In an event that has been called the WannaCry ransomware attack, hackers encrypted data on computers all around the world. The victims – which included hospitals and car factories – had to pay ransom in Bitcoin to get their files back.

Computers without up to date operating systems were particularly vulnerable to the attack.

People who have never come into contact with the internal IT operations of a large company find this hard to understand. Why don’t companies just install the latest patches, like private persons do on their home computers?

KBC Group is de enige beursgenoteerde bank-verzekeraar die België nog rijk is1. Vandaag vond de jaarvergadering plaats in de hoofdzetel aan de Havenlaan.

De resultaten van 2016 en de andere cijfers kan je in het jaarverslag (pdf) vinden. Alle agendapunten werden met een ruime meerderheid van de aanwezige aandelen goedgekeurd.

In tegenstelling tot vorig jaar, kwamen er veel vragen uit het publiek. Een activistische aandeelhouder van de “groene petten” had vragen over de rol van KBC in het dossier van de Nationale Bank van België (NBB). Deze affaire bewaar ik tot laatst. Continue reading “Jaarvergadering KBC 2017”

Eén van de populairste artikels op deze site legt uit hoe de Belgische personenbelasting berekend wordt. Door de taxshift zijn enkele details niet meer up-to-date. Dit is de nieuwe versie voor 2017. Ik heb de voorbeelden opnieuw doorgerekend en vergeleken met vorig jaar. Je zal zien dat de personenbelasting wel degelijk gedaald is1.

Donderdag 13 juli is de deadline om je belastingen door te sturen via tax-on-web. De website heeft een knop waarmee je je belastingen kan laten berekenen.

Je kan dus laten voorspellen hoeveel je zal terugkrijgen of zal moeten bijbetalen van de belastingen.

Maar hoe werkt die berekening eigenlijk? Je krijgt een hele resem onbegrijpelijke sommen te zien, vol codes en onduidelijke ambtenarentaal zoals “om te slane belasting”.

Hieronder leg ik het simpelste voorbeeld uit: een alleenstaande zonder kinderen die heel het belastingjaar2 bij één werkgever werkte en geen andere inkomsten heeft dan zijn loon. Hij woont in Vlaanderen, vlakbij het werk, heeft geen huis en doet niet aan pensioensparen of andere zaken die recht geven op een belastingvermindering.

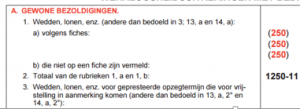

Wanneer je je loonbrief bekijkt, zie je dat er een (groot) verschil is tussen het brutoloon dat je werkgever betaalt, en het nettoloon dat op je rekening gestort wordt.

Er zijn twee belangrijke redenen waarom bruto en netto zo verschillend zijn: de RSZ en de personenbelasting. Van je brutoloon gaat 13,07% rechtstreeks naar de sociale zekerheid, de RSZ3. Deze RSZ bijdrage telt niet mee voor de berekening van jeinkomstenbelasting in Tax-on-web.

Het brutoloon (na aftrek van de RSZ-bijdrage) dat je verdiende in 2016 kan je vinden bij code 1250 van tax-on-web:

Banks create money. To be more precise, when a bank grants a loan, it simultaneously creates a deposit. Bank deposits are functionally equivalent to cash.

Economics education apparantly fails to pass on some elementary knowledge to students.

It doesn’t help that the activities of banks are often described as ‘monetary intermediation’. Intermediation implies that bankers are the middle men between borrowers and savers.

The English description of NACE code 64.1 is ‘monetary intermediation’. Source

However, there exists a much better description for banks. In Dutch, the formal description of banks is “geldscheppende financiële instellingen”, which literally means “money-creating financial institutions”:

The Dutch description of NACE code 64.1 means ‘money-creating financial institutions’. Source

As far as I can tell, Dutch is the only European language in which banks are described as active money creators1. All other languages use ‘monetary intermediation’.

Maybe everybody should take a cue from Dutch and start saying ‘money creating institutions’ from now on, so we don’t have this debate a hundred years from now 😛

===

I explain how banks create money in Bankers are people, too. After you’ve read my book, you’ll know more about banking than many PhD economists!

Update 20 October 2019: the link to the Bank of England paper was broken. It’s fixed now, thanks to Anna for notifying me!

The launch of the report was accompanied by a symposium in Brussels on Tuesday. During an interesting panel discussion, it was debated how the ECB can improve the way it works. Carl Dolan and Leo Hoffmann-Axthelm from Transparency International EU stressed that the ECB had cooperated with the NGO.

Many topics were covered during the discussion. For example the status of whistleblowers, freedom of information requests, and the “cool-off period” demanded when ECB executives move to the private sector.

Or to be more precise, debate about the financial institutional framework edition.

How should banks be regulated? Ten years ago, this question would have only interested a few specialists. Discussions about bank supervision and the role of the central bank were way too boring for the general public1. Besides, bankers surely knew what they were doing?

