Opiniestuk met Hans Bevers in De Tijd (11/06/2020):

Mik met een relanceplan op vaste kosten en investeringen

Enkele citaten in artikel Trends (26/03/2020):

Opiniestuk met Hans Bevers in De Tijd (11/06/2020):

Mik met een relanceplan op vaste kosten en investeringen

Enkele citaten in artikel Trends (26/03/2020):

Many European banks and insurance companies are trading well below their book value.

Large firms can unlock a lot of value by taking over smaller competitors, thanks to the negative goodwill. Consolidation would support the profitability of the financial industry.

Italian banks in particular would benefit from a consolidation of their fragmented domestic market1. In February, Intesa Sanpaolo launched a bid for UBI Banca. UniCredit should consider a similar deal with Banco BPM, Banca Monte dei Paschi di Siena or BPER Banca. Also, French BNP Paribas could merge its subsidiary BNL with one of those banks.

Spanish banking is already quite concentrated. Santander took over Banco Popular in 2017. The integration was completed in 2019. Santander and BBVA could acquire Bankinter, Bankia, or Banco de Sabadell. Of course, further domestic growth of the majors depends on regulatory approval. The two global Spanish banks definitely have the expertise to execute such an operation.

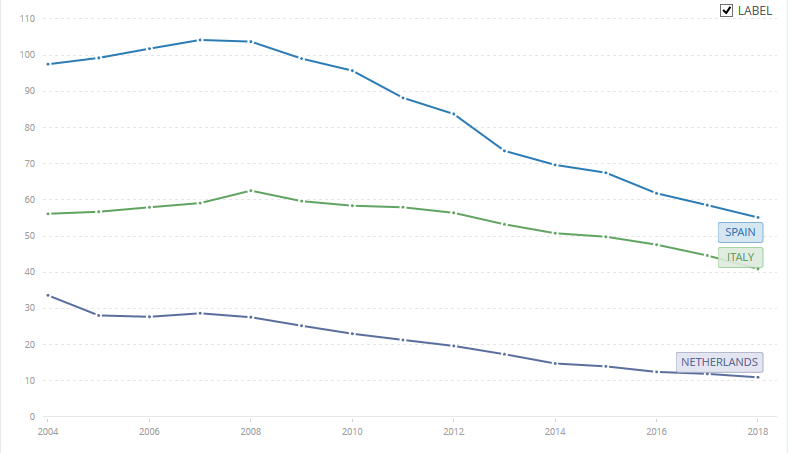

Figure 1 shows the number of bank branches relative to population for Spain, Italy and the Netherlands. It’s clear that Italy and Spain have a lot of potential for cost cutting.

In neighbouring Portugal, Banco Comercial Português seems a good match for Santander. Especially since both Iberian banks are active in Poland. Speaking of Poland, Santander and ING might be interested in mBank. mBank is owned by Commerzbank, a bank that desperately needs to focus its strategy.

A foreign group could shake up the uncompetitive Dutch market by buying ABN AMRO. However, as most of ABN AMRO is still state owned, this will be complicated.

Many listed insurers like Aegon, NN Group (NL), Ageas (BE), Baloise, Swiss Life (CH) or UnipolSai (IT) trade at a significant discount to their book value. This could be an opportunity for big insurance companies AXA, Allianz and Zurich Insurance Group.

Consortiums of buyers could also divide the operations of their targets (although there is a bad precedent for this scenario).

Exciting times!

Update 9 June 2020: Banco Sabadell plans to close 235 branches

Update 23 July 2020: Marc Rubinstein at Net Interest came to the same conclusion: “Coming out of Covid, when banks realise they don’t need such a large physical presence, further consolidation is likely. What’s more, if equity valuations don’t recover, banks may be able to use negative goodwill to cover restructuring charges.”

Door de lockdown hebben veel bedrijven verlies geleden. Het ligt voor de hand dat de overheid de schade moet vergoeden.

Maar in plaats van dat rechtstreeks te doen, met eenduidige voorwaarden, bouwt de politiek weer een reeks koterijen bij.

Politici hebben de mond vol van gerichte maatregelen en vereenvoudiging.

In realiteit krijgen we hinder- en sluitingspremies (een druppel op een hete plaat voor grotere bedrijven), lagere btw voor de horeca (hulp aan één sector), cadeaus voor kapitaalverstrekkers (investeren is risico’s nemen, waarom moet dit een fiscaal voordeel krijgen?)…

Ik hoop dat politici die voor deze maatregelen stemmen niet gaan zagen over de ingewikkelde belastingaangifte of over toekomstige begrotingstekorten1.

De gegoede klasse zoals politici, professoren en vermogensbeheerders (tiens, wie zat ook al weer in het economisch relancecomité?) wordt in de watten gelegd. Zo wordt de btw op restaurant verlaagd naar 6%2. En wie tot 75.000 euro belegt in “vriendenaandelen” krijgt als beloning een jaarlijkse belastingkorting.

