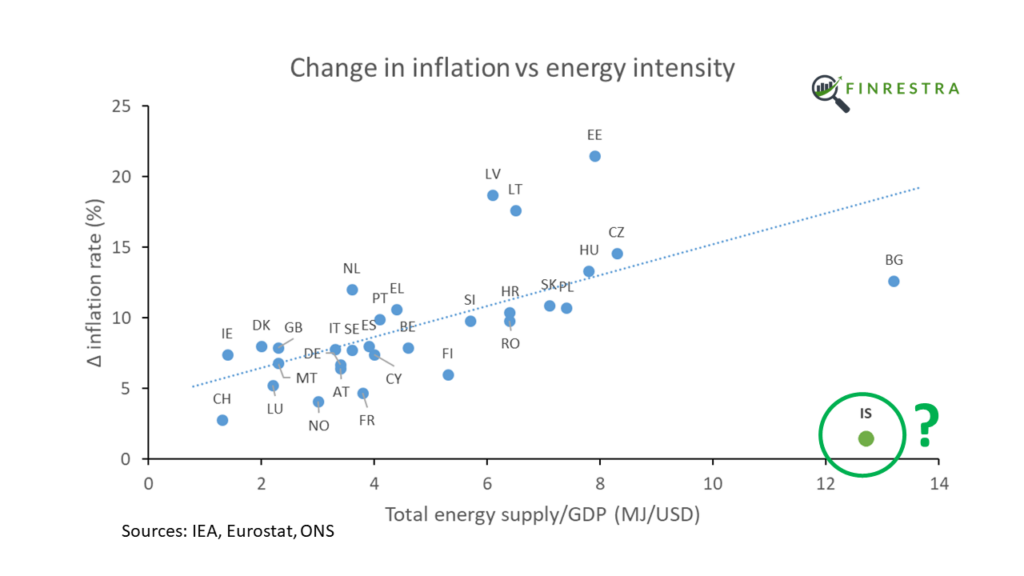

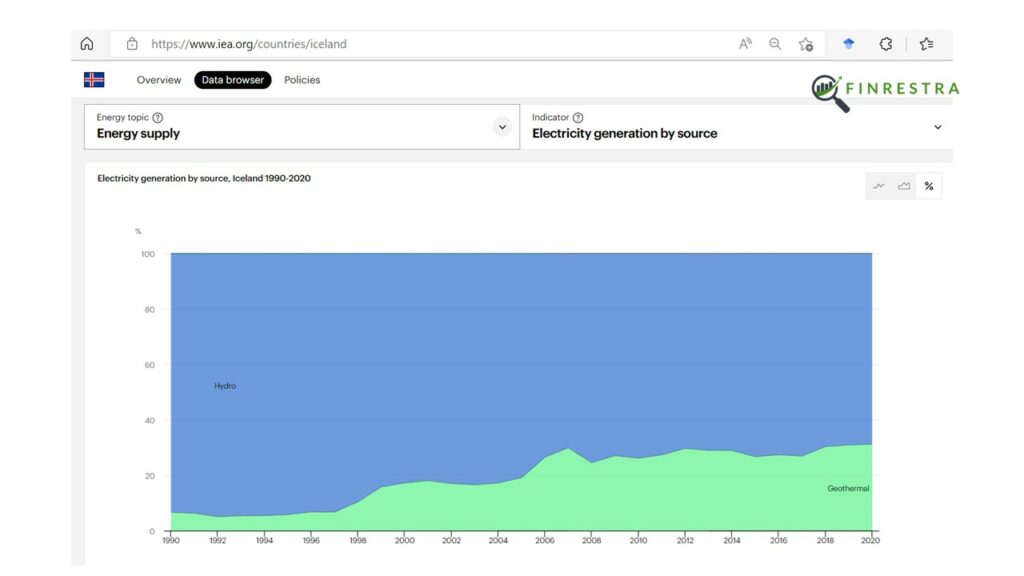

What’s going on in Iceland? Iceland is a rich country with an abnormally high energy use. Why doesn’t this result in much higher inflation?

