This post was originally intended to be published elsewhere, but ultimately wasn’t. Note that this article is only about helicopter money. However, governments and central banks urgently need to do much more. The state should bail out all businesses. Businesses should hold on to their employees even if they cannot work so the economy can have a V-shaped recovery. The government should pay the workers. I also have other proposals for the ECB, see here and here.

Continue reading “Helicopter money as a weapon in the war against the coronavirus crisis”Tag: ECB

How the ECB can stop the coronavirus crisis overnight

I haven’t posted on the blog in a while, but I’m very active on Twitter.

Here’s my 3 point plan for the ECB:

(1) The ECB should issue bonds, which are risk free (the ECB cannot default on euro liabilities). It should buy every sovereign bond trading at a yield of 40 basis points or more above the yield on the ECB bonds.

(2) The ECB should set the interest rate on TLTROs at -5% until six months after the coronavirus public health crisis is over.

(3) The ECB should do helicopter money as soon as businesses are operational again, because the outlook for price stability is bleak.

WTF is the ECB doing???

Total radio silence while markets are imploding. This is Trichet level incompetence. Criminal!!!

This is not a drill

The ECB, government leaders and the banking sector must act immediately to stop the financial panic caused by the coronavirus.

A recession can still be avoided.

Banks should provide bridge loans to businesses suffering from the corona shock.

The ECB should do a TLTRO-like operation, providing cheap funding proportional to banks’ SME/corporate credit portfolios. Make the terms of the ECB loans conditional on coronavirus metrics. For example: banks should repay 4 months after the last new COVID-19 case is detected in the EU.

If Europe’s leaders fail to act decisively, the financial costs will snowball.

Larry Summers is a VSCO girl. On central banks, fiscal stimulus, and why you should read Eric Lonergan

In case you’re not familiar with teen culture, VSCO girl is a fashion trend.

Surely, the Very Serious People who think about central banks are not susceptible to such fads, right?

I regret to inform you that the Very Serious economists and central bankers are just as prone to trends as teens on TikTok.

Continue reading “Larry Summers is a VSCO girl. On central banks, fiscal stimulus, and why you should read Eric Lonergan”The Owl of Frankfurt: Lagarde discovers her powers

Big shoes to fill

Christine Lagarde took over the ECB from Mario Draghi in 2019. Draghi was widely respected as the man who saved the euro. He promised to do ‘whatever it takes’ when prices for bonds of large euro countries were unsustainably low. Furthermore, Draghi introduced monetary policy tools that were considered radical at the time, such as quantitative easing (buying bonds) and targeted refinancing operations (lending to banks).

Critics suspected that Lagarde would be no match for her predecessor. Indeed, Draghi was an economist and former banker. By contrast, Lagarde was ‘merely’ a lawyer and politician.

Maybe that is why her opponents would systematically underestimate Lagarde. Time and again during her presidency, she followed the same strategy. Instead of trying to come up with new ideas herself, she listened to all options. Not just those of an inner circle of old central bankers and professors, but especially the alternatives suggested by junior staff and independent thinkers. Once Lagarde made up her mind on the right course to follow, she used her political skills to win the day.

The 2020 review

But let’s return to the start. Although Draghi’s ECB had performed better than under the disastrous Trichet, all was not well. Unemployment in the euro area was high. The ECB’s interest rates were negative. Inflation in the euro area was below the two percent target. The contemporary consensus said that the central bank was out of ammo.

It was in this context that Lagarde launched a monetary policy review. She wanted to know how the ECB could boost economic growth and fight climate change.

The policy review set in motion the bureaucratic cogs of the ECB. Meanwhile, Lagarde was subtly consolidating her power. She kept a tight grip on meetings and did not tolerate leaks. She also improved communication with national leaders and the European Parliament.

But most importantly, Lagarde read the Internet. And what she read did not make her happy. Lagarde’s advisors had assured her that the ECB’s hands were tied. They claimed that the institution was powerless in the current macroeconomic environment and that fiscal stimulus was needed.

But online, she discovered that central banks had historically used instruments that none of the very serious people were talking about. It was as if everybody suffered from amnesia.

