I’m trying something new. I’ve started making videos about banking, monetary policy and sustainable finance.

I’m still trying to figure out the best format. But I already like the ability to use graphs and pictures. Compared to blogging, video is less nuanced. For example, you can’t link to all sources. But maybe that’s an advantage.

Conny Olovsson (Riksbank) argues that “monetary policy does not have the appropriate tools for counteracting global warming, but global fiscal policy is significantly better suited for this purpose.”

Isabel Schnabel (ECB) argues that climate risks are mispriced by financial markets. Central banks should not sustain market failures.

The fraction of bonds issued by carbon intensive companies in the ECB’s CSPP portfolio and accepted as collateral is far larger than the GVA of these companies, see e.g. Matikainen (figure 3) or Dafermos (figure 4).

Paris Agreement, Article 2, 1(c): This Agreement, in enhancing the implementation of the Convention, including its objective, aims to strengthen the global response to the threat of climate change, in the context of sustainable development and efforts to eradicate poverty, including by: Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.

Lagarde has said climate change is the job of the ECB: “[w]hether climate change (…) is to be considered as part of our primary objective. And the answer is yes.” (1:44)

A green mandate for the ECB? Dirk Schoenmaker says yes, Hans Peter Grüner says no.

Tommaso Valletti on how the EU anti-monopoly system works in practice (On the role of economic consultants arguing in favor of M&A: “They produce a glossy pamphlet with three nice pages: exactly what the judge needs, he can say ‘ah, here is a counter-argument, here is an anecdote to rebut this. So, nobody knows’.”; On the capabilities of the EU: “DG Comp has less than 1000 people for half a billion citizens.”)

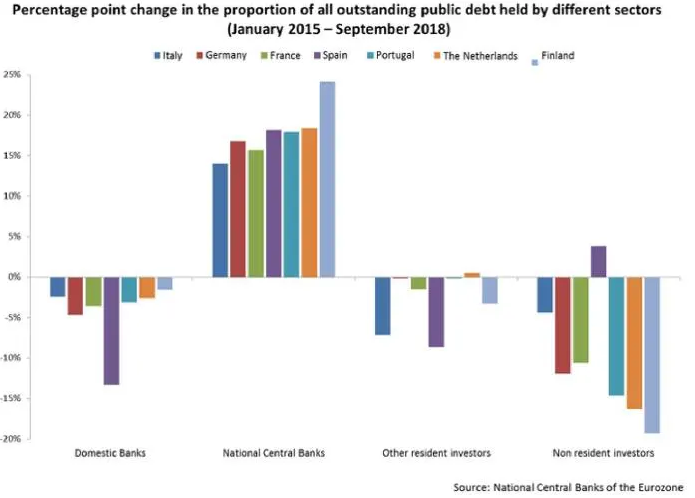

Mainly non-resident investors, although there are national differences, as this graph by Marcello Minenna shows:

What did companies do with the money from the ECB?

Corporates used the attracted funds mostly to increase dividends, according to research by Karamfil Todorov.

Did QE ease financial conditions?

Yes. Karamfil Todorov found that the ECB’s Corporate Sector Purchase Programme (CSPP) “increased prices and liquidity of bonds eligible to be purchased substantially”1.

Can we trust central bank research on the effect of QE?

Central bank researchers face strong incentives to be positive on QE. Brian Fabo, Martina Jančoková, Elisabeth Kempf and Ľuboš Pástor found that “central bank papers report larger effects of QE on output and inflation. Central bankers are also more likely to report significant effects of QE on output and to use more positive language in the abstract. Central bankers who report larger QE effects on output experience more favorable career outcomes.”

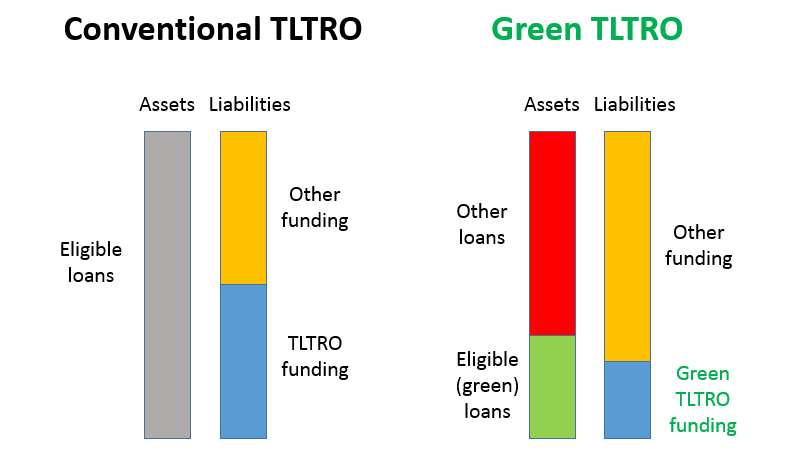

How can the European Central Bank (ECB) support a sustainable recovery? In a report for Positive Money Europe and Sustainable Finance Lab, Jens van ‘t Klooster and Rens van Tilburg propose that the ECB starts a Green TLTRO program.

