“In Europe, the relative underperformance of value [stocks] versus growth has not been as sustained since the early 1980’s. In the US, according to research by O’Shaughnessy Asset Management, investors have to go back to 1926-1941 to find a comparable period of sustained relative performance.”

That’s from Inflection Point, a blog post in which Marc Rubinstein takes a long term look at the valuation of stocks and the impact of technology on markets and the economy. The article has a lot of references.

Update: Chris Meredith of O’Shaughnessy Asset Management talked about his research on Odd Lots.

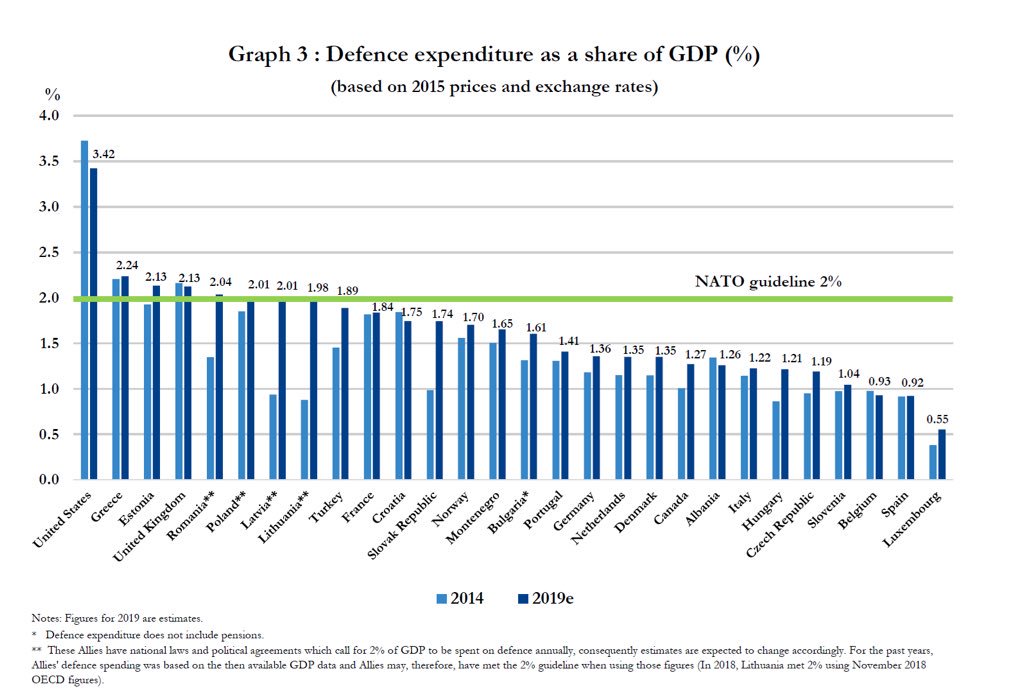

President Trump couldn’t buy Greenland from Denmark. In response, he tweeted that most NATO members don’t pay their fair share.

For the record, Denmark is only at 1.35% of GDP for NATO spending. They are a wealthy country and should be at 2%. We protect Europe and yet, only 8 of the 28 NATO countries are at the 2% mark. The United States is at a much, much higher level than that….

For some strange reasons there seem to be a flurry of tweets and takes about the incoming crisis of Eurozone banks – probably partly triggered by Raoul’s tweets, partly by those chart below. So a quick thread on the situation of EZ banks today. https://t.co/yx3IFXTkT2pic.twitter.com/8jLyUtOBns

Some talk out there about "total collapse of the entire EU banking sector”. I don't buy it. Share prices follow, they don't lead. Few banks need to raise capital, and firewalls now in place to protect funding. Which is why there’s no panic in credit. /1https://t.co/80od6yvHfI

I have changed jobs! I’m back at Ghent University, studying financial networks. I intend to use this platform to share thoughts on my research, in addition to the usual topics.

Posts about local issues (e.g. Belgian taxes or personal finance) will be written in Dutch and sometimes crossposted on the Facebook page of my book Hoe bankiers geld scheppen.