What other factors could contribute to the rise of inflation?

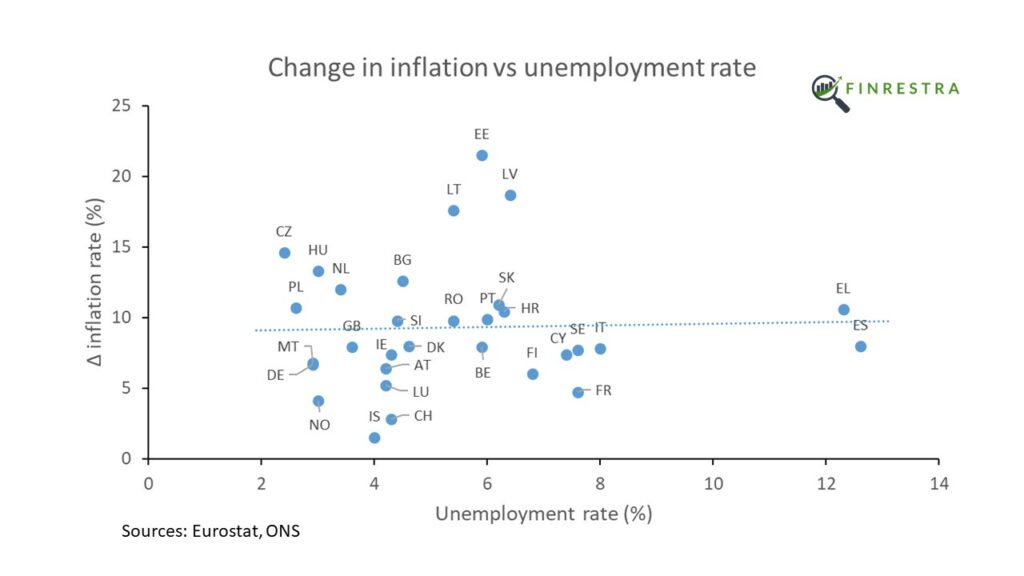

According to economic theory (NAIRU, Phillips curve), when unemployment is “too low”, workers demand higher wages. And higher wages lead to higher prices.

However, there is no correlation7 between unemployment8 and the change of inflation in Europe.

Inflation rose more in Spain and Greece than it did in Germany, although the German unemployment rate is much lower.

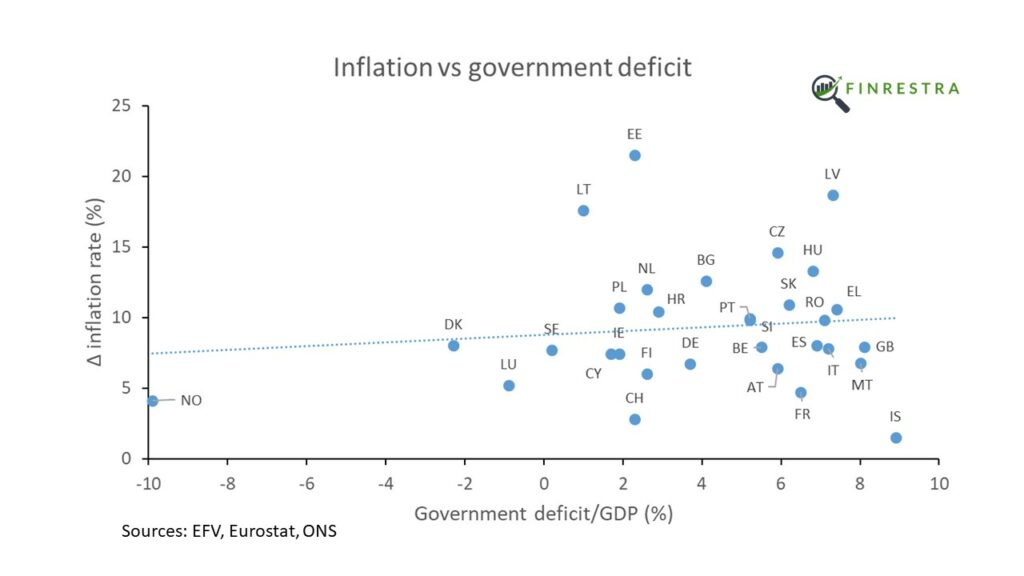

Government deficits and debt

Do deficits cause inflation (Fiscal theory of the price level)? It makes intuitive sense that if the government spends more money into the economy than it takes away with taxes, this deficit leads to inflation.