In the spring of 2020, Lagarde held a secret meeting with three outsiders. The quartet of conspirators hatched a plan…

===

Next episode: the conference of the long knives

First episode: Paris, 2076

The Owl of Frankfurt: Paris, 2076

Eulogy by Aya Sissoko, President of the ECB, 8 January 2076

It is with great sadness that we say farewell to our honorary President and dear friend Christine Lagarde today.

Madame Lagarde will be fondly remembered as the fourth President of the European Central Bank, the predecessor of the Euro Central Bank.

Christine became President during a protracted malaise in the euro area. By throwing off the yoke of false dogma, she revitalized the ECB. Her curiosity, vision and political prowess changed the course of history.

Under her leadership, the ECB showed the world how to handle the climate transition. At the same time, the euro economy grew at a rate previously believed to be impossible.

Ask any of the Seven Bankers, and they will all agree: Christine was the first modern central banker. Her autobiography, published 30 years ago, is still a must-read.

Christine’s career set the gold standard for our profession. Not just for what she did during her presidency, but also for what she didn’t do.

Her resignation in the wake of the Crisis of 2033 was a clear statement against the all-powerful central banker. During her retirement, Christine refrained from commenting on current events.

Christine, Madame Lagarde, you were born Lallouette – the lark – but you will always be The Owl of Frankfurt.

On behalf of the 1.4 billion people who use the euro every day,

Bon voyage!

===

Next episode: Lagarde discovers her powers

ECB science fiction

Why is science fiction always about space or robots? Nobody cares about that kids’ stuff. ‘Pew pew, shooting at aliens’, how original 🙄

No, people want to read about central banks!

How did Christine Lagarde become the most powerful banker in history?

You’ll find out here, starting 02/02/2020…

Central banks will always be political

What do crypto enthousiasts have in common with defenders of independent central banks?

Based on the “Buy Bitcoin”-replies to ECB/Fed tweets, it seems the answer is “not much”.

However, that’s incorrect. Both groups think that their projects are apolitical.

Many central bankers view themselves as technocrats, divorced from politics.

But that’s a fantasy.

You see, anything a central bank does – even within its mandate – has political consequences.

Should monetary policy take into account climate change?

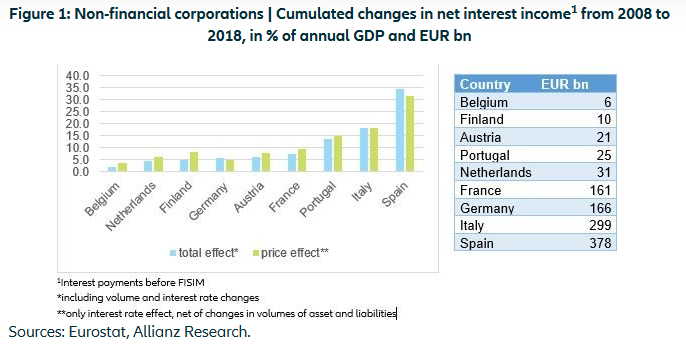

Should the central bank change interest rates or do QE to reach its inflation goal? Whatever option is chosen, monetary policy has distributional effects. For example, the German government has saved hundreds of billions in interest costs.

These two dilemmas illustrate that central banking is inherently political.

Therefore, economists should calculate the consequences of different monetary policy options. These scenarios will make the politics of the central bank’s actions explicit. For example, I estimated the effect of deeply negative interest rates (a proposal of Miles Kimball) on banks, governments, the ECB and the private sector.

Especially in the euro area, the ECB should take differences in asset mixes between countries into account.

Increased transparency will enable central bankers to defend monetary policy against criticism.

Update 26 January 2020: my arguments are obviously not new, see for example:

Hard work pays off

Remember Actually, lobbyists are good?

I wrote

it seems that the ECB is way ahead of the Federal Reserve when it comes to green central banking

Indeed, new ECB President Christine Lagarde acknowledged her institution’s climate responsibility at the European Parliament…

…and the European Investment Bank (EIB) will stop financing fossil fuel energy projects.

The hard work of the “climate and finance lobbyists” pays off!