The number of corona infections can roughly be modeled as N ~ R^t, where t is time1 and R is the reproduction number. The reproduction number R is the average number of new infections caused by one person infected with Covid-19.

If R > 1, the number of patients grows exponentially. If R < 1, the epidemic fizzles out.

How do people get infected? Obviously, they have to come into contact with the virus.

R is high when people are close together, indoors, and talking/singing/shouting. That explains why most infections occur at care facilities, slaughterhouses, prisons and at home2. There also seems to be a climatological effect. Sunlight, heat and humidity are correlated with a lower R. Genetic and (tuberculosis) vaccination differences between populations have been suggested to play a role.

Johannes Borgen (@jeuasommenulle) has estimated R for different countries3. You can find his methodology here.

As expected, lockdowns reduce R to below 1.

According to this map, the pandemic is still growing in Latin America, Africa and South Asia.

De coronacrisis is een ongeziene klap voor de economie.

Deze schok is helemaal anders dan de bankencrisis, de eurocrisis of de recessies van de jaren ’70 en ’80. De oorzaak van de huidige crisis ligt buiten het economisch systeem. Niet bij roekeloze bankiers, fiscale excessen, oliekartels, stakingen, inefficiënte bedrijven of torenhoge inflatie.

Bedrijven, werknemers, banken en belastingbetalers zitten momenteel in hetzelfde schuitje. Iedereen wil dat de economie zich veilig kan herstellen, zonder permanente schade.

Daarom is het teleurstellend dat belangengroepen de coronacrisis gebruiken om hun oude verlanglijstjes door te drukken.

Voorstellen als hogere belastingen voor “de rijken” of een btw-verlaging voor de horeca zijn niet nodig, niet eerlijk en niet efficiënt.

Het is veel beter om de reële schade te vergoeden. Zo kunnen bedrijven de crisis overleven en blijven de koopkracht en de tewerkstelling op peil. De banken zullen slechts minimale kredietverliezen lijden. Gerichte, tijdelijke coronasteun slaat geen gat in de toekomstige begroting, zodat er geen nieuwe belastingen nodig zijn.

Hoog tijd om de klassenstrijd te stoppen!

What is the inflation rate during and after lockdowns?

Inflation is already hard to measure in normal times, as I discussed in Bankers are people, too (page 126-129).

But the corona crisis adds further complications. Some services are unavailable due to the corona lockdown, for example restaurant visits and air travel. To discourage hoarding, supermarkets stopped offering discounts.

The abrupt shock causes headaches for statisticians.

For more, you should read Claire Jones’ Alphaville post on the fuzzy inflation figures.

Toegegeven, het klinkt te mooi om waar te zijn. Hoe kan een pizzarestaurant geld verdienen door haar eigen pizza’s te kopen?

Het verhaal begint met klachten over koude pizza’s. Bizar, aangezien het restaurant helemaal niet aan huis leverde!

Lees het volledige relaas van Ranjan Roy: Doordash and Pizza Arbitrage.

I don’t believe that the corona pandemic will fundamentally change the course of geopolitics or the global economy. As I predicted on March 25, 2020:

All the doomers, America-haters, EU-haters, permabears, moralizing nutters, communists, and libertarians are crawling out of the woodwork due to the coronavirus. However, I expect they will be proven wrong again. #timestamp#prediction

Stel je voor: twee bedrijven die actief zijn in de reissector.

Bedrijf A vervoert haar passagiers met een Airbus. Bedrijf B met een gewone bus.

Beiden zijn zwaar getroffen door de coronacrisis.

A was al zwaar ziek voor corona. De bedrijfsschulden zijn meer dan 10 keer het eigen vermogen en er is amper winst. A betaalt geen accijns op de brandstof die ze verbruikt en er is 0% btw op tickets.

B was kerngezond. Het bedrijf heeft nauwelijks schulden en maakt jaarlijks winst. B betaalt wel accijns op de brandstof die ze verbruikt en er is 6% btw op tickets.

Waarom zou A meer steun moeten krijgen dan B?

Dit is geen fictief voorbeeld, bekijk zelf de jaarrekeningen van A en B.

Waarom zou Brussels Airlines een speciale deal moeten krijgen?

Luchtvaartmaatschappijen betalen geen accijns op kerosine. Er is geen btw op vliegtickets. Brussels Airlines heeft een half miljard euro schulden. Het bedrijf maakt amper winst en betaalt dus bijna geen vennootschapsbelasting.

‘Ja maar’, zeggen lobbyisten, ‘Brussels Airlines is belangrijk voor de luchthaven van Zaventem’.

Dat geloof ik. Maar dan moet de luchthavenuitbater ook maar een duit in het zakje doen.

Andere argumenten:

Ik ben overigens niet tegen staatssteun, integendeel. Maar die steun moet dan wel afhangen van objectieve criteria. Geen discriminatie van KMO’s ten voordele van een lobbyende luchtvaartmaatschappij!