However, there is no correlation9 between government deficits10 and the rise in inflation.

Denmark and the UK have the same change in inflation, although the Danish government ran a budget surplus in 2021, while the British had an 8.1% deficit. Finland and Estonia had similar deficits, but their inflation numbers are very different.

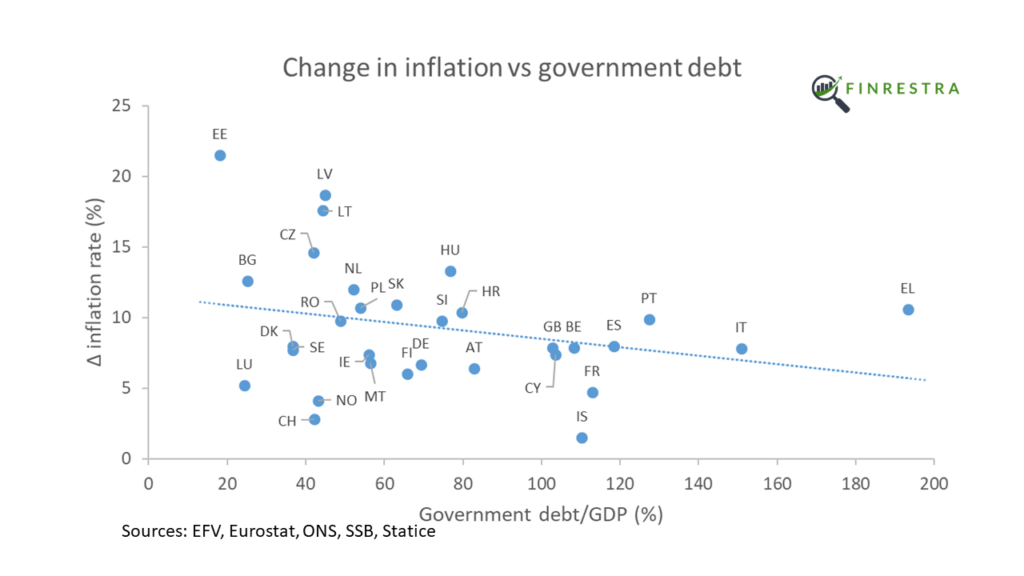

What about public debt? Maybe inflation goes up because people lose confidence in the sustainability of the debt. Or because governments choose to inflate away the debt.

However, there is a slightly negative relation11 between government debt and inflation12.

Greece, with its massive government debt, has experienced a smaller rise in inflation than the Baltic countries, where government debt is very low. Estonia has both the lowest government debt to GDP, and the highest inflation in Europe! Inflation is higher in the Netherlands than it is in Italy, although Italy’s debt-to-GDP ratio is almost 100 percentage points higher.

The picture shows central bank policy rates13 on June 1, 2022. Since that time, central banks have raised interest rates in an attempt to tamp down inflation.

But it’s not clear that interest rates have an effect on Europe’s inflation. In the euro area, where the ECB sets monetary policy for all 19 member states, inflation rose by 4.7% in France and 21.5% in Estonia.

In Slovakia, a country with a negative interest rate, the rise in inflation (+10.9%) is similar to neighboring Czech Republic (+14.6%), Hungary (+13.3%) and Poland (+10.7%), where policy rates were over 5%.

Conclusion

In conclusion, Europe’s worse inflation in generations is driven by energy. Conventional factors monitored by central banks don’t seem to play a role.