The global financial crisis and its aftermath changed this complacent attitude. The existing rules did not prevent the worse financial crisis since the 1930s. Governments had to bail out banks at a moment’s notice. Politicians took drastic decisions during the panic of September 2008. While those actions were taken with little democratic oversight, national leaders2 were the only agents willing and able to stop the collapse.

The crisis spurred a thorough update of bank regulation. Both in the United States and in Europe, legislation was passed to make banks safer. Avoiding a repetition of ad-hoc bailouts became a priority. The U.S. got its Dodd-Frank Act. The European Union (EU) set up the European Banking Authority (EBA) and worked towards a banking union3. America and Europe implemented capital and liquidity standards based on the Basel III recommendations. Continue reading “What I like about America, finance edition”

The internet offers an endless stream of analyses and opinions. On this blog, I sometimes comment on articles written by people who have a large audience. My disagreement with better known commentators is regularly confused for arrogance. “What do you know, dude? You are a blogger, the other guy is a professor.” Such statements show how easily people refer to authority1 instead of critically evaluating the arguments.

When I point out dubious logic, that does not mean the authors have nothing interesting to say. Quite the contrary, I often agree with them on many points. But pinpointing disagreements and calling assumptions into question can be very insightful. So when I critique for example Paul Krugman or Geert Noels, I’m not saying “neglect these fools”. I hope that readers will take into account my point of view, and confront it with that of others. I am no contrarian for the sake of being a contrarian.

This ideal dynamic is illustrated by historians David Wootton and Joel Mokyr. Mokyr’s book A Culture of Growth: The Origins of the Modern Economy explains why Western Europe was the first region in the world to make sustained technological and economic progress. In his review, Wootton summarizes the thesis put forth in the book. Then, he argues that the story is incomplete. In the comments below the review, both gentlemen defend their points of view.

That is one of the advantages of the internet. Well-informed contributors can quickly challenge opinions. I have learned a lot over the years from (often anonymous) online commentators. It is a shame many media have closed down the comment sections. Blocking feedback does not add to their credibility.

I would advise scientific journals to enable comments as well. Papers go through peer-review before they are published, but the reader cannot see these discussions. Commenting on a scientific article via a new publication takes a lot of time. Getting out new results and contradictory information faster would accelerate learning in all disciplines. Blogs can also expose disinformation.

If you don’t agree with me, you can always let me know in the comments!

Update 17/05/2017: Chris Said has a nice blog post on different levels of understanding. He calls the dialectic process of reaching the next level ‘Learning by flip-flopping‘. Open discussions as I advocate above are the means to transcend your previous, more basic knowledge.

Naar aanleiding van de honderdste verjaardag van de Russische Revolutie zond Klara een reeks uit over het reusachtige land. Radiomaker Johan de Boose vertelt over de Russische geschiedenis van Ivan de Verschrikkelijke tot de moord op de laatste tsarenfamilie. Je kan de podcastversie vinden op Trojka! Naar Rusland met Johan de Boose. Bijna tien uur luisterplezier!

Update 17/05/2017: Ik vond onlangs een boeiend artikel over een andere episode in de Sovjetgeschiedenis. Het gaat over kalenderhervormingen die gedreven waren door economische en ideologische motieven.

Wistje-dat-je: fabrieksarbeiders in de USSR leden aan wat studenten kennen als procrastinatie (uitstelgedrag):

Soviet sources are rife with complaints about the failure of newly arrived migrants [from the countryside] to shed their old work habits, in particular the tendency to slack for long periods of time only to compensate in a frantic rush as deadlines neared—a pattern of “storming” that remained a feature of the Soviet economy till the end. (Bron)

David Beckworth recently interviewed1 (podcast) professor Jesús Fernández-Villaverde. Among other things, they discussed the hyperinflation in the Weimar Republic, i.e. Germany after World War I. The economists ponder why a hyperinflation that occurred in 1923 has had such a large impact on German economists and central bankers, even to this day. After all, the NSDAP rose to power in the 1933, at a time of mass unemployment and austerity. This was almost a decade after the hyperinflation ended.

The professors get to the hyperinflation at 8:20 into the conversation. Fernández-Villaverde tells the story of how inflation got out of hand when French and Belgian troops occupied the Ruhr2. The Weimar government encouraged workers to resist the military occupation. Strikers were paid with money freshly printed by the Reichsbank, the German central bank. The combination of no real economic production with an increasing amount of Papiermarks tanked the purchasing power of the currency. The hyperinflation began. Continue reading “Why do Germans remember the Weimar hyperinflation?”

The European Conservatives and Reformists (ECR) group in the European Parliament recently launched “Leer Geld”, an initiative led by MEP Sander Loones, to raise awareness about the effects of the monetary policy conducted by the European Central Bank (ECB).

The initiative is to be welcomed: monetary policy is too often overlooked by civil society, yet its impact on our lives has never been greater. Under its “quantitative easing” programme (QE), the ECB has been buying large quantities of government bonds since 2015. Surely injecting the equivalent of 20 percent of GDP into the eurozone finance sector cannot be without consequences. (continue)