The German Federal Constitutional Court (Bundesverfassungsgericht) made a decisionconcerning the ECB’s QE program1.

This article explains how the ECB can defend itself.

But I want to play devil’s advocate, and defend the German judges.

Despite buying thousands of billions of euros worth of bonds, the ECB has undershot its inflation target for years. The Court has a point that buying vast amounts of sovereign debt doesn’t seem proportional to this disappointing outcome.

In fact, the ECB could achieve its primary objective of price stability with a much smaller balance sheet. For example by dual interest rates. Or by helicopter money.

Second, the Court could prohibit the Bundesbank from participating in QE. But buying German bonds was not needed for monetary policy anyway! It was a political decision to buy bonds proportional to the national capital key in the ECB.

Finally, the decision of the Court should force European politicians to fix this mess. Maybe the ECB should have a dual mandate like the Fed has, so inflation and employment carry the same weight in monetary policy decisions. Or they could change the structure of the Eurosystem. Do we still need 19 national central banks when we have the ECB? Sounds like a make-work scheme to me…

The corona crisis is a once-in-a-lifetime emergency. You cannot expect firms to anticipate zero revenu for months on end.

Therefore, it’s reasonable to help firms with loans and grants. But not all firms. Let’s reward corporate citizens who follow the law and pay taxes.

“Companies that evade their tax liability in Germany are not entitled to be saved by the German taxpayer” German Finance Minister @OlafScholz. https://t.co/Lx9aipCVeQ

3. Building up resilience must be a priority. Solid government institutions and #fiscal space are essential to mitigate economic breakdowns. Conditionalities should preclude companies using tax havens from public assistancehttps://t.co/jRf4mZwhof 7/n

A GENTLEMAN’S PRIMER ON SHORTING INSOLVENT SHITCOS

So you’ve found a ShitCo. It’s such an ugly zombie it couldn’t be an extra in season 19 of The Walking Dead But it’s still got a $185m cap And you want to be the one to mung the last rancid, putrefying drops out of that corpse

So if you want to convince me of your financial panacea, show me what it means in practice. Who are the winners and losers? What are the consequences of your plan for households, companies, banks, government finances, inflation, employment?

Two stories dominated popular economics over the past years. Both of them turn out to be useless in the current corona crisis.

Story 1: “Robots will take our jobs!”

Fact check: people lost their jobs due to shutdowns. But no robot is taking those jobs. Partly because of the nature of the crisis. We don’t want to go to crowded restaurants right now, not even if they have robot waiters. But also because robots aren’t ready. We still rely on (badly paid) people to pick fruit and to slaughter animals.

Story 2: “Crypto will replace fiat money and banks!”

Fact check: firms need cash. They don’t want bitcoin, but dollars and euros. Central banks and governments backstop the economy. This would be impossible with a cryptocurrency with a fixed supply, as I already pointed out in Bankers are people, too.

So instead of educating voters and policy makers about money, economic influencers have wasted years of popular discourse on these two sideshows.

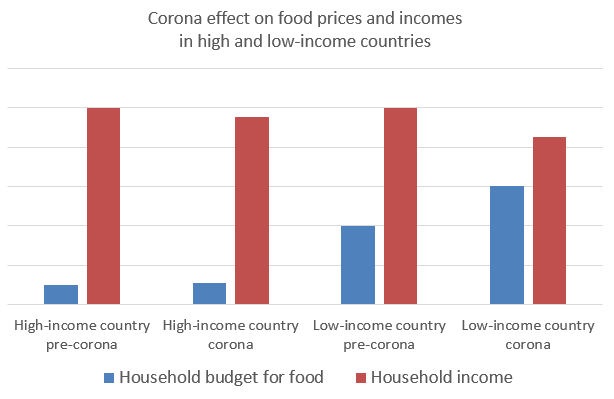

The amount of household income spent on food varies greatly by country. In countries like the U.S., Singapore and Australia, less than 10% of consumers’ income goes to food. Households spend more than 40% of their income on food in countries like Nigeria, Kazakhstan and Algeria.

How does the coronavirus affect food affordability? Affordability is a function of incomes and food prices.

Incomes

White collar workers can work from home during lockdowns. In countries with a strong social safety net, the government pays unemployment benefits to people who lose their jobs. The income loss of households due to lockdowns is modest.

On the other hand, lockdowns are devastating if they stop the informal economy and the state doesn’t support people’s incomes. Families who depend on remittances are in trouble if their relatives can’t earn and send money.

The corona crisis has hit certain sectors especially hard. Nations that depend on tourism or on the export of oil or garments face a severe dollar income shock.

Food prices

The coronavirus has raised retail food prices in multiple ways.

Schematic effect of (the reaction to) the coronavirus on food affordability. Note that there are huge inequalities within countries.

WEIRD economists should take into account inequality before advocating lockdowns.

If you want to learn more about the impact of Covid-19 on food security, you should follow the Food Pandemic Twitter account of R. Zurayk, N. Amhaz, A.Yehya. They share a lot of news from Africa and the Arab World.

A perspective from the South on food security in the pandemic by R. Zurayk | Journal of Agriculture, Food Systems, and Community Development https://t.co/6RR9WOFbMm

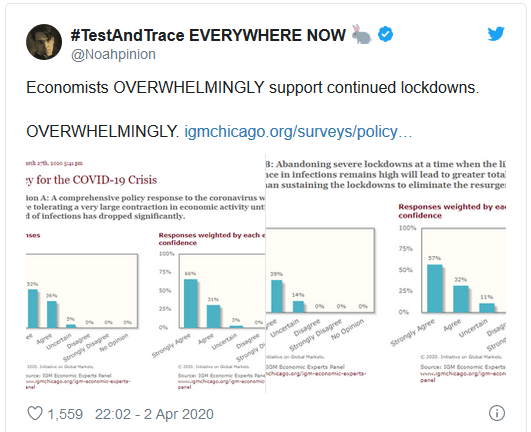

Most economists argue that there is no ‘health versus economics’ dichotomy. A widely shared article by Sergio Correia, Stephan Luck, and Emil Verner on the 1918 Spanish flu “suggest[s] that pandemics can have substantial economic costs, and NPIs [non-pharmaceutical interventions] can lead to both better economic outcomes and lower mortality rates”. Sam Bowman and Martin Eichenbaum, Sergio Rebelo and Mathias Trabandt believe that shutdowns are worth the lives saved, despite the costs.

On the other hand, Michael Burry and Toby Young think that governments are overreacting. Lockdowns cause disproportionate damage to people’s lives.

All of these commentators base their recommendations on the U.S. or Western Europe. But the best response to Covid-19 might be very different in the rest of the world. Not just food affordability, but also demographics and the effectiveness of measures to contain the virus differ greatly between countries. Economists are WEIRD.