Contact

This work started as a small project I did during the summer, using June 2022 inflation instead of the change of inflation (see tweet below). In this post and in the video, I used the latest available data. I also added six countries (Bulgaria, Croatia, Cyprus, Malta, Romania14 and Iceland) to the dataset.

If you have any questions or suggestions about this work, you can find me on Twitter @janmusschoot or mail me at jan.musschoot@finrestra.com.

For my professional services, please contact me on Linkedin or mail me at jan.musschoot@finrestra.com.

Energy use per GDP explains the vastly different inflation rates between European countries. pic.twitter.com/U1lVqF5BAp

— Finrestra 🎙️ podcast (@JanMusschoot) July 25, 2022

Statistical robustness

Twitter user Rasmus checked the data points I posted in June. His test shows that the regression line slope is different from zero:

…and I'm wrong (I think), I tested for equal means, and not whether the regression line slope is different from "0". Actually testing for that gives me an 0.0013 % chance that the slope is "0", but don't take my word for it! https://t.co/C3lIgNJAjSpic.twitter.com/LQu8jgKGKT

It is remarkable that there is such a strong correlation between inflation and energy intensity, given the different energy mix between countries. For example, natural gas is the most important fuel in Italy. Poland mostly burns coal, while Sweden relies on wood. While natural gas and coal prices are up hundreds of percent, that’s not the case for oil or nuclear.

Other complicating factors that my analysis doesn’t take into account are price caps for energy (e.g. France), and the energy intensity of exporting industries (which should have less of an effect on domestic consumer price inflation).

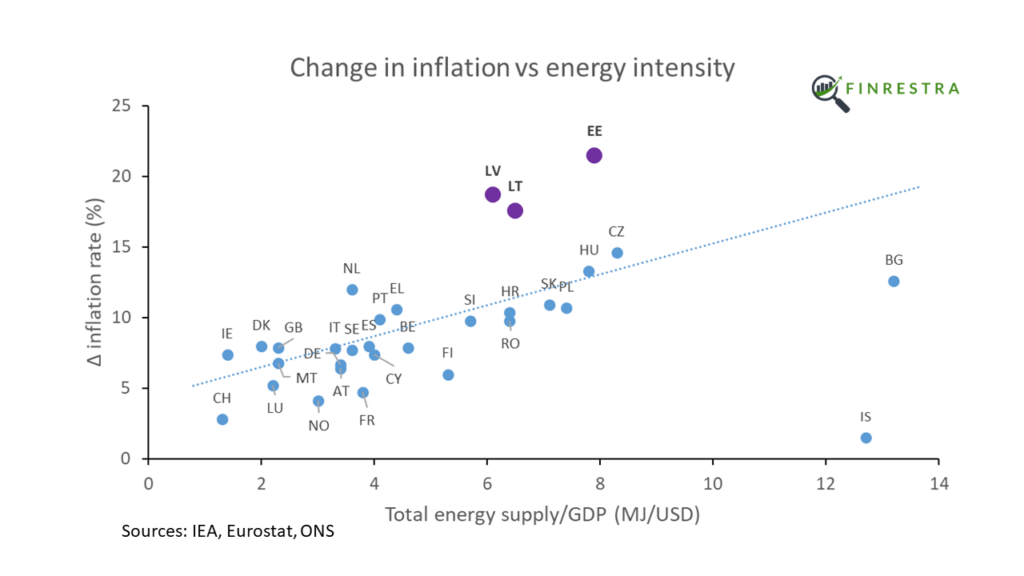

What’s the deal with the Baltics?

The three Baltic countries (Estonia, Latvia and Lithuania) are outliers. Their inflation is much higher than we’d expect based on their energy intensity. It’s not obvious that the fact that they share a border with Russia is the explanation. Finland, a euro country like the Baltics, also borders on Russia and has a relatively low inflation.