Green TLTRO is a refinancing program for commercial banks. Banks can fund their green loans with longer term (several years) deposits from the European Central Bank (ECB). Green loans are bank loans that comply with the EU’s Green Taxonomy.

The figure below shows the balance sheet of a commercial bank with conventional (left) and green (right) TLTRO. Under TLTRO-III, the ECB funds 50% of a bank’s eligible assets. Under green TLTRO, the ECB funding is only available for green bank loans.

The interest rate on the Green TLTRO is determined by the volume of green bank loans. More green loans result in a lower interest rate on the funding from the ECB. With negative interest rates, banks have to pay back less to the ECB than they borrowed. This provides a strong incentive to banks to increase their lending to green projects, and to pass on the low rates to borrowers.

Is Green TLTRO a pie in the sky proposal? Only if you’re not keeping up with the times.

TLTROs are a well-established monetary policy tool. The ECB is currently doing TLTRO-III.

Today at 11:30CET we'll get the allotment for ECB's TLTRO-III.5. Expect a much smaller take-up than in June, although potentially above €50bn.

There's €5.7bn maturing and €10.9bn in TLTRO-II repayments, so that excess liquidity would rise closer to the €3tn mark. pic.twitter.com/ikjvAtQ8Av

In a recent speech, ECB Executive Board Member Isabel Schnabel pointed out that climate change is a market failure. She said that collective action, including by the ECB, should correct this market failure and accelerate the transition towards a carbon-neutral economy.

Asked about the Green TLTRO report by MEP Bas Eickhout, ECB President Lagarde said that “climate change has to be part and parcel of our strategy review. Not because it is a secondary objective, but because of its impact on price stability, because of its significant impact on risk assessment and risk management. And the Green TLTRO, as you called it, is a matter that is of interest and that we will look at.”

What volume of green loans should the ECB target during the first 3 years? How low should the interest rate on Green TLTRO be? Should the eligible bank assets include loans to households for house purchases, a category that is currently exluded from TLTRO?

In a webinar on 12 October 2020, Jens van ‘t Klooster discusses the Green TLTRO proposal with Isabel Vansteenkiste (ECB) and Frederik Ducrozet (Pictet).

Update 2020/10/18: this is the video

Full disclosure: I have done consulting work for this report.

Ancient history: “In 2003, refinancing via LTROs amounts to 45 bln Euro which is about 20% of overall liquidity provided by the ECB.” (On June 18, 2020, banks borrowed 1.31 trillion euro from the ECB via TLTRO!)

The German Federal Constitutional Court (Bundesverfassungsgericht) made a decisionconcerning the ECB’s QE program1.

This article explains how the ECB can defend itself.

But I want to play devil’s advocate, and defend the German judges.

Despite buying thousands of billions of euros worth of bonds, the ECB has undershot its inflation target for years. The Court has a point that buying vast amounts of sovereign debt doesn’t seem proportional to this disappointing outcome.

In fact, the ECB could achieve its primary objective of price stability with a much smaller balance sheet. For example by dual interest rates. Or by helicopter money.

Second, the Court could prohibit the Bundesbank from participating in QE. But buying German bonds was not needed for monetary policy anyway! It was a political decision to buy bonds proportional to the national capital key in the ECB.

Finally, the decision of the Court should force European politicians to fix this mess. Maybe the ECB should have a dual mandate like the Fed has, so inflation and employment carry the same weight in monetary policy decisions. Or they could change the structure of the Eurosystem. Do we still need 19 national central banks when we have the ECB? Sounds like a make-work scheme to me…

On the Macro Musings podcast, Ashoka Mody says1 countries like Italy need fiscal transfers from other member states.

But fiscal burden sharing is a toxic idea, as Dutch finance minister Wopke Hoekstra demonstrated.

What’s the real problem?

Italy is 135% of GDP. Spain and France are 100% of GDP, so three of the big Eurozone countries are not going to be able to do fiscal stimulus of 5, 7, 10% of GDP, which is basically what is going to be needed for this crisis. We’re going to need enormous amount of fiscal stimulus. Maybe Germany will do that. In the US, with this two trillion, they’re already at about 9% of GDP, and I expect that it will go up even more, for a number of reasons, but Italy cannot do anything close to that, or Spain cannot do anything close to that.

Every country should do whatever it takes to save its economy. Bail out businesses, pay unemployment benefits.

The expenditures can be funded by bonds. The ECB should keep the spreads low. That means buying whatever it takes.

Secondly, the ECB is once again neglecting its primary objective. Oil prices and unemployment point to low nominal aggregate demand. Without income support to households, it’s unclear how the ECB can achieve its inflation target.