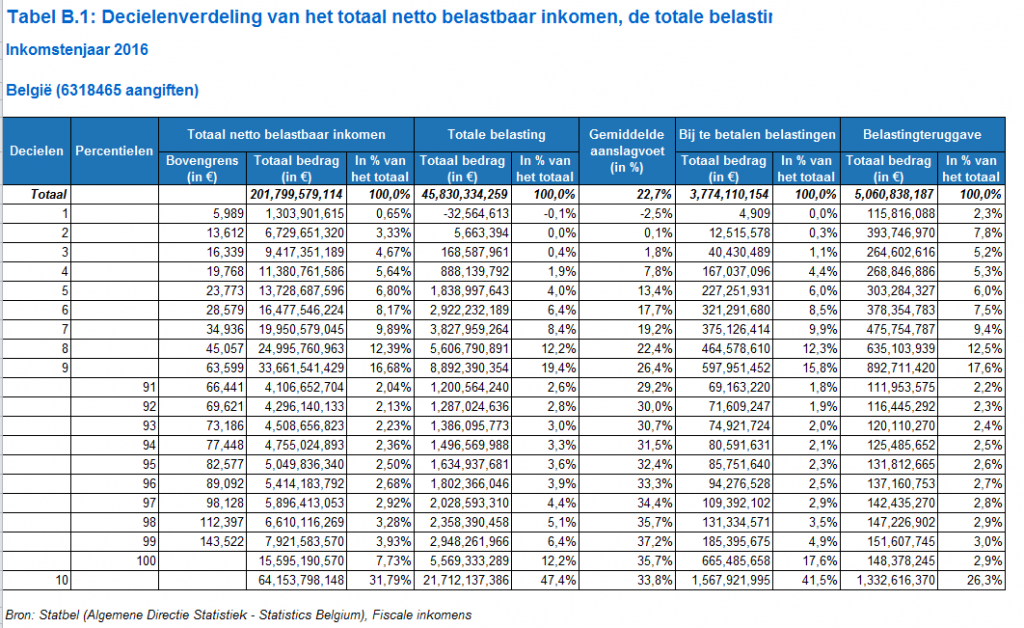

Je hebt nog tot 11 juli om je belastingaangifte te doen via Tax-on-Web.

Maar hoeveel (personen)belasting betalen de andere Belgen? De onderstaande tabel toont de verdeling van de inkomsten en bijhorende belastingen. De hoogste tien procent is verder uitgesplitst.

Meer details over de belastinginkomsten, onder andere over de geografische spreiding, kan je vinden op de website van StatBel.

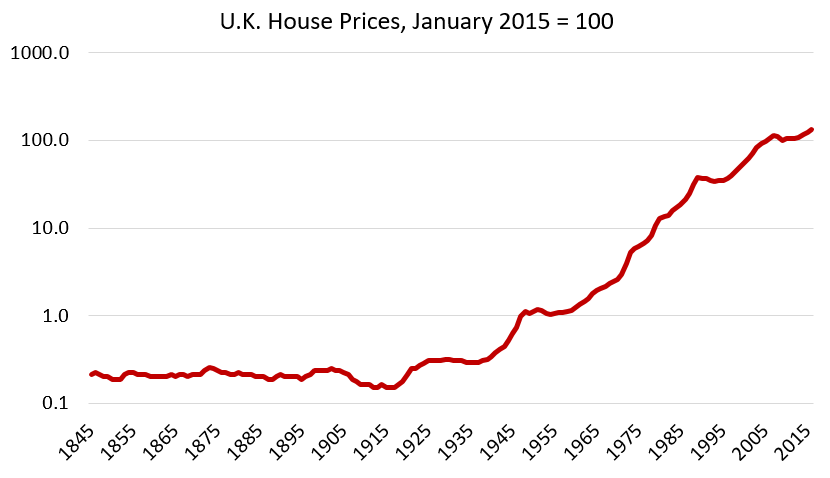

De Britse journalist Mike Bird deelde onlangs een vergelijkbare grafiek op Twitter. Onderstaande figuur toont de evolutie van de (nominale) huizenprijzen in het Verenigd Koninkrijk sinds 1845. Let op de logaritmische schaal: één streep hoger = tien keer duurder.

Spaarders krijgen al jaren erg weinig rente op hun spaargeld. De Duitse journalist Holger Zschaepitz noemt dit een “geheime onteigening van spaarders door de financiële repressie van de ECB”.

Het is volgens Zschaepitz dus de schuld van de centrale bank. Maar in de Verenigde Staten is er ook een centrale bank, en daar krijgen actieve1 spaarders meer dan 2 procent rente. Hoe is dit verschil tussen de eurozone en de V.S. te verklaren?

Eén van de redenen is het feit dat de Amerikaanse federale overheid het voorbije decennium veel grotere tekorten opgestapelde dan de overheden in de eurozone.