There are several reasons why inflation is higher in the Baltic states than the average in the euro area. The share of energy goods in the purchasing basket of consumers in the Baltic states is larger, which has affected the rise in the price of the consumer basket. Natural gas and electricity were a little cheaper in the region before Russia’s invasion of Ukraine, but prices have now caught up to those in other countries.15

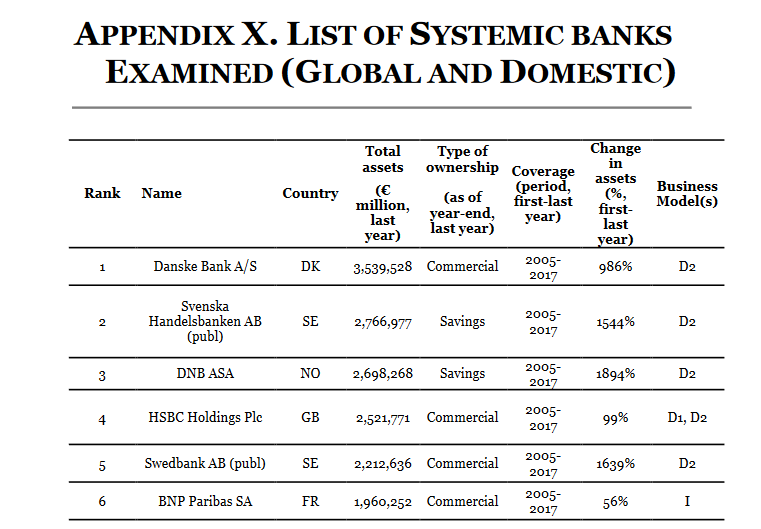

Please take into account exchange rates, Ayadi et al. Even if you don’t know that HSBC and BNP Paribas are the largest banks in Europe, the change in assets of the Nordic banks should have been a huge red flag.

The same study classifies HSBC as a retail bank and La Banque Postale as an investment/wholesale bank. I’ll take common sense over fancy statistical software any day…

I hate to bring this up on the first (working) day of 2022, but the primary objective of the ECB is still price stability.

With inflation close to 5%, it seems that talking and tweeting about the ECB’s secondary objectives is more important than delivering stable prices.

Within a year’s time, your economists have doubled their projections for inflation in 2022.

🇪🇺 New @ecb staff projections. Key figures: 3.2% inflation in 2022 (!), but headline and core inflation at 1.8%, close to but *below* 2% target. pic.twitter.com/Y5On3eIPsv

So you’ll understand that people don’t believe you when you say that inflation will go down this year.

If you do choose to stay ECB President in 2022, I wish you a firm hand.

On New Year’s day, the 20th birthday of the euro, you called the euro a “beacon of stability and solidity around the world”.

To keep it that way, the ECB will need your strong leadership.

Happy birthday to the euro! 20 years since the launch of euro cash, our currency is a beacon of stability and solidity around the world – thanks to you, the hundreds of millions of Europeans who use it every day. https://t.co/BZBSZeRR9J

Hello and welcome to a special episode of the Finrestra podcast.

I wish you a happy new year! Stick around till the end, because I’m giving away 250 euros.

New year, new month, so here’s a quick recap of the European financial news of December.

Santander has to pay almost 68 million euros to Andrea Orcel. Santander had offered the former UBS banker the role of CEO, but withdrew its offer.

In other legal news, a French court has reduced a 4.5 billion euro fine for UBS to 1.8 billion euro. The Swiss bank was found guilty of money laundering.

Dutch green bank Triodos will set up a multilateral trading facility for its shareholders (technically certificate holders). Since the beginning of 2020, shareholders cannot sell their certificates. It is expected that trading will resume at a price that is 30 or 40 percent lower than before the pandemic.

There was also consolidation and divestment news.

BNP Paribas has agreed to sell its American subsidiary Bank of the West for 16.3 billion dollars. Listen to episode 9 of the Finrestra podcast for our take on this transaction.

Cooperative bank Crelan acquires AXA Bank Belgium. The deal had already been announced in 2019, but was waiting for approval by the ECB. The new bank will be the fifth largest in Belgium.