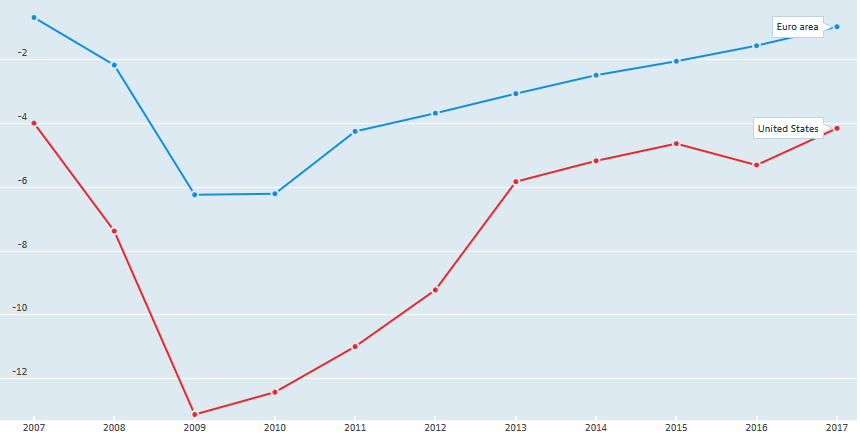

Overheidstekort als percentage van het bruto binnenlands product in de Verenigde Staten (rood) en de eurozone (blauw). Bron van data en figuur: OESO.

Dit klinkt slecht voor de V.S., tot je naar de economische resultaten kijkt. De V.S. hebben een lagere werkloosheidsgraad en een hogere economische groei dan de eurozone. In plaats van hun schuldgraad te verkleinen, zouden landen met begrotingsoverschotten beter de belastingen verlagen of noodzakelijkeinvesteringen doen2. Dat zou de economie in heel de eurozone een duwtje in de rug geven. En dan zou de ECB in navolging van de Fed de rente kunnen optrekken.

Journalisten en politici in Duitsland moeten beseffen dat ze deel uitmaken van een muntunie. De ECB kan niet enkel rekening houden met de Duitsers. Droog dus je tranen, Holger.

“125.000 arbeiders dumpen groepsverzekering voor pensioenfonds“. De Tijd schrijft dat de sociale partners van de sectoren garages, metaalhandel, koetswerk, metaalrecuperatie en edele metalen1Sefoplus hebben opgericht. Sefoplus is een ‘instelling voor bedrijfspensioenvoorziening (IBP)’, beter bekend als ‘een pensioenfonds’.

Tot nu toe hadden de arbeiders in deze sectoren een groepsverzekering. De verzekeraar wou echter geen minimumrendement van 1,75% meer garanderen.

In het artikel wordt niet vermeld wie de verzekeraar is. Ik heb wat opzoekingswerk gedaan. Hieronder lees je over welke verzekeringsmaatschappij het gaat, en hoe de tweede pijler van het Belgische pensioensysteem werkt.

The ECB has released the declarations of interest of its executive and supervisory board members.

You’ll see that the forms are pretty vague when it comes to point IV – Financial interests. Board members should name “Any financial interests holdings in companies/firms listed on a stock exchange”.

Some members have included equity funds and bonds under this item, although one could argue if that’s really required.

However, the declarations of interest do contain some remarkable info:

German board members Sabine Lautenschlager-Peiter and Joachim Wuermeling own co-operative shares in banks. The value of these holdings is trivial.

Ed Sibley owns some shares in Bank of Ireland. Mr. Sibley adds: “These are the remnants from a share ownership scheme from when I worked for Bank of Ireland (until 2008). They are worth less than €500, and I am in the process of getting rid of them.”

The spouse/partner of Vytautas Valvonis works at the Lithuanian branch of Dankse Bank.

Several board members (Benoît Cœuré, Tom Dechaene, Yves Mersch, Gaston Reinesch, Vitas Vasiliauskas, Claude Wampach) teach at universities (see item II – private activities). The earnings from these professorships are trivial.

Mr. Wampach owns Turkish lira denominated bonds issued by the European Investment Bank. Let’s hope he hedged the currency risk 😉

The financial interests of board members Margarita Delgado (Spain), Catherine Galea (Malta) and Andreas Ittner (Austria) contain only securities from their home countries.

Constantinos Herodotou (Cyprus), Madis Müller (Estonia) and Pierre Wunsch (Belgium) have the most diversified investment portfolios – Mr. Müller even owns a gold ETF. They should teach their colleagues about the importance of diversification!