Regular listeners know that I usually do an in-depth analysis of one topic after the news. However, today I want to tell you a bit about Finrestra and my plans for 2022.

I started this podcast because there are not many podcasts focused on European finance. My original goal was to do a weekly interview. But I quickly found out that this is easier said than done. Weekly episodes require more time than I have. And it hasn’t been easy to find people who want to come on the show. So I want to thank my first guests Uuree Batsaikhan, Koen Vingerhoets and Rik Coeckelbergs again!

For 2022, there will be two episodes per months. I hope that from February onwards, I will be able to interview a number of very interesting guests. Stay tuned!

If you’re listening to this podcast on Apple or Spotify, you may not know that there is also a Finrestra YouTube channel, where I post short videos about financial topics. For example, I have a series of bank profiles, including of Santander, Triodos, BNP Paribas and ING, which were all mentioned in the news recap. I also want to create more videos with short stories about European finance.

But neither the podcast nor YouTube pays my bills, and this is where you can help me. Don’t worry, I’m not asking for money, I’m giving you a chance to win money!

Finrestra stands for Financial Research and Training. So far, we have mainly worked for Belgian based clients. But I want to expand my activities to the rest of Europe. If you share my YouTube video with my two courses for 2022 on LinkedIn and tag a friend before 25 January, you can win 250 euro. I’ll put the link in the description.

This has been another episode of the Finrestra podcast. You can find my on twitter @janmusschoot. You can mail me at jan dot musschoot at finrestra dot com.

Thanks for listening and I hope you have a great 2022!”

Euro area inflation remains far above the ECB’s 2 percent target. Dutch inflation was 5.2 percent, a figure not observed since 1982. The German inflation rate was the highest since 19 ninety 2. Ironically, the union of the ECB’s own employees wants higher wages due to inflation.

In other record news, the French stock market index CAC 40 reached a new all-time high. It finally surpassed its peak from the year 2000.

There was also consolidation news:

BBVA wants to buy the stake of Turkish Garanti BBVA bank it doesn’t own yet

KBC buys the Bulgarian banking activities of Raiffeisen Bank International

The news of record high stock prices brings us to the topic of this episode: European bank CEOs should be ashamed.

Why?

Because their stocks have been horrible investments. Despite a nice rally in 2021, most large European banks still trade 70, 80 or 90 percent below their 2007 highs.

Or look at banks by market capitalization. The biggest European bank, HSBC, is only worth a quarter of American JP Morgan. And you could argue that HSBC isn’t even really a European bank, as most of its profit is generated in Hong Kong.

What’s the second largest European bank by market cap? Surely it must be a German, British or French one? Nope. It’s actually Sberbank of Russia. Russia, a country with a GDP smaller than Italy’s.

I can hear some CEOs already. How they are victims of low interest rates, low growth, overcapacity. Blah blah blah.

Instead of making excuses, take a hard look at banks like DNB, KBC, Nordea and SEB. Why are these relatively small banks worth more than giants like Deutsche Bank, Société Générale and UniCredit?

I know the answer. But do bank CEOs?

Here’s some free advice. Listen to episode 3 of the Finrestra podcast. And watch the “Bank in two minutes” series on our YouTube channel.

What will you learn? That successful banks focus. Focus on a few countries. Focus on one client segment, or at least on very complementary segments.

In contrast, banks with low profitability are often monsters of Frankenstein. They are part retail bank, part investment bank. They are active in dozens of countries.

They are big, but do they deliver what clients and investors want? The market doesn’t think so.

Now dear listener, before I go, I want to ask you a favor. For an upcoming episode, I would like to talk about Industry, the series about junior investment bankers. I recognized a lot of situations in the series. So if you work in a bank, watched Industry and would like to talk about it, please contact me! This has been another episode of The Finrestra Podcast. If you have suggestions for topics or guests, you can mail me at jan.musschoot@finrestra.com. You can find me on twitter @janmusschoot. Thanks